Author: David Romic - retail options trader and active member in the options trading communities on Reddit (u/thedavidromic). I share wheel strategy setups, trade management, and lessons learned from real positions.

If you're looking for advice on your specific situation, feel free to scroll down and find a scenario you need help with. Keep in mind that this text mainly focuses on advice for rolling in the wheel strategy.

Understanding What "Rolling" Actually Means

Rolling an option means simultaneously closing your current position and opening a new one, typically at a later expiration date.

When you roll, you're buying back the option you sold (closing it) and simultaneously selling a new option with a different expiration and possibly a different strike price.

Let's take an example - if you sold a $50 put expiring in January and the stock drops to $48, you could "roll" by buying back the previous trade (that January $50 put) and simultaneously make a new trade, selling a February $50 put (or February $49 put for example).

By doing this, you're extending the timeline of your trade and giving the stock more time to recover.

In short, the mechanics are straightforward, buy back the old trade and sell a new one to give yourself more time (expanding the DTE) or more room for the stock to go up (changing the strike price).

Knowing WHEN to roll is where traders, but only because they lack experience so let's solve that.

TLDR: When to Roll Options

Roll options when you can collect net credit (premium received > cost to close) AND one of these conditions is true:

For LOSING positions (option is in-the-money against you):

- You have 14-21 days until expiration

- You still believe in the stock long-term and want to avoid assignment

- The net credit improves your breakeven by at least 2-3%

- Example: You sold a $50 put, stock is at $48. Rolling to next month's $50 put costs you $220 to close but collects $280 in new premium = $60 net credit. Your new breakeven from this improves from $48 to $47.40.

For WINNING positions (option is out-of-the-money, profitable):

- You've captured 50-80% of maximum profit from a trade with original 45 DTE

- There are 21+ days until expiration (time decay is slow)

- You're confident in the stock staying in your favor

- Example: You sold a $50 put for $200, it's now worth $40 with 25 DTE (out of 45 DTE from your trade) . You've captured $160 (80%). Rolling to next month collects $180 new premium minus $40 cost for rolling = $140 net credit instead of waiting for the last $40.

Don't roll if: Net debit required, stock fundamentals changed negatively, you need capital elsewhere, or transaction costs exceed benefits.

When to Roll Losing Positions (In-the-Money Against You)

In-the-money trade example and it's best rolling solutions:

The Assignment Question Comes First

Before you even think about rolling, ask yourself: "Do I actually want to own this stock at the strike price?"

If the answer is yes, then don't roll—just take assignment.

This is the most critical advice because it ties in your stock outlook and you're not solely focusing on a "losing trade".

The wheel strategy works best when you're willing to own the underlying stock. Assignment isn't a failure, it's part of the plan.

If the answer is no—maybe the stock's fundamentals deteriorated, or it no longer fits your portfolio—then rolling or closing the position makes sense.

The Best Time to Roll: 14-21 Days to Expiration

For the wheel strategy, the optimal window to roll losing positions is when you have 14-21 days until expiration if you're practicing the wheel strategy. Here's why:

Too early (30+ DTE): Your current option still has significant value, making it expensive to close. The stock might still recover on its own.

Too late (< 7 DTE): Your option has little extrinsic value left. The new option you're rolling to won't collect enough premium to justify the transaction costs.

Just right (14-21 DTE): Your current option has lost most extrinsic value but isn't yet deeply in-the-money. The new option still has good premium available.

Calculate the Net Credit

This is non-negotiable: you must roll for a net credit in the wheel strategy.

The math:

- Premium collected from new option (the one you're selling)

- Minus: Cost to close current option (the one you're buying back)

- Equals: Net credit

If the result is positive, you're rolling for credit. If negative, you're rolling for a debit—which means you're paying to extend a losing trade. That's rarely a good idea.

Example scenario:

- Original trade: Sold $50 CSP for $1.50 premium ($150)

- Current situation: Stock at $47, option worth $3.20 with 15 DTE

- Rolling option: Next month's $50 put trading at $3.80

Roll calculation:

- Cost to close current: $3.20 (−$320)

- Premium from new option: $3.80 (+$380)

- Net credit: $0.60 ($60)

You'd receive $60 to extend your position by 30 days. That's a roll for credit—it makes sense to consider.

The main problem people struggle with is the adjusted cost basis.

Your broker will probably show your original position being down $170 ($320 current value minus $150 you collected from the example). After the roll, you'll have collected a total of $210 in premium ($150 + $60).

The problem: You need to track this manually through the full cycle of the wheel strategy. Solution: QuantWheel automatically tracks your adjusted cost basis and net premium through rolls and assignments and bunch of other stuff.

Here's an

Consider Strike Adjustments

When rolling, you don't have to keep the same strike. You have three options:

1. Roll out in time, same strike (most common)

- Maintains your original thesis

- Gives stock more time to recover

- Example: $50 put → next month's $50 put

2. Roll out AND up (for puts) / down (for calls)

- Gives stock more room to recover

- Collects less premium

- Improves probability of success

- Example: $50 put → next month's $49 put

3. Roll out AND down (for puts) / up (for calls)

- More aggressive, maintains premium

- Increases assignment risk

- Only if very bullish

- Example: $50 put → next month's $51 put

Most wheel traders stick with option 1 (same strike) or option 2 (more conservative strike) when rolling losing positions.

The Two-Roll Limit

Here's a practical guideline: don't roll the same position more than twice.

If you've rolled twice and the stock is still working against you, the market is telling you something. At this point:

- Take assignment and sell covered calls, or

- Close the position and accept the loss

- Move on to better opportunities

Continuously rolling a losing position (called "rolling and hoping") ties up mental energy and capital in a declining stock. It's often better to accept the loss and redeploy capital elsewhere.

When to Roll Winning Positions (Out-of-the-Money, Profitable)

The 50% Rule and Its Limitations

Many wheel traders follow the "50% rule": close positions when you've captured 50% of maximum profit.

The logic is sound: if you sold an option for $2.00 ($200) and it's now worth $1.00 ($100), you've captured $100 of the $200 maximum profit. Time decay slows significantly after this point, so you're better off closing and opening a new position.

But there's a problem: what if there are only 7 days until expiration? Closing costs transaction fees, and you'll pay bid-ask spreads twice (once to close, once to open new).

This is where rolling winning positions makes more sense than closing and opening separately.

The Optimal Rolling Window: 21+ DTE with 50-80% Profit Captured

Roll winning positions when:

- You've captured 50-80% of maximum profit, AND

- You still have 21+ days until expiration, AND

- You can roll for credit to the next cycle

Example scenario:

- Original trade: Sold $45 CSP for $1.80 ($180), 45 DTE

- Current situation: 24 DTE remaining, option worth $0.40 ($40)

- Profit captured: $140 / $180 = 78%

You have three choices:

Option A: Hold until expiration

- Potential gain: remaining $40

- Time: 24 days

- Return: 22% of original premium over 24 days

Option B: Close and open new position

- Transaction costs: 2 commissions + 2 bid-ask spreads

- Potential gain: new $1.70 premium

- Time: 45 days new cycle

Option C: Roll to next cycle

- Close current for $0.40, sell next cycle for $1.80

- Net credit: $1.40 ($140)

- One transaction, lower costs

- Continue exposure in stock you like

Option C (rolling) typically wins because you maintain continuity with lower transaction costs than closing and reopening separately.

Calculate Time-to-Money Efficiency

When deciding whether to roll a winner, calculate your return per day:

Current position:

- Days remaining: 24

- Profit remaining: $40

- Return per day: $40 / 24 = $1.67/day

Rolling to new position:

- Net credit from roll: $140

- Days in new position: 30 (if rolling 30 DTE)

- Return per day: $140 / 30 = $4.67/day

Rolling generates nearly 3x the daily return in this example. That's a clear signal to roll rather than wait.

Don't Roll Just to Roll

Here's where discipline matters: only roll winning positions if the new cycle offers attractive premium.

If implied volatility has collapsed (IV Rank below 20), or if the stock price has moved significantly in your favor, the new premium might be weak. In these cases, close the position, take your profit, and look for a better opportunity elsewhere.

Rolling winners works best in stocks with:

- Consistent IV rank above 30

- Stable or improving fundamentals

- Technical setups that support continued exposure

- Liquidity (tight bid-ask spreads)

Advanced Rolling Strategies for the Wheel

The Diagonal Roll (Time + Strike Adjustment)

A diagonal roll changes BOTH expiration and strike price. This is useful when your outlook on the stock has changed slightly.

For puts (you sold a cash-secured put):

- Rolling out and UP (higher strike) → More conservative, less premium

- Rolling out and DOWN (lower strike) → More aggressive, more premium

For covered calls (after assignment):

- Rolling out and DOWN (lower strike) → More conservative, more premium, easier to get called away

- Rolling out and UP (higher strike) → More aggressive, less premium, hold shares longer

Example: You sold a $50 covered call, stock rallied to $52. You want to keep shares longer.

- Close current $50 call

- Sell next month's $53 call

- Collect net credit while giving stock room to run

The Calendar Roll (Same Strike, Different Expiration)

This is the standard roll most wheel traders use: keep the same strike, extend the expiration.

Best for:

- Maintaining your original thesis

- When strike is still appropriate

- Simplest execution

Example: Your $45 put → next month's $45 put

Rolling Across Earnings

Earnings announcements create a dilemma: IV typically spikes before earnings, but the event creates risk.

Strategy 1: Roll before earnings

- Close your position before earnings

- Roll to post-earnings expiration

- Avoid earnings volatility

- Miss the IV spike premium

Strategy 2: Roll through earnings

- Keep your position through earnings

- Collect elevated IV premium

- Accept earnings risk

- Appropriate if you'd be comfortable owning at the strike

Most conservative wheel traders use Strategy 1, rolling before earnings to avoid overnight gap risk.

When NOT to Roll (Important Exceptions)

1. The Stock Fundamentals Changed

If the company reports deteriorating fundamentals—declining revenue, concerning guidance, competitive pressures—don't roll just to avoid assignment.

Take the loss and move on. Rolling ties up your capital in a weakening position.

2. You Need Capital for a Better Opportunity

Opportunity cost matters. If you have a significantly better opportunity available, close your current position (even at a small loss) and redeploy capital to the better trade.

Don't stay in a mediocre position just because you can roll it.

3. The Roll Requires a Net Debit

This is non-negotiable for wheel traders: never roll for a net debit unless you have a very specific strategic reason.

Rolling for debit means you're paying to extend a losing position. That's speculating on a recovery, not executing a systematic wheel strategy.

4. Transaction Costs Exceed Benefits

If the net credit from rolling is $10, but you'll pay $6 in commissions and another $8 in bid-ask spread costs, you're netting $-4. Don't roll.

This commonly happens on small positions or in illiquid options. Calculate total costs before executing.

5. You've Already Rolled Twice

As mentioned earlier, two rolls is typically the limit. Beyond that, you're "rolling and hoping" instead of trading systematically.

Accept the outcome (assignment or loss) and move to a fresh opportunity.

The Mechanics: How to Actually Execute a Roll

Use a "Closing Roll" Single Order

Most brokers offer a "roll" order type that executes both legs simultaneously:

- Buy to close current position

- Sell to open new position

This is preferable to executing two separate orders because:

- You get filled as a single transaction

- Market makers see your intent and provide better pricing

- You avoid "leg risk" (getting filled on one side but not the other)

In Think or Swim (TOS)

- Right-click your existing position

- Select "Create Closing Roll"

- Choose new expiration date

- Adjust strike if desired

- Review net credit/debit

- Submit order

In Tastytrade

- Select your position

- Click "Roll"

- Choose new expiration

- Select new strike

- Review net credit

- Submit

In Robinhood

Robinhood doesn't have a native roll function. You must:

- Close existing position manually

- Open new position manually

- Calculate net credit yourself

- Execute as two separate orders (less ideal)

Order Types for Rolling

Limit Order (recommended):

- Set the minimum net credit you'll accept

- Order fills only if you get your price or better

- Protects against poor execution

Market Order (avoid):

- Fills immediately at current market price

- Can result in poor fills, especially in illiquid options

- Only use in highly liquid options (SPY, QQQ, etc.)

Roll Decision Calculator: A Simple Framework

Here's a step-by-step framework for deciding whether to roll:

Step 1: Assess Your Position

Is it winning (OTM, profitable) or losing (ITM, unprofitable)?

Step 2: Check Days to Expiration

- 30+ DTE: Too early, wait

- 14-21 DTE: Prime rolling window

- < 7 DTE: Often too late unless high IV

Step 3: Calculate Net Credit

- Price to close current position: $____

- Premium from new position: $____

- Net credit (or debit): $____

If net debit, stop here. Don't roll.

Step 4: Evaluate Fundamentals

Has anything changed with the stock?

- Earnings disappointment?

- Sector weakness?

- Technical breakdown?

If yes, consider taking the loss instead of rolling.

Step 5: Calculate New Breakeven

- Original strike: $____

- Total premium collected (including roll): $____

- New breakeven: Strike minus total premium

Is this breakeven acceptable given current stock price and outlook?

Step 6: Decision Matrix

| Condition | Losing Position | Winning Position |

|---|---|---|

| 14-21 DTE, net credit, fundamentals intact | Roll | N/A |

| 21+ DTE, 50-80% profit captured, net credit | N/A | Roll |

| Net debit required | Don't Roll | Don't Roll |

| Fundamentals deteriorated | Close or Take Assignment | Close |

| Need capital elsewhere | Close | Close |

| Already rolled 2x | Take Assignment or Close | N/A |

Real-World Examples: Rolling in Action

Example 1: Rolling a Losing Put

Setup:

- Sold AMD $110 put, 45 DTE, collected $3.50 premium ($350)

- Stock dropped to $106 after 30 days (15 DTE remaining)

- Current option value: $4.20

Analysis:

- Position is $4.20 - $3.50 = $0.70 underwater ($70 loss)

- 15 DTE is in the rolling window

- AMD fundamentals still intact, AI story remains strong

Roll options:

- Next month $110 put trading at $4.80

- Next month $108 put trading at $3.90

Option 1 calculation (same strike):

- Close current: -$4.20

- New premium: +$4.80

- Net credit: $0.60 ($60)

- New breakeven: $110 - $4.10 = $105.90

Option 2 calculation (lower strike):

- Close current: -$4.20

- New premium: +$3.90

- Net debit: -0.30(0.30 ( 0.30(-30)

- Don't roll to this strike, it's a debit

Decision: Roll to next month's $110 put for $0.60 credit. This gives AMD 30 more days to recover back above $110, and improves overall cost basis to $105.90.

Example 2: Rolling a Winning Put

Setup:

- Sold MSFT $380 put, 45 DTE, collected $5.00 premium ($500)

- Stock traded sideways, now at $385 after 21 days (24 DTE remaining)

- Current option value: $1.20

- Profit captured: $3.80 (76%)

Analysis:

- Position is 76% profitable

- 24 DTE still has time

- Rolling window is optimal (21+ DTE)

Roll option:

- Close current: -$1.20

- Next month's $380 put: +$4.80

- Net credit: $3.60 ($360)

Comparison:

- Hold until expiration: Collect remaining $1.20 over 24 days = $50/week

- Roll now: Collect $3.60 over next 30 days = $120/week

Decision: Roll to next month for $3.60 credit. This generates 2.4x more weekly return than holding the current position.

Example 3: When NOT to Roll

Setup:

- Sold SNAP $12 put, 30 DTE, collected $0.90 premium ($90)

- SNAP reports disappointing earnings, drops to $9.50

- Current option value: $2.60 with 15 DTE

- Next month's $12 put: $3.10

Analysis:

- Roll would collect: -$2.60 + $3.10 = $0.50 credit ($50)

- But fundamentals changed: growth slowing, guidance lowered

- Already down $170 on the position

Decision: Don't roll. Close the position for -$170 loss and move capital to a higher-conviction opportunity. The $50 credit from rolling doesn't justify staying in a deteriorating stock.

Tools and Technology for Rolling Decisions

Most Brokers: Manual Calculation Required

Standard broker platforms (Think or Swim, Tastytrade, Robinhood) show you:

- Current position P&L

- Option prices for different expirations

- Greeks

But they DON'T automatically:

- Calculate your net credit from rolling

- Track your adjusted cost basis through multiple rolls

- Show your real breakeven after rolls

- Aggregate premium collected across the cycle

You need spreadsheets or manual tracking to maintain this information across 10+ positions.

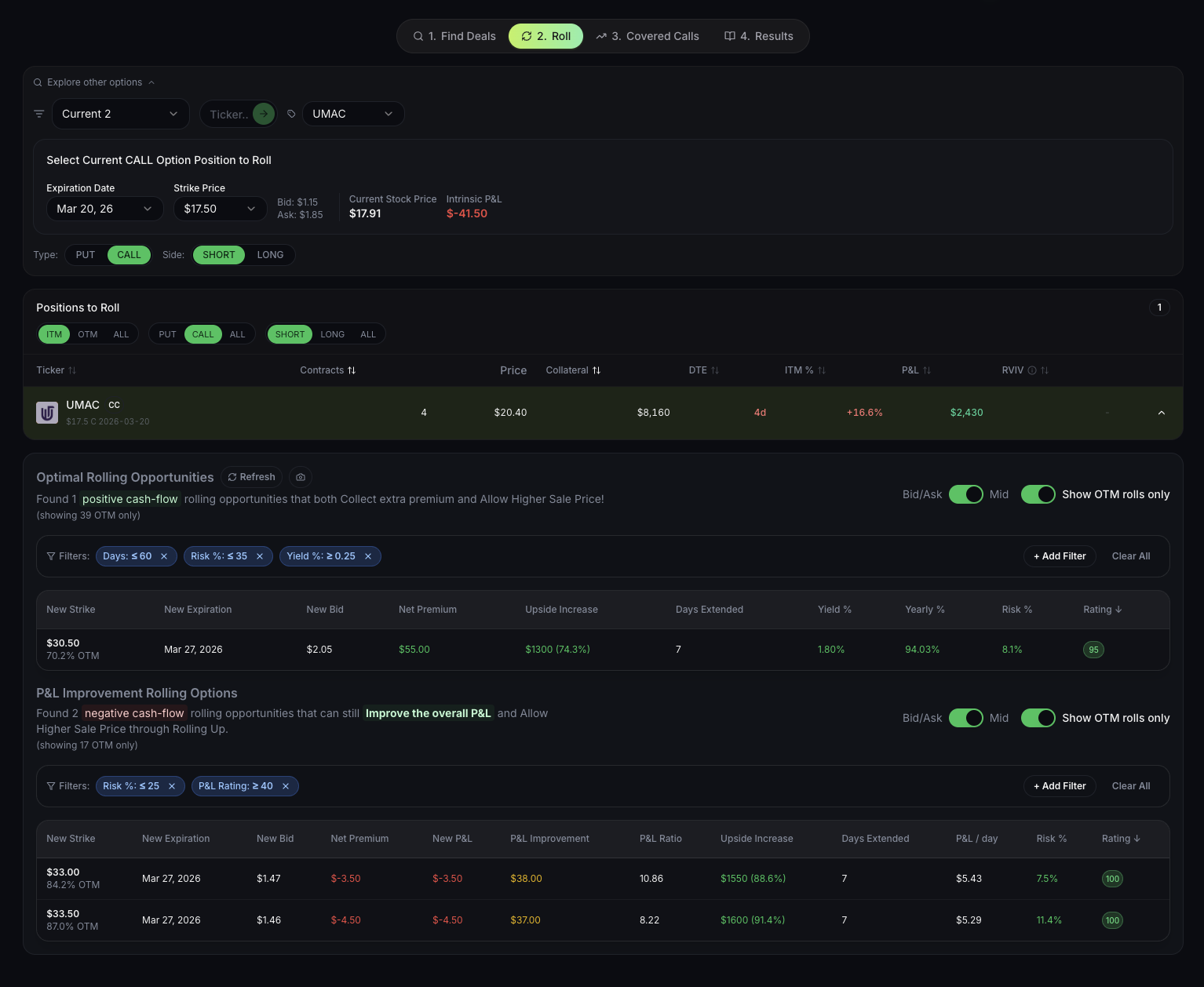

QuantWheel's Roll Assistant

This is exactly the problem QuantWheel solves. The Roll Assistant feature:

- Analyzes all possible roll options (different expirations and strikes)

- Calculates net credit for each option

- Shows your new breakeven for each roll

- Ranks options by return, time efficiency, or risk

- Automatically updates your cost basis when you execute

- Tracks total premium through complete wheel cycles

Example of what you see:

Current Position: AMD $110 Put, 15 DTE, -$70 P&L Roll Options: 1. Next week $110 put: +$150 net → New BE: $108.50 (Conservative) 2. Next month $110 put: +$60 net → New BE: $105.90 (Recommended) 3. Next month $108 put: -$30 net → DEBIT (Not Recommended) QuantWheel Recommendation: Roll to next month $110 put - Optimal credit-to-time ratio - Maintains thesis - 30-day extension for recovery

When managing 15 wheel positions, having this calculation automated for every position saves hours per week. You can see at a glance which positions are rollable, which should be closed, and which should be left alone.

Common Rolling Mistakes (And How to Avoid Them)

Mistake 1: Rolling Too Early

The problem: Rolling at 30+ DTE when your option still has significant value means paying a high cost to close.

Solution: Wait until 14-21 DTE for losing positions, or until 50%+ profit captured for winning positions.

Mistake 2: Rolling for a Debit

The problem: Paying money to extend a losing position is speculating, not systematic trading.

Solution: Only roll if you receive net credit. If a credit roll isn't available, close the position or take assignment.

Mistake 3: Rolling Without Checking Fundamentals

The problem: Mechanically rolling without reassessing the stock can trap you in deteriorating positions.

Solution: Before every roll, ask: "Would I enter this position fresh today at these terms?" If no, don't roll.

Mistake 4: Rolling Forever (Roll and Hope)

The problem: Continuously rolling the same losing position for months, hoping for recovery.

Solution: Maximum two rolls per position. After that, accept assignment or close.

Mistake 5: Ignoring Transaction Costs

The problem: Rolling for $20 net credit but paying $15 in commissions and spreads nets you only $5.

Solution: Calculate total costs before rolling. If net benefit is minimal, close and move on.

Mistake 6: Rolling in Illiquid Options

The problem: Wide bid-ask spreads destroy your net credit calculation.

Solution: Only roll options with tight spreads (typically < $0.10 spread on monthlies). If spreads are wide, close position separately.

Tax Implications of Rolling Options

Rolling Doesn't Reset Your Holding Period

When you roll an option, the IRS considers it a closing transaction and an opening transaction—two separate events.

For taxes:

- Your original option's P&L is realized when closed

- The new option starts fresh with a new holding period

- Premium from rolling is added to your basis

Short-Term vs Long-Term (Usually Not Relevant)

Options are almost always short-term capital gains/losses because:

- Few traders hold options > 1 year

- Most wheel positions cycle within 30-60 days

- Rolling resets the timeline anyway

Plan for short-term capital gains treatment on all wheel strategy trades.

Record Keeping is Critical

Every roll creates two tax events:

- Closing the old position (gain or loss)

- Opening the new position (new basis)

You must track:

- Date of original trade

- Premium collected on original

- Date of roll

- Cost to close original

- Premium collected on new position

- Date of final close or assignment

This gets complicated with 10+ positions rolling multiple times per year. Most traders use spreadsheets, but mistakes are common.

QuantWheel automatically logs every leg of every roll, generating tax-ready exports for your accountant at year-end. Every transaction is timestamped with premium collected, cost to close, and net credit for the complete audit trail.

The Rolling Decision Framework: Quick Reference

Use this flowchart for every rolling decision:

START HERE:

Is your position losing (ITM) or winning (OTM)?

→ LOSING (ITM):

- ❓ Do you still want to own the stock?

- YES → Take assignment, don't roll

- NO → Continue

- ❓ Is DTE between 14-21 days?

- NO → Wait or close

- YES → Continue

- ❓ Can you roll for net credit?

- NO → Close position or take assignment

- YES → Continue

- ❓ Are fundamentals still intact?

- NO → Close position

- YES → ROLL

→ WINNING (OTM):

- ❓ Have you captured 50-80% profit?

- NO → Hold longer

- YES → Continue

- ❓ Is DTE 21+ days?

- NO → Hold to expiration

- YES → Continue

- ❓ Can you roll for net credit?

- NO → Close position, look elsewhere

- YES → Continue

- ❓ Does new position offer good premium (IV still elevated)?

- NO → Close and redeploy capital

- YES → ROLL

Final Thoughts: Rolling as Part of Your System

Rolling options is a tool, not a strategy. It's most effective when used systematically within your wheel strategy framework:

Use rolling to:

- Extend time on positions you still believe in

- Avoid unwanted assignments when circumstances change

- Capture additional premium on winning positions

- Manage risk without closing positions unnecessarily

Don't use rolling to:

- Avoid taking losses on deteriorating stocks

- Chase a stock lower indefinitely

- Roll just because you can

- Delay inevitable assignments on positions you'd own anyway

The best wheel traders have clear rules for when they roll, and they follow them consistently. They roll for credit, within specific DTE windows, and only when fundamentals remain intact.

With 10+ positions in play, keeping track of roll timing, net credits, and adjusted cost basis across your portfolio becomes the challenge. Whether you track this in spreadsheets or use a specialized platform like QuantWheel, having a systematic approach to rolling decisions is what separates profitable wheel traders from those who struggle.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.