You're watching your Excel spreadsheet with 12 open option positions, trying to remember which cash-secured put expires Friday and whether you already collected that covered call premium this week. Your broker shows you got assigned last Tuesday, but calculating your actual cost basis—accounting for all the premium you've collected—requires pulling out a calculator and hoping you didn't miss anything.

There's a better way to generate income from options trading without the spreadsheet chaos.

You can create a full system inside QuantWheel, from discovering trades to journaling them.

Introduction

The options wheel strategy has become one of the most popular approaches for traders looking to generate consistent income from the stock market. Unlike purely directional strategies that bet on stocks moving up or down, the wheel strategy focuses on collecting premium while positioning yourself to own quality stocks at prices you're comfortable with.

This complete guide walks you through everything you need to know about the wheel strategy—from the basic mechanics that make it work to advanced position management techniques that separate profitable traders from those who struggle. You'll learn exactly what happens at each stage of the wheel, how to handle the situations that confuse most beginners, and the tracking systems that prevent costly mistakes.

Whether you're completely new to options or you've been selling premium for years, this guide gives you the framework to implement the wheel strategy with confidence.

TLDR: The Options Wheel Strategy Explained Simply

The wheel strategy is like being a landlord for stocks—you get paid to wait, and you're happy whether you buy the property or just keep the rent.

Here's how it works in plain English:

Step 1: Get paid to set a buy limit order You sell a "cash-secured put" on a stock you'd be willing to own. Let's say AAPL is trading at $180, and you sell a put with a $170 strike price, collecting $3 per share ($300 per contract). You now have $170 in cash set aside, and you're getting paid $300 to potentially buy AAPL at $170.

Step 2: Two possible outcomes

- Option A: AAPL stays above $170. Your put expires worthless, you keep the $300 premium, and you start over (sell another put).

- Option B: AAPL falls below $170. You're "assigned"—meaning you buy 100 shares at $170 each. Your real cost? $167 per share ($170 strike minus the $3 premium you collected).

Step 3: If assigned, sell covered calls Now you own 100 shares of AAPL at an effective cost of $167. You sell a "covered call" with a $175 strike for another $2 per share ($200). This gives someone the right to buy your shares at $175.

Step 4: Two possible outcomes again

- Option A: AAPL stays below $175. Your call expires worthless, you keep the $200 premium, and you sell another call.

- Option B: AAPL rises above $175. Your shares get "called away" (sold at $175). You make the difference ($175 sale - $167 cost = $8/share) plus all the premiums collected.

The "wheel" completes: You're back to cash, having collected premium at every step, and you start over with step 1.

The key insight: You make money whether the stock goes up, down, or sideways. You only lose if the stock crashes and stays down—but you picked a quality stock you were willing to own anyway.

Simple example with real numbers:

- Sell $50 put, collect $2 premium → Assigned at $50 (real cost: $48)

- Sell $52 covered call, collect $1 premium → Called away at $52

- Total profit: $5 per share ($2 put premium + $1 call premium + $3 capital gain) on a stock that only moved from $48 to $52

That's the wheel strategy. Conservative. Systematic. Boring. Profitable.

What Is the Options Wheel Strategy?

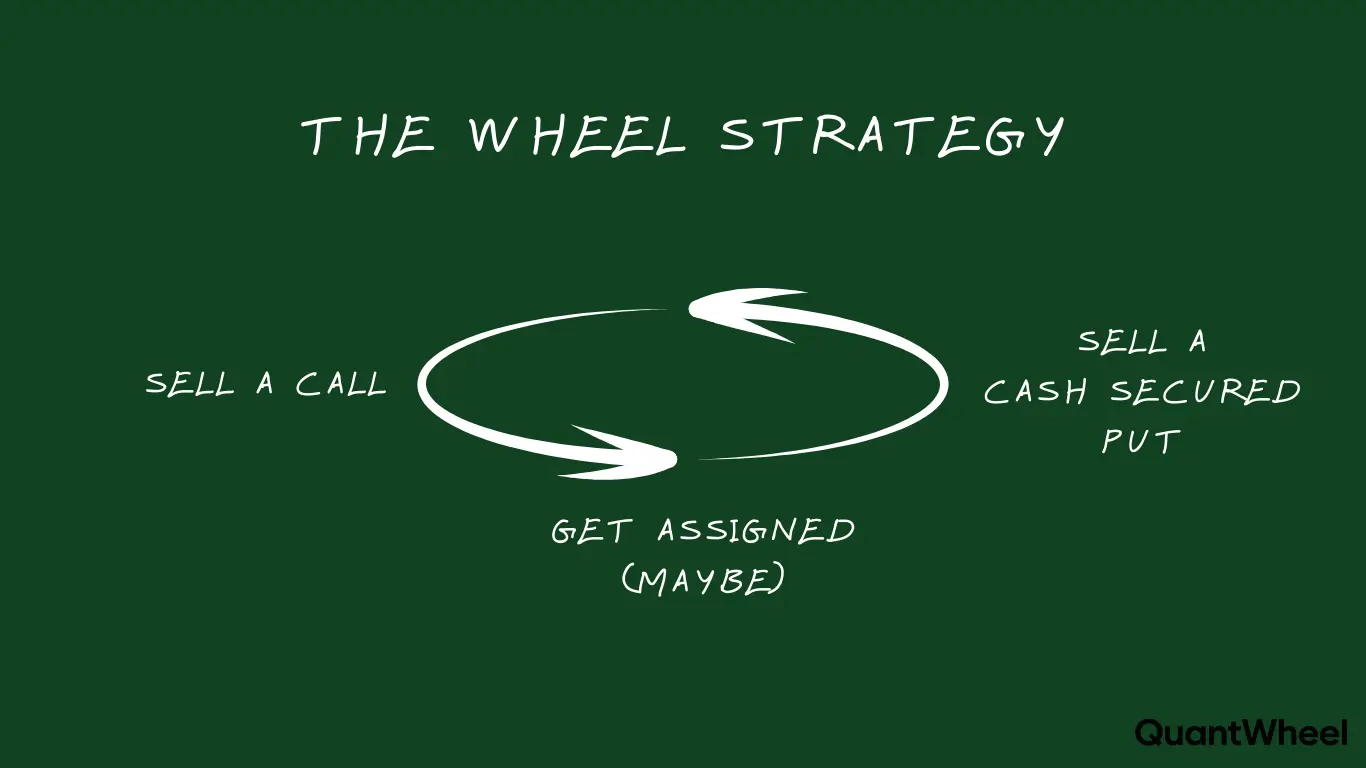

The options wheel strategy is a systematic options trading approach that combines two foundational strategies—cash-secured puts and covered calls—into one continuous income-generating cycle.

At its core, the wheel strategy works like this: You sell cash-secured puts on stocks you wouldn't mind owning. If the stock price stays above your strike price, the option expires worthless and you keep the premium you collected upfront. If the stock falls below your strike, you get "assigned" and purchase 100 shares at the strike price. Once you own the shares, you sell covered calls against them, collecting more premium. If the stock rises above your call strike, your shares get called away (sold), completing the wheel cycle.

The term "wheel" refers to the continuous nature of this approach—you keep rotating through the same sequence: sell puts, potentially get assigned, sell calls, potentially have shares called away, then start over with puts again.

Basically, your goal is to pick trades with strike prices where the stock isn't likely to reach, but if it reaches it then you're okay with it, as long as you respect some ground rules about the wheel.

The Core Components

Cash-Secured Puts: The entry point of the wheel strategy. You sell a put option contract, which obligates you to buy 100 shares of the underlying stock at the strike price if the option is exercised. "Cash-secured" means you keep enough cash in your account to fulfill this obligation. In exchange for taking on this obligation, you collect premium upfront.

Assignment: This is what happens when the stock price falls below your put strike price at expiration. Your broker automatically purchases 100 shares at the strike price and debits your account for the cash. Assignment isn't a failure—it's part of the strategy. Your actual cost basis is the strike price minus all the premium you collected on the put.

Covered Calls: Once you own the shares from assignment, you sell call option contracts against those shares. This gives someone else the right to buy your shares at the strike price. You collect premium for providing this right. "Covered" means you own the underlying shares, limiting your risk.

Called Away: When the stock price rises above your call strike price at expiration, your shares get sold at the strike price. You keep all the premium collected from the covered calls, plus any capital gains from the difference between your cost basis and the call strike price.

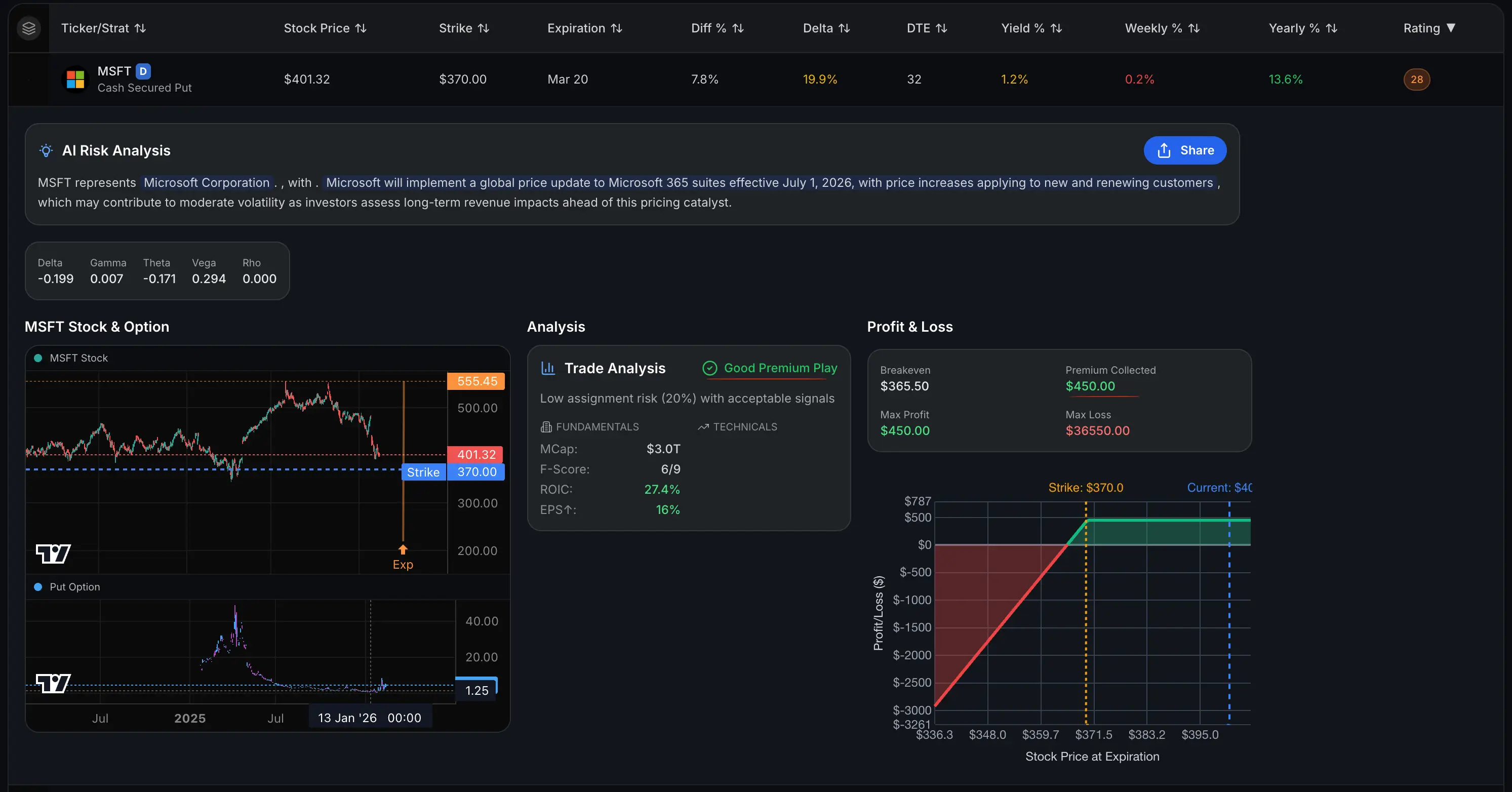

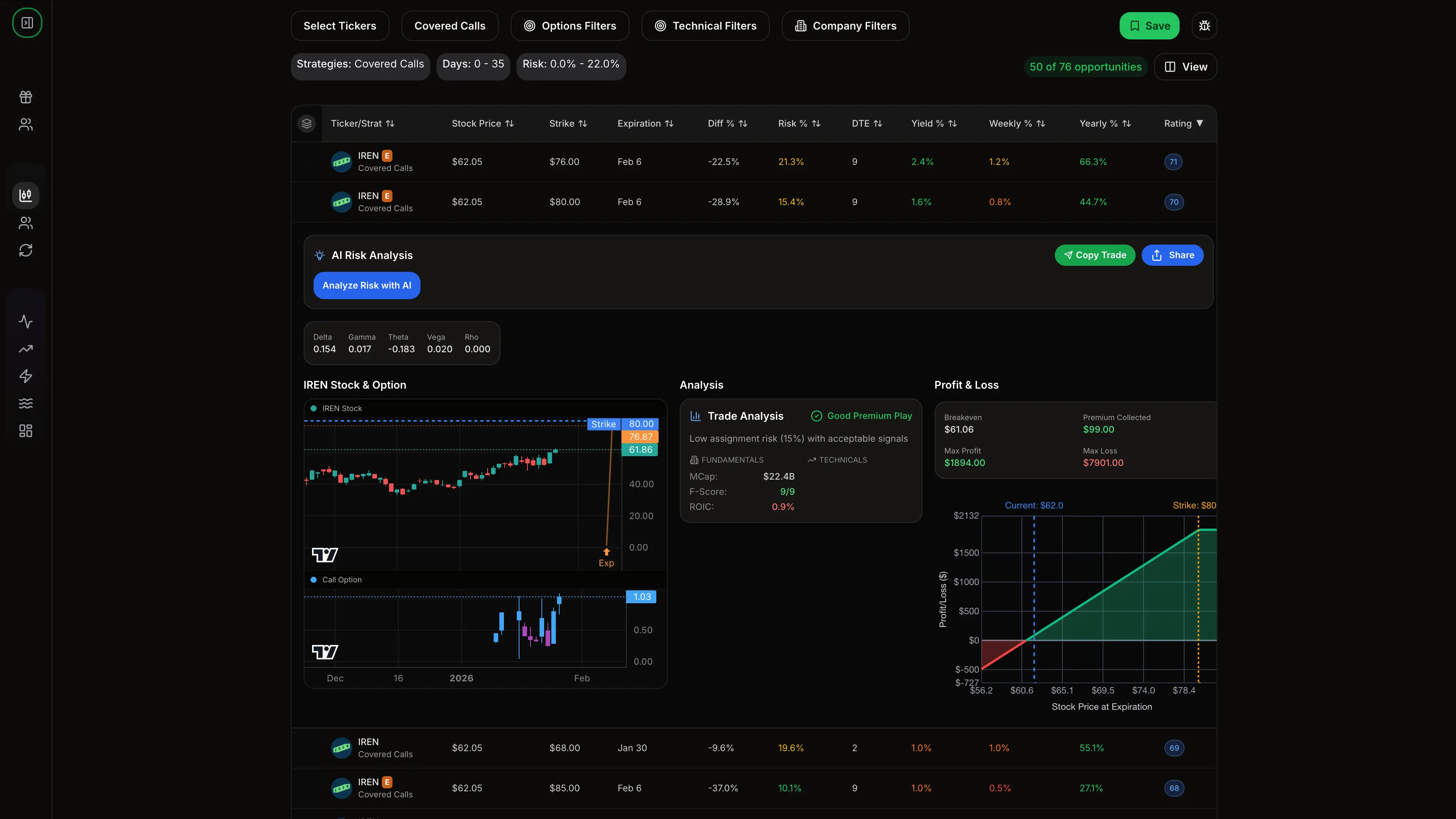

Example of a good Cash - Secured put trade:

Example of a good Covered Call trade after you've entered the wheel:

Why Traders Use the Wheel Strategy

The wheel strategy appeals to traders who want to generate income from their portfolio without constantly predicting market direction. Instead of betting on whether a stock will go up or down, you're positioning yourself to profit in multiple scenarios.

You profit when the stock stays flat (premium collection without assignment), when it rises moderately (premium collection plus capital gains), and even when it declines modestly (premium cushions the loss). The strategy only struggles when stocks experience severe, sustained declines—which is why stock selection matters enormously.

Many traders transition to the wheel strategy after getting frustrated with purely directional approaches that require perfect market timing. The wheel provides a more systematic, rules-based approach that generates returns through statistical edges rather than market predictions.

The Philosophy Behind the Wheel

The wheel strategy embodies a fundamentally conservative approach to options trading. Rather than using options for leverage or speculation, you're using them as an income overlay on stocks you're comfortable owning long-term.

This philosophy aligns with the concept of "getting paid to wait." When you sell cash-secured puts, you're essentially setting a limit buy order on a stock you want to own—except you're getting paid premium to place that order. When you sell covered calls, you're setting a limit sell order on shares you already own—again collecting premium for your patience.

The wheel works best when you think of assignment as the plan, not the backup plan. Many beginners view assignment as something to avoid, but experienced wheel traders recognize that the full cycle—from put sale through assignment to covered calls and back to cash—is where the strategy generates its most consistent returns.

How the Wheel Strategy Works (Step-by-Step)

Understanding the mechanics of each wheel strategy phase helps you execute with confidence and avoid the mistakes that trip up beginners.

Phase 1: Selling Cash-Secured Puts

Your wheel journey starts by identifying a stock you'd be willing to own at a price below current market value. Let's use a real example with specific numbers.

Example Setup:

- Stock: AMD (Advanced Micro Devices)

- Current price: $115 per share

- Your target buy price: $110 per share

- Option selected: 30-day put with $110 strike

- Premium collected: $2.80 per share ($280 per contract)

When you sell this cash-secured put, you're making an agreement: "I'll buy 100 shares of AMD at $110 if the price falls below that level by expiration in 30 days. Pay me $280 upfront for taking on this obligation."

Your broker immediately sets aside $11,000 in cash (100 shares × $110 strike price) to ensure you can fulfill the obligation. This cash sits in your account earning no interest, but you've collected $280 in premium immediately.

Two Possible Outcomes:

Scenario A: AMD stays above $110 at expiration The put expires worthless because nobody would exercise the right to sell AMD at $110 when they can sell it for $115+ on the open market. You keep the entire $280 premium. Your cash is released, and you can sell another put to start a new wheel cycle. In 30 days, you made $280 on $11,000 in cash (2.5% return in one month).

Scenario B: AMD falls to $105 at expiration Your put finishes "in the money" because the strike price ($110) is above the market price ($105). You get assigned—meaning you must buy 100 shares at $110 each. Your broker debits $11,000 from your cash account and credits 100 shares of AMD to your portfolio.

Here's the critical insight most brokers don't show you clearly: Your real cost basis isn't $110 per share. You collected $2.80 in premium, so your effective cost is $107.20 per share. You paid $11,000 but received $280 up front, so your net outlay is $10,720 for 100 shares.

This cost basis calculation becomes increasingly important as you continue the wheel cycle, and it's where manual tracking becomes error-prone. Platform solutions like QuantWheel automatically adjust your cost basis when assignments happen, ensuring you always know your real entry price.

Phase 2: Managing Assignment

Assignment typically occurs automatically over the weekend after expiration Friday. On Monday morning, you'll see 100 shares in your account where you previously had a put option.

What actually happens during assignment:

- The Options Clearing Corporation (OCC) matches your short put with someone exercising a long put

- Your broker receives the assignment notice

- Your broker purchases 100 shares at the strike price

- Your cash account is debited for the full amount

- The shares appear in your portfolio

Important timing notes: Assignment can technically happen any time before expiration if your put is deeply in the money, though this is relatively rare with American-style equity options. Most assignments occur at expiration. If you're holding a put option through expiration that's even $0.01 in the money, expect assignment.

Your immediate priorities after assignment:

- Calculate your adjusted cost basis (strike price minus premium collected)

- Evaluate the stock's current price and recent news

- Check upcoming earnings dates (you may not want to hold through earnings)

- Determine your covered call strategy (which strike, which expiration)

Some traders make the mistake of panicking after assignment, especially if the stock has continued declining. Remember: You selected this stock because you were willing to own it at this price. Assignment means your initial thesis is playing out—you're buying a quality stock at a discount to where it was trading when you sold the put.

Phase 3: Selling Covered Calls

Once you own the shares, you transition to the covered call phase of the wheel. This is where you generate additional income on your stock position while defining your exit price.

Continuing our AMD example:

- Your cost basis: $107.20 per share (after accounting for put premium)

- Current price: $105 per share (you're underwater by $2.20 per share)

- Option to sell: 30-day call with $110 strike

- Premium collected: $2.50 per share ($250 per contract)

When you sell this covered call, you're making a different agreement: "If AMD rises above $110 in the next 30 days, I'll sell my 100 shares at that price. Pay me $250 upfront for this commitment."

Two Possible Outcomes:

Scenario A: AMD stays below $110 at expiration Your call expires worthless. You keep the $250 premium and still own the shares. You can immediately sell another covered call, continuing to collect premium while you wait for the stock to recover. Your effective cost basis has now dropped to $104.70 ($107.20 original cost minus $2.50 in call premium).

Scenario B: AMD rises to $115 at expiration Your call finishes in the money. Your shares get called away—sold at $110 per share. Let's calculate your total profit on this complete wheel cycle:

- Put premium collected: $280

- Call premium collected: $250

- Capital gain: $280 (bought at effective $107.20, sold at $110)

- Total profit: $810 on $10,720 invested = 7.6% return in approximately 60 days

Your shares are now gone, you're back to 100% cash, and you can start a new wheel cycle by selling another cash-secured put.

Phase 4: Strike Selection Strategy

Choosing the right strike prices for both your puts and calls significantly impacts your wheel strategy results. This is where the mechanical process meets strategic decision-making.

For cash-secured puts:

Most wheel traders target strikes around the 30-delta level (roughly 30% probability of finishing in the money at expiration). This delta level provides a reasonable balance between premium collection and assignment probability.

A 30-delta put typically sits 5-10% below the current stock price, depending on the stock's implied volatility. On a $100 stock with moderate volatility, you might sell the $95 strike. On a high-volatility stock, the 30-delta strike might be $90 or lower.

The higher your strike (closer to current price), the more premium you collect but the higher your assignment probability. The lower your strike (further from current price), the less premium you receive but the lower your assignment probability. Your strike selection should align with how aggressively you want to generate income versus how much cash you want to keep dry.

For covered calls:

Strike selection becomes more nuanced on the covered call side because you need to consider your cost basis, not just the current stock price.

If you're holding shares above your cost basis (you're profitable), you can sell calls at strikes above your entry, locking in a profit if called away. If you're holding shares below your cost basis (you're underwater), you face a decision: sell calls above your cost basis and potentially give up recovery gains, or sell calls at or below your cost basis and accept potentially selling at a loss.

Many traders follow the "never sell calls below cost basis" rule, preferring to wait for recovery rather than locking in a loss. Others take a more aggressive approach, selling calls at any strike that generates acceptable premium, recognizing that capital is better deployed in new opportunities than sitting in underwater positions indefinitely.

Phase 5: Rolling Options (Advanced Management)

Rolling is the process of closing your existing option and simultaneously opening a new option at a different strike price and/or expiration date. This technique allows you to manage positions that aren't working out as planned without completely abandoning your strategy.

When to consider rolling:

Rolling puts before assignment: If you sold a $100 put and the stock has fallen to $95, you might choose to roll to avoid assignment. You'd buy back the $100 put (taking a loss) and simultaneously sell a new put at a lower strike or further expiration (or both), collecting additional premium. This extends your timeline and adjusts your strike to current market conditions.

Rolling calls to avoid profit caps: If you sold a $110 call with your cost basis at $105, and the stock suddenly jumps to $120, you might not want to cap your gains at $110. You could roll the call to a higher strike (like $125) at the next expiration, paying to close the current call but collecting premium for the new one.

Rolling for additional premium: If your option is close to expiration but not quite at your target price, rolling to the next expiration at the same strike can collect additional premium, giving your thesis more time to work out.

The roll decision framework:

Rolling makes sense when the additional premium collected exceeds the cost of buying back your existing option, AND you still believe in your thesis for the position. Rolling doesn't make sense when you're simply avoiding realizing a loss on a thesis that's proven wrong.

Here's where professional tracking becomes essential. When you roll an option, you're creating a series of related trades that need proper accounting. Did you close the roll at a net credit (collected more premium than you paid)? How many times have you rolled this position? What's your total premium collected across all rolls? What's your effective time invested?

QuantWheel automatically tracks roll sequences, showing you the cumulative P&L across all related options in a chain. Without this tracking, determining whether your rolling strategy is working or you're just delaying inevitable losses becomes guesswork.

Stock Selection: The Foundation of Wheel Success

The wheel strategy's success depends more on stock selection than on options tactics. You can execute perfect strikes and expirations, but if you're wheeling low-quality stocks, you'll struggle.

Characteristics of Wheel-Friendly Stocks

Quality first, premium second: The single most important criterion is that you genuinely want to own this stock long-term at the price you're targeting with your puts. Every time you sell a put, ask yourself: "If I got assigned and this stock fell another 20%, would I be comfortable holding these shares for a year?"

If the answer is no, don't sell the put—no matter how attractive the premium looks.

Adequate liquidity: Wheel strategies require consistent options volume for reasonable bid-ask spreads. Target stocks with at least 1,000 average daily option volume on your target expiration dates. Liquid options markets give you flexibility to adjust positions without excessive slippage.

Moderate to high implied volatility: Higher volatility generates more premium, making the math of the wheel strategy more attractive. Stocks with implied volatility rank (IVR) above 50 typically offer better premium relative to risk. However, volatility alone doesn't make a stock wheel-worthy—it needs to be paired with quality fundamentals.

Stable underlying business: You want volatility in options prices, not existential risk in the business model. Companies with proven business models, strong balance sheets, and sustainable competitive advantages make better wheel candidates than speculative growth stories or declining businesses.

Stock Categories to Consider

Large-cap tech: Companies like AMD, NVDA, MSFT, and AAPL often provide good wheel opportunities. They combine solid fundamentals with enough volatility to generate meaningful premium. The risk is concentration—tech stocks tend to move together, so running multiple tech wheels increases correlation risk.

Dividend aristocrats: Stocks like JNJ, PG, and KO offer lower premiums due to lower volatility, but they provide downside protection through dividend income and generally stable prices. These work well for conservative wheel traders who prioritize safety over maximum income generation.

ETFs: SPY, QQQ, and IWM can be excellent wheel candidates for traders who want broad market exposure rather than single-stock risk. ETF options are highly liquid, and the diversified holdings reduce the risk of catastrophic losses from company-specific events.

Red Flags to Avoid

Avoid meme stocks and excessive hype: Stocks driven by social media sentiment rather than fundamentals create dangerous wheel conditions. Premium looks attractive because implied volatility is elevated, but you risk assignment on stocks that can fall 50%+ quickly when sentiment shifts.

Be cautious around earnings: Elevated implied volatility often appears right before earnings announcements, making option premiums temporarily attractive. However, post-earnings volatility crush can leave you with positions that immediately show losses. Many wheel traders close positions before earnings or avoid selling new options during earnings season.

Question stocks with declining fundamentals: If a stock's business is genuinely deteriorating (not just experiencing temporary headwinds), collecting premium while it declines is just losing money slowly. High premium on declining stocks is the market telling you there's real risk—listen to that signal.

Position Sizing and Risk Management

Even the best stock selection and option execution can't overcome poor position sizing. The wheel strategy ties up significant capital per position (you need cash to secure puts and eventually own shares), so managing how much capital goes into each position matters enormously.

The Capital Allocation Framework

Position size per stock: Most experienced wheel traders risk no more than 5-10% of their portfolio on any single stock. If you have a $100,000 account, that means your individual put strikes shouldn't exceed $5,000-$10,000 (50-100 shares worth).

This sizing protects you from concentration risk. Even if you selected a quality stock and it declines 50%, limiting exposure to 5-10% of your portfolio means your overall portfolio only declines 2.5-5% from that single position.

Total cash deployed: You need to decide how much of your portfolio to allocate to wheel strategies versus keeping in reserve. Conservative traders might wheel with 50-60% of capital, keeping 40-50% in cash or other investments. Aggressive traders might wheel with 80-90%, keeping only minimal cash reserves.

The right allocation depends on your risk tolerance and whether you're running the wheel as your primary strategy or as one component of a diversified portfolio.

Scaling based on confidence: Not all wheel opportunities are created equal. You might allocate 10% to your highest-conviction stocks and only 3-5% to opportunities that look attractive but aren't slam dunks. This weighted approach aligns position sizes with conviction levels.

Managing Multiple Positions

Once you're running more than 2-3 wheel positions simultaneously, tracking becomes complex. You need clear visibility into:

- How many positions you're currently managing

- Expiration dates for all options (puts and calls)

- Total cash required to cover all possible assignments

- Current P&L on each position and aggregated

- Upcoming events (earnings, ex-dividend dates, economic reports)

This is where manual spreadsheet tracking starts breaking down. You update a cell wrong, or forget to update after a roll, and suddenly your tracking is inaccurate. Positions slip through the cracks, expirations surprise you, and you make decisions based on incomplete information.

Professional tracking tools designed specifically for wheel traders—like QuantWheel's position management dashboard—automatically sync with your broker, track all open positions, alert you to upcoming expirations, and calculate aggregate metrics like total capital deployed and portfolio-level Greeks. This visibility prevents the mistakes that come from information gaps.

When to Close Positions Early

You don't have to hold every option until expiration. In fact, many successful wheel traders follow rules about early closure:

The 50% profit rule: If your option has lost 50% of its value (meaning you can buy it back for half what you sold it for), many traders close the position immediately rather than waiting for the final 50% to decay. This rule is based on the observation that options lose value slowly as they approach expiration—the last 50% of premium takes much longer to decay than the first 50%.

Taking profits at 50% lets you redeploy capital into new positions with fresh time decay, potentially generating more premium over time than waiting for every option to expire completely.

The bad thesis rule: If the fundamental reason you selected a stock changes (earnings disappoint, business model is disrupted, management makes questionable decisions), close the position even if it means taking a loss. Don't let the wheel strategy mechanics force you to hold positions you no longer believe in.

The opportunity cost rule: Sometimes better opportunities emerge while you're waiting for current positions to play out. If you find a significantly better wheel candidate but don't have capital available, it might make sense to close current positions early (even if it means foregoing some premium) to free up capital for the superior opportunity.

Tracking and Accounting: The Hidden Challenge

Here's a problem that doesn't get discussed enough in wheel strategy content: the tracking and accounting burden becomes overwhelming faster than you expect.

Why Tracking Matters

When you're running one or two positions, tracking in your head or a simple spreadsheet works fine. You remember that you sold a put for $2, got assigned at $50, and now you're selling calls. Easy.

But once you scale to 5+ positions, the complexity multiplies exponentially:

- Position 1: Currently in cash-secured put phase, expires in 12 days

- Position 2: Got assigned two weeks ago, sold first covered call, expires in 18 days

- Position 3: Been through three roll sequences on the covered call, need to track total premium across all rolls

- Position 4: About to get assigned based on Friday's close, need to plan covered call strategy

- Position 5: Shares got called away last week, ready to start new put cycle

Each position is at a different phase, with different cost basis calculations, different premium totals, and different management requirements. Your spreadsheet now has 20+ rows of data, formulas that break when you update cells, and constant manual entry every time something happens.

The Cost Basis Problem

This is where most traders struggle: calculating real cost basis after multiple transactions.

Let's trace a complete cycle:

- Sell $50 put, collect $2 premium → Your commitment: buy at $50

- Get assigned → Broker shows cost basis of $50, but real cost is $48

- Sell $52 covered call, collect $1.50 premium → If called away, real profit is $5.50/share ($2 put + $1.50 call + $2 capital gain)

- Call expires worthless → Cost basis should now show as $46.50 ($48 minus $1.50 call premium)

- Sell $51 covered call, collect $1.20 premium → Real cost basis now $45.30

- Get called away at $51 → Total profit $5.70 per share ($2 + $1.50 + $1.20 + $1)

Your broker's records might show you bought at $50 and sold at $51 for $1/share profit. But you actually made $5.70/share when accounting for all the premium collected across the cycle. If you're not tracking this accurately, your performance reporting is wrong, your tax preparation is complicated, and you can't make informed decisions about which positions are actually working.

Here's where platforms like QuantWheel solve a real problem: Automatic cost basis adjustment on every transaction in the wheel cycle. When you get assigned, your cost basis automatically updates to reflect premium collected. When you sell covered calls, your effective cost basis continues adjusting. When shares get called away, the platform calculates your total profit across the entire cycle—not just the capital gain your broker shows.

This automation isn't just convenience. It's preventing costly mistakes in position management and ensuring accurate tax reporting at year-end.

Tax Reporting Complexity

Speaking of taxes, the wheel strategy creates significant record-keeping requirements:

- Each option trade is a separate taxable event

- Assignment is a taxable event (though loss/gain isn't realized until shares sold)

- Every covered call that expires or gets closed is a taxable event

- Rolls create two taxable events (close old position, open new position)

By the end of the year, a single wheel position that went through full cycles might generate 10-15 taxable events. Multiply that by 5-10 positions, and you're looking at 50-150 transactions to report accurately.

Professional tracking platforms export all trade data in formats compatible with tax software, and they calculate wash sales, holding periods, and adjusted cost basis automatically. This turns what would be days of year-end tax prep into minutes of data export.

Common Wheel Strategy Mistakes

Even experienced traders make these mistakes when running the wheel. Knowing what to avoid is often more valuable than knowing what to do.

Mistake 1: Chasing Premium Over Quality

High premium is seductive. When you see you can collect $5/share on a $50 put versus $1/share on a different $50 put, the choice seems obvious. But that $5 premium exists because the market perceives significantly higher risk.

Traders who chase premium end up holding shares in declining stocks, collecting small amounts of premium while suffering large capital losses. A stock that falls from $50 to $30 wipes out months of premium collection in a few days.

The fix: Always evaluate the stock first, premium second. If you wouldn't be happy owning this stock for a year at your strike price, don't sell the put regardless of premium.

Mistake 2: Selling Calls Below Cost Basis

You sold a $50 put, collected $2 premium (effective cost $48), and got assigned when the stock fell to $45. Now you're underwater by $3/share. The temptation is to sell a $46 call for quick premium, ensuring that if called away, you're only losing $2/share instead of $3.

The problem: You're locking in a loss and capping your recovery. If the stock rebounds to $55, you've sold your shares at $46 (realizing a $2/share loss) instead of $55 (realizing a $7/share gain).

The fix: Most successful wheel traders follow the rule "never sell calls below your adjusted cost basis unless the fundamental thesis has changed." If you still believe in the stock, give it room to recover. If you no longer believe in it, exit the position entirely rather than trying to salvage it with unfavorable calls.

Mistake 3: Overconcentration in Single Sectors

Running wheel strategies on AMD, NVDA, and INTC feels like diversification—three different stocks. But they're all semiconductors that correlate heavily. When the sector falls, all three positions move against you simultaneously.

The fix: Spread wheel positions across uncorrelated sectors. Combine tech with consumer staples, financials, healthcare, and broad market ETFs. Sector diversification protects you from concentrated losses when specific industries face headwinds.

Mistake 4: Ignoring Earnings Dates

Options premiums spike right before earnings due to uncertainty about results. This makes selling options look attractive. However, earnings reactions can be violent and unpredictable—stocks can move 10-20% overnight regardless of whether results were "good" or "bad."

If you're holding a short put when a stock gaps down 15% on earnings, you're facing immediate assignment at prices far above current market value. If you're holding a covered call when a stock gaps up 20%, you're watching profit potential evaporate as your shares get called away at your strike.

The fix: Check earnings dates before selling any option. If earnings fall within your option period, either choose a different expiration or accept the elevated risk consciously. Many wheel traders simply avoid selling new positions within 2 weeks of earnings.

Mistake 5: Not Having a Loss-Cutting Rule

The wheel strategy doesn't have built-in stop losses like directional trading. You can theoretically hold a losing position indefinitely, selling covered calls at strikes above your cost basis while the stock trades 40% below it, hoping for eventual recovery.

This hope-based approach ties up capital in losing positions for months or years. Meanwhile, that capital could be deployed in new opportunities with better odds.

The fix: Establish a maximum loss rule. Many traders use "if I'm down 25-30% on the position, I exit regardless of unrealized loss." This rule forces you to recognize when a thesis is wrong and redeploy capital into better opportunities. Yes, sometimes the stock recovers after you cut the loss—but more often, cutting losses early protects you from catastrophic account drawdowns.

Advanced Wheel Strategy Variations

Once you've mastered the basic wheel mechanics, several variations allow you to adjust the strategy to market conditions and personal preferences.

The Aggressive Wheel

Standard wheel strategy sells puts at 30-delta strikes (30% probability of assignment). The aggressive wheel sells closer to 40-50 delta (higher assignment probability) to maximize premium collection.

This variation suits traders who:

- Actually want to own the underlying stocks

- Have conviction the stocks will recover from any short-term drops

- Prioritize premium income over avoiding assignment

- Are comfortable with higher assignment frequency

The trade-off is clear: More premium collected, but higher probability of holding stocks through declines. This variation works best in sideways to moderately bullish markets on quality names you genuinely want to own.

The Dividend Wheel

This variation focuses exclusively on dividend-paying stocks with reliable distributions. You're stacking three income streams: put premiums, covered call premiums, and dividend payments when assigned.

Target stocks like:

- Dividend aristocrats (25+ years of rising dividends)

- Utilities and consumer staples

- Financially strong companies with 3%+ yields

The dividend wheel generates lower option premiums (due to lower volatility), but the combined income from all three sources and the higher quality of underlying stocks makes it appealing to conservative income-focused traders.

Important timing note: Be aware of ex-dividend dates when managing covered calls. If your call is in the money approaching ex-dividend, it might get exercised early so the long call holder can capture the dividend.

The ETF Wheel

Rather than wheeling individual stocks, this variation runs the strategy exclusively on broad market ETFs like SPY, QQQ, or IWM.

Benefits:

- Diversification eliminates single-stock risk

- Extreme liquidity in ETF options (tight spreads, easy to adjust)

- No earnings surprises or company-specific disasters

- Options are cash-settled, simplifying accounting

Drawbacks:

- Lower premiums due to lower volatility

- Less opportunity for stock selection edge

- Correlation to overall market means all positions move together

The ETF wheel works well for traders who want the wheel strategy's income mechanics without single-stock selection risk.

The Covered Strangle (Advanced)

Instead of just selling calls after assignment, experienced traders sometimes sell both calls and puts on assigned positions (covered strangle). You own 100 shares and simultaneously sell an out-of-the-money call and an out-of-the-money put.

This collects premium on both sides but creates more complex risk management:

- If the stock rises, your shares get called away (standard wheel)

- If the stock falls, you get assigned on the put, doubling your position to 200 shares

- If the stock stays in the range, both options expire worthless and you keep both premiums

This variation is only appropriate for traders who:

- Have enough capital to potentially double positions

- Are genuinely comfortable owning 200 shares at the put strike

- Can monitor and manage increased complexity

Tools and Resources

Running a successful wheel strategy requires the right combination of analytical tools, data sources, and tracking systems.

Essential Screening Capabilities

You need to scan the market for wheel-appropriate opportunities efficiently. Manual ticker-by-ticker screening simply doesn't scale once you're looking at more than 30 stocks.

Effective screeners filter for:

- Implied volatility rank/percentile (identify elevated premium)

- Option liquidity (volume and open interest)

- Stock fundamentals (quality scores, dividend history)

- Strike prices at target deltas (30-delta puts, etc.)

- Upcoming earnings dates

Generic options screeners like ThinkorSwim and TradeStation can do this, but they're painfully slow—often taking 5-10 minutes to scan just 100 tickers with full options chain data. Real-time screening tools purpose-built for premium collection strategies scan 500+ tickers in under a minute, letting you identify opportunities while they're still actionable.

Position Management Requirements

Once you're running 5+ wheel positions, you need systematic tracking:

Must-have features:

- Automatic cost basis calculation through complete wheel cycles

- Expiration calendar showing all upcoming dates

- P&L tracking per position and aggregated across portfolio

- Alert system for positions needing attention (approaching expiration, hitting profit targets)

- Roll tracking (cumulative premium across multiple rolls)

Nice-to-have features:

- Portfolio-level Greeks (aggregate delta, theta exposure)

- Sector concentration analysis

- Historical performance metrics by stock, strategy, timeframe

- Tax reporting exports

This is exactly why platforms like QuantWheel exist—it's purpose-built for traders running wheel strategies at scale. The automatic cost basis adjustments alone save hours of manual spreadsheet updates and prevent the calculation errors that lead to poor management decisions.

Educational Resources

Books:

- "The Complete Guide to Option Selling" by James Cordier (covers premium collection philosophy)

- "Trading Options Greeks" by Dan Passarelli (understanding position Greeks for better management)

Communities:

- r/thetagang (Reddit community specifically for premium collection strategies)

- r/options (broader options trading discussions)

Data Sources:

- CBOE volatility data for understanding market conditions

- Barchart for options chain data and unusual activity

Frequently Asked Questions

(Note: These are intentionally different from the FAQ section above, providing deeper technical answers)

How do you adjust the wheel strategy for bear markets?

During sustained downturns, consider these adjustments: 1) Reduce position sizes by 30-50% to preserve capital, 2) Sell puts at lower deltas (20-25 instead of 30) to reduce assignment probability, 3) Focus on defensive sectors like utilities and consumer staples that hold up better, 4) Keep larger cash reserves (50-60% instead of 30-40%), and 5) Consider pausing new put sales until market stabilizes. The wheel works in bear markets, but more defensive positioning is prudent.

Can you run the wheel strategy in a retirement account?

Yes, but your account needs approval for Level 2 or 3 options trading (varies by broker). Cash-secured puts and covered calls are typically allowed in IRAs because they're defined-risk strategies. However, portfolio margin isn't available in retirement accounts, so you'll need full cash secured for every put. This limits how many positions you can run simultaneously. Some brokers (like Fidelity and Schwab) are more permissive with retirement account options than others.

What happens if a stock gets delisted while I'm in a wheel position?

If you're holding a short put when delisting is announced, your put may be exercised immediately, forcing assignment before you can react. If you're holding shares and covered calls, the calls will typically be adjusted based on the delisting terms (merger, bankruptcy, etc.). This is why stock quality matters—financially strong companies with solid businesses rarely face surprise delistings. Avoid wheeling speculative small-caps where delisting risk is elevated.

How do implied volatility changes affect open wheel positions?

Rising IV after you've sold options helps you—it increases the value of buying back the option if you want to close early. Falling IV (like post-earnings volatility crush) hurts you—it makes rolling more expensive because you're buying back at deflated prices and selling new options at deflated premiums. This is why many traders avoid selling options right before earnings when IV is artificially elevated—the inevitable post-earnings IV crush makes position management more difficult.

Should you ever take assignment early if a put is deep in the money?

Generally no, because time value remaining in the option means you'll give up premium by accepting early assignment. However, if the stock has declined significantly and you want to start selling covered calls immediately rather than waiting for put expiration, early assignment (by purchasing the put to close) might make sense. Calculate whether the additional covered call premium you could collect by taking assignment early exceeds the time value you'd forfeit on the put.

Conclusion: Building Your Wheel Strategy

The options wheel strategy offers a systematic approach to generating income from the options market without requiring perfect market timing or directional predictions. By selling cash-secured puts on quality stocks you're willing to own, accepting assignment when it occurs, and selling covered calls until shares are called away, you create a repeatable cycle that profits in multiple market scenarios.

Success with the wheel strategy comes down to three fundamentals:

Stock selection matters more than options tactics. Choose quality companies with solid fundamentals, reasonable valuations, and adequate options liquidity. The perfect strike price on a mediocre stock won't save you from poor selection.

Position sizing protects you from catastrophic losses. Limit exposure to any single name, maintain cash reserves for unexpected opportunities, and scale position sizes based on conviction levels. Risk management isn't exciting, but it's what separates sustainable long-term returns from one-bad-trade account destruction.

Systematic tracking prevents costly mistakes. As you scale beyond 2-3 positions, manual tracking becomes error-prone. Professional tools built specifically for premium collection strategies—like QuantWheel—automate the tedious tracking, cost basis adjustments, and performance reporting that ensure accurate decision-making.

The wheel strategy isn't flashy. It won't double your account in a month. It's the options trading equivalent of Warren Buffett's investing philosophy: boring, systematic, and profitable over time.

If you're ready to implement the wheel strategy with professional-grade tracking and management tools, QuantWheel was built specifically for traders like you.

Conservative. Consistent. Boring. Profitable.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The wheel strategy can result in significant losses if the underlying stocks decline substantially. Assignment is part of the strategy, but it exposes you to full downside risk on the underlying shares. Options sold may expire worthless (favorable) or be exercised against you (potentially unfavorable depending on market conditions). Individual results vary significantly based on market conditions, execution quality, stock selection, and timing.