The wheel strategy - often just "the wheel" - is an options income strategy where a trader sells cash-secured puts on a stock they'd be willing to own, takes assignment if the put goes in the money, sells covered calls on the assigned shares, and repeats the cycle after the shares are called away. Each leg collects premium, which is the income the strategy is designed to generate.

What it is

The wheel has four stages. They run in a fixed order and repeat as long as you keep running the strategy on a given stock.

Stage 1 - Sell a cash-secured put (CSP). You set aside cash equal to 100 shares at the put's strike price and sell a put option. The premium is credited immediately. If the stock stays above the strike at expiration, the put expires worthless and you keep the premium.

Stage 2 - Assignment. If the stock closes below the strike at expiration, the put buyer exercises and you buy 100 shares at the strike. This is called being assigned. Your cost basis is the strike price minus every premium you've collected on this stock so far.

Stage 3 - Sell a covered call (CC). With 100 shares in hand, you sell a call option above your cost basis. Another premium is credited. If the stock stays below the call strike at expiration, the call expires worthless and you keep the premium and the shares.

Stage 4 - Called away. If the stock closes above the call strike at expiration, the call buyer exercises and your 100 shares are sold at the strike. This is called away. You go back to Stage 1 with the cash proceeds.

📸 SCREENSHOT: wheel-strategy-illustration.png

At every stage, premium is collected upfront. What determines whether the strategy is profitable over time is how the stock moves relative to the strikes you chose, plus how many premiums compound against your cost basis before you're called away.

When it matters

The wheel is designed for traders who want consistent options income on stocks they're comfortable owning. It suits stable or slowly-appreciating stocks. It works poorly on stocks in strong downtrends - the puts get assigned at higher strikes than the current price, and the covered calls collect less premium because implied volatility has shifted.

Three decisions drive the outcome:

- Which stock. You must be willing to own 100 shares at the strike. That's the hard filter. Everything else is optimization.

- Which strike. Closer to the money means more premium and higher assignment odds. Further out of the money means less premium and lower assignment odds.

- Which expiration. Shorter expirations decay faster and give you more decisions per year. Longer expirations reduce transaction overhead but tie up capital longer.

How QuantWheel uses this

Every feature in QuantWheel maps to a stage of the wheel:

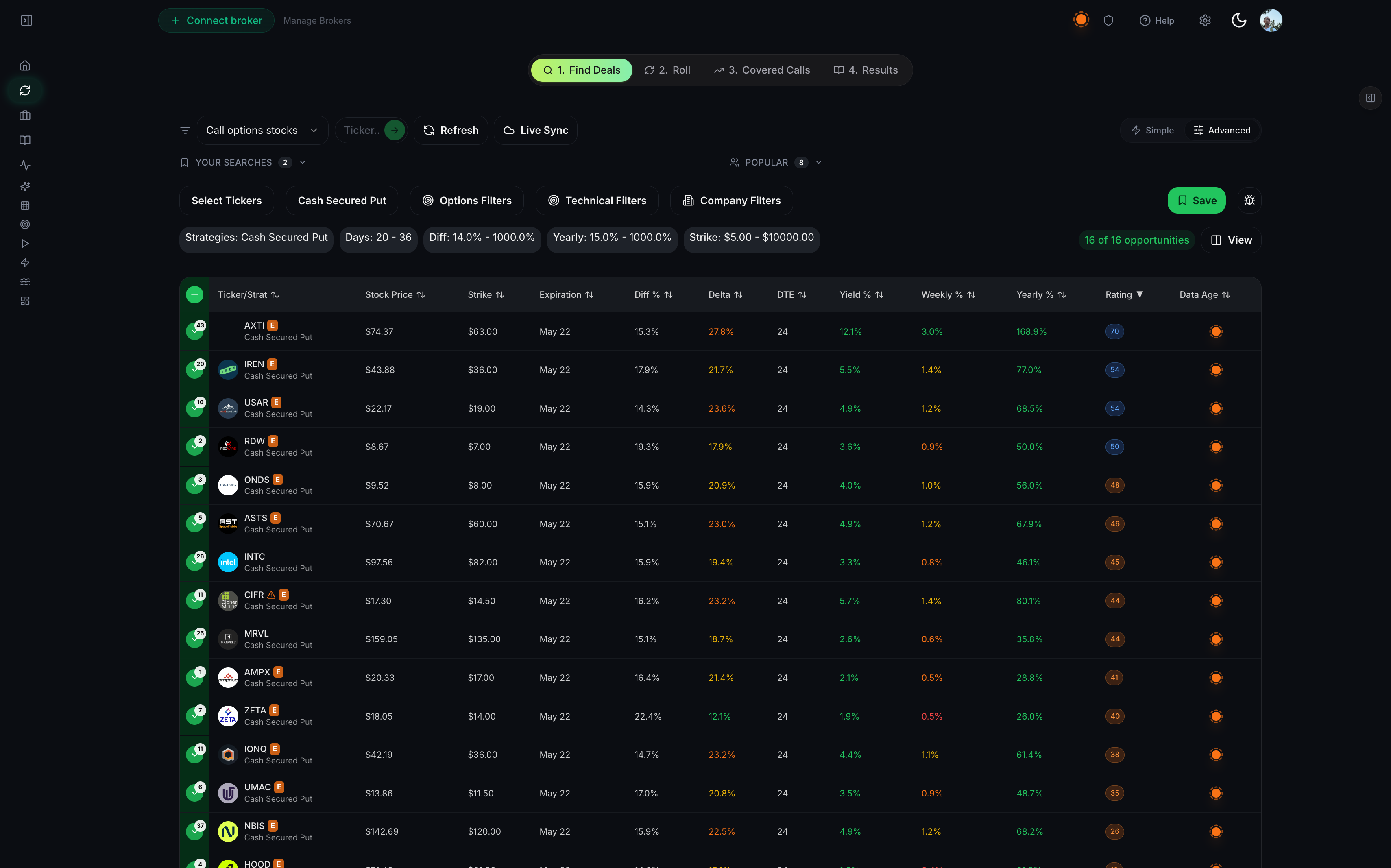

Find Deals (Wheel tab 1) screens the market for Stage 1 candidates - cash-secured puts that match your yield, delta, and rating thresholds.

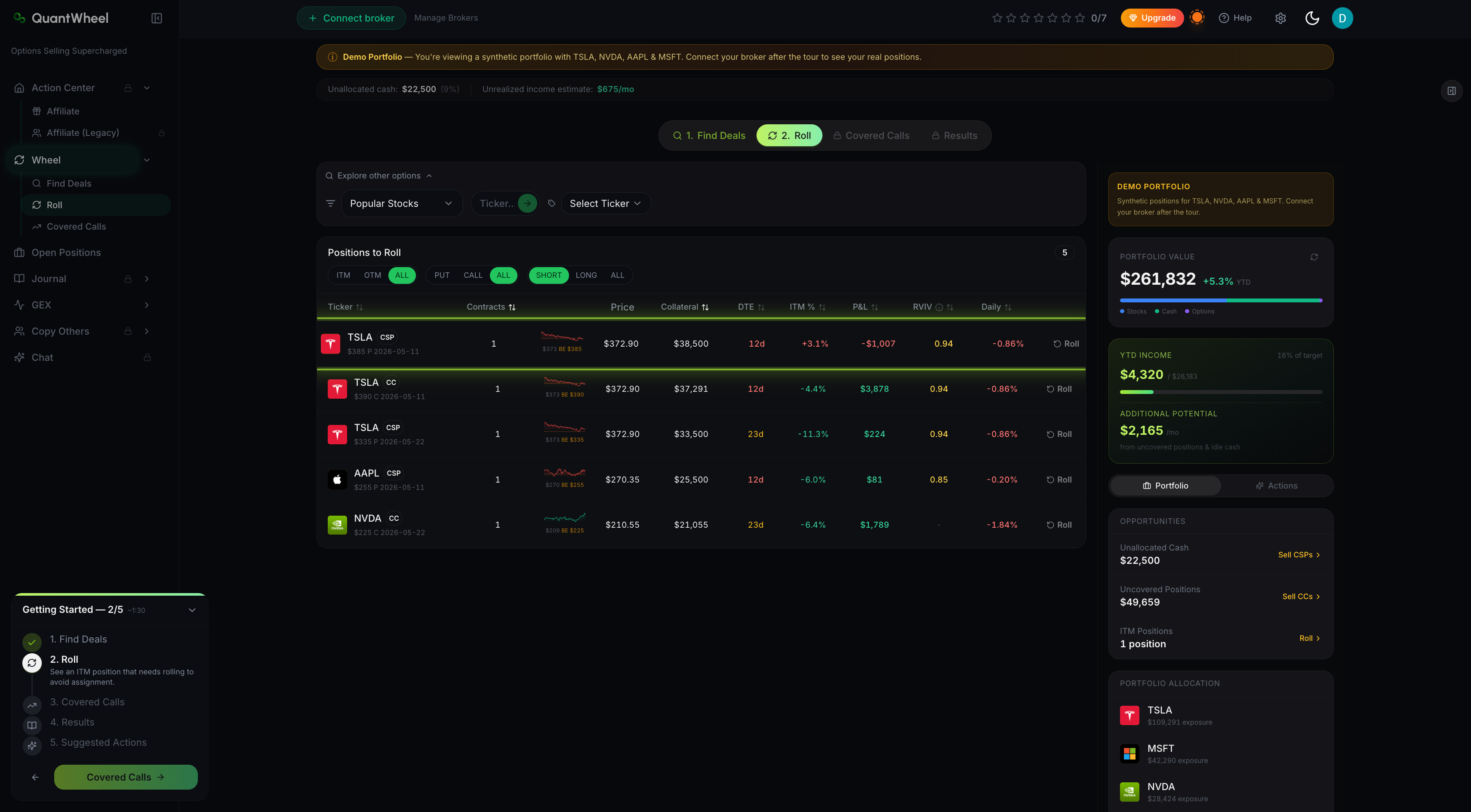

Roll (Wheel tab 2) surfaces positions from Stage 1 or Stage 3 that are going in the money and need to be rolled to avoid assignment or called-away. Clicking one of "problematic" positions expands it and shows optimal rolling suggested opportunities.

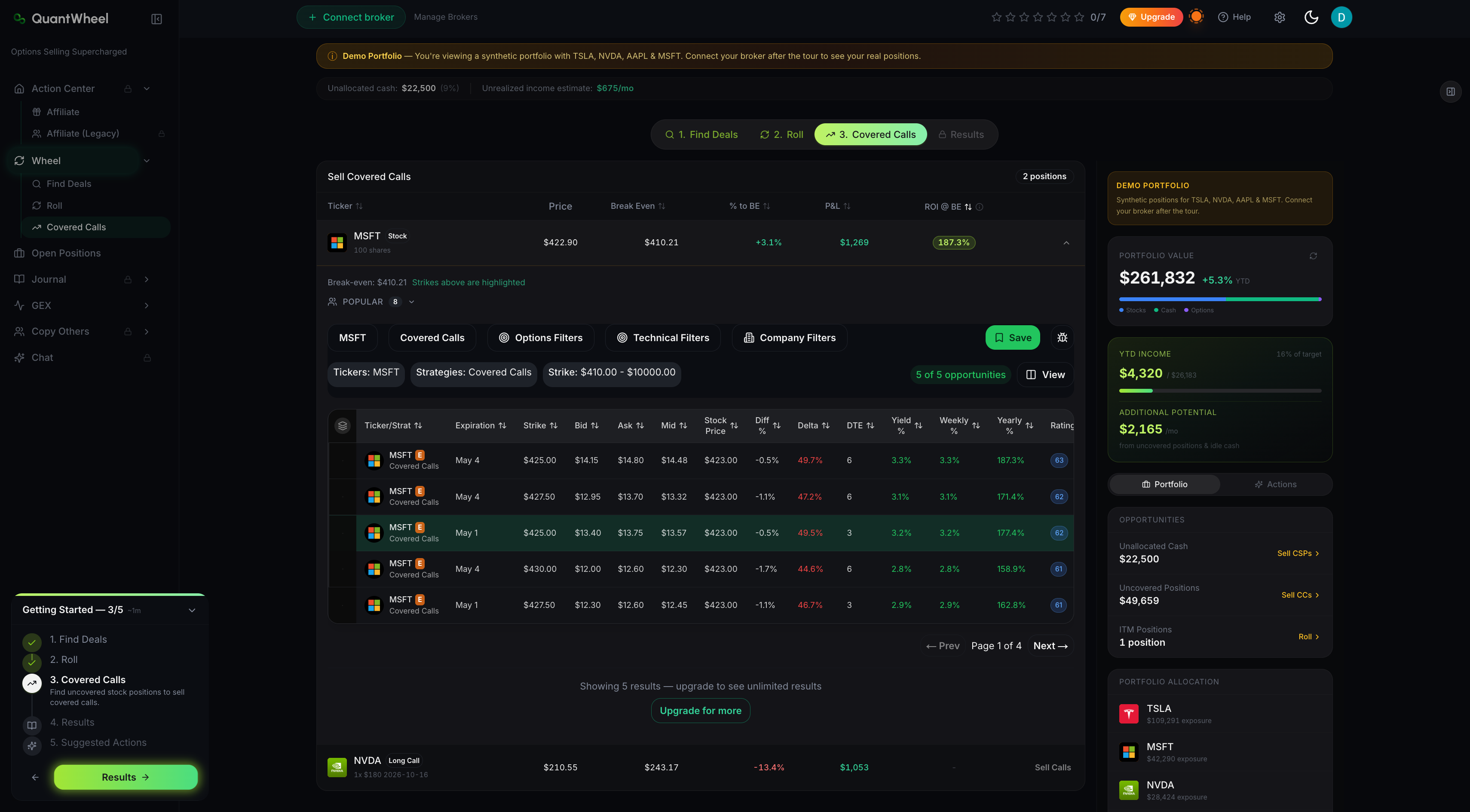

Covered Calls (Wheel tab 3) surfaces your own uncovered stock positions (Stage 3 candidates) and finds calls to sell against them.

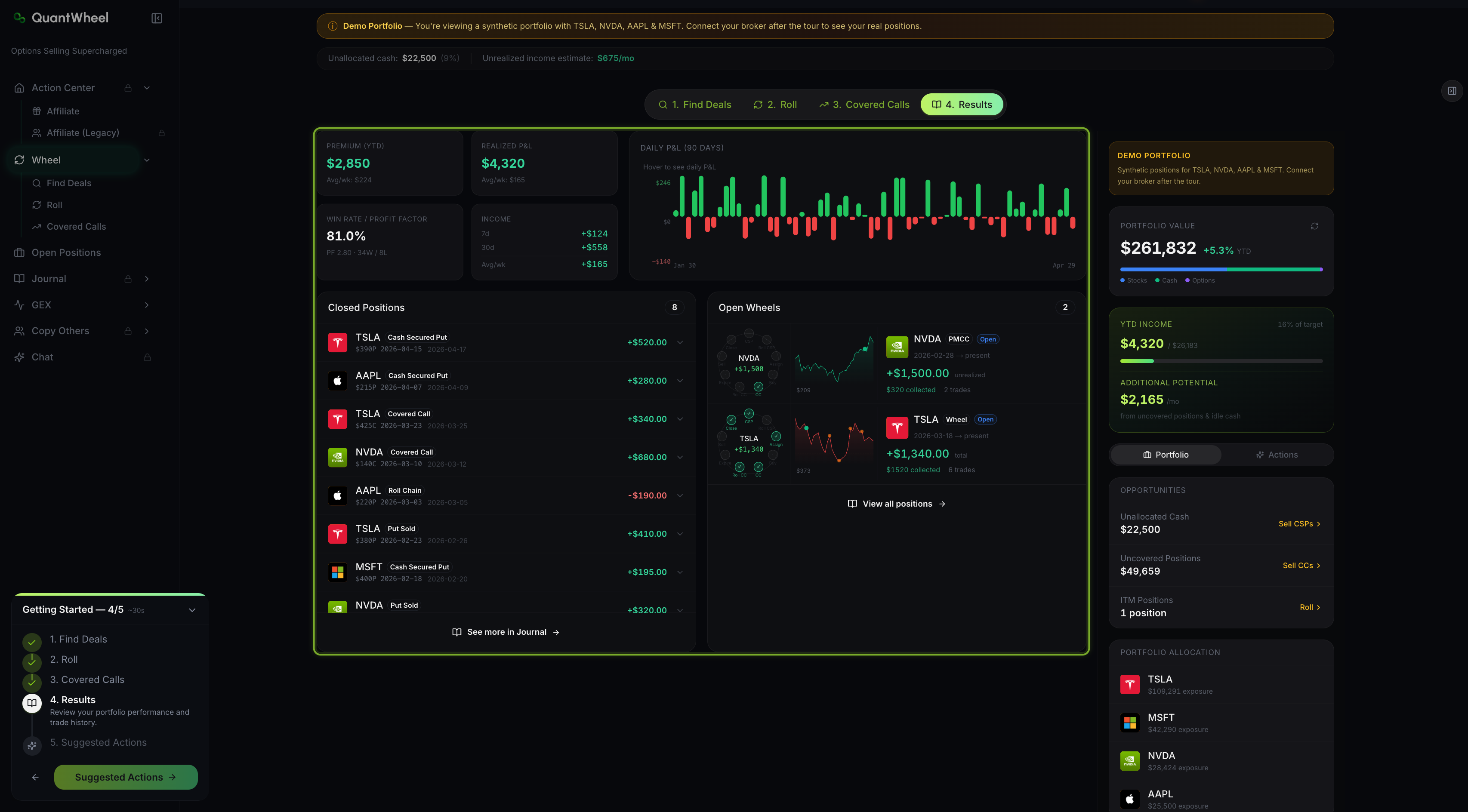

Results (Wheel tab 4) shows closed wheels and open wheels with premium, win rate, and P&L.

Open Wheels on the Action Center shows each in-progress position at its current stage in the cycle. You can see how it looks in previous screenshot.\

Journal → Per-Ticker tracks your Real Cost - the cost basis adjusted down by every premium you've collected on that stock. This is the number that matters across a full cycle, and it's what most spreadsheets get wrong after 5+ rolls.

Common misconceptions

"The wheel is set-and-forget."

It isn't. Rolls, assignments, earnings events, and ex-dividend dates all force decisions. The reason people run it through software instead of a spreadsheet is that the decisions compound - a tracker that handles 3 positions breaks at 15.

"The premium is the profit."

Premium is the income stream. The profit is premium minus any realized loss on the underlying shares if you're called away below cost. That's why Real Cost matters - it's the number you compare the call strike against to know whether a called-away scenario is a win or a wash.

"Assignment is a failure."

Assignment is a designed outcome of the strategy. The whole point of choosing a stock you'd be willing to own at the strike is that assignment is acceptable. What matters is whether your Real Cost after assignment is below the price you'd buy the stock at anyway.

"You need to predict direction."

The wheel works across a range of market conditions, not by predicting direction. It collects premium on time decay and implied volatility. It underperforms when the stock moves sharply against the position faster than rolling can recover - that's a risk, not a prediction requirement.

Related

- Understanding QuantWheel plans: Sandbox, GEX, and PRO

- How to connect your first broker and see your positions

Risk disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and is not investment advice.