Before comparing returns and risks, let’s clarify exactly what each strategy entails.

Buying Stocks: The Traditional Approach

When you buy stock, you pay the current market price and immediately own the shares. Your profit or loss depends entirely on price movement—if the stock rises, you gain; if it falls, you lose.

Your maximum profit is unlimited (theoretically, the stock could rise indefinitely), and your maximum loss is 100% if the company goes bankrupt.

This is the simplest, most straightforward investment approach. You can hold indefinitely, collect dividends if offered, and sell whenever you choose.

Selling Cash-Secured Puts: The Income Alternative

Selling a cash-secured put means you’re willing to buy a stock if it falls, for less, and get paid for it on top.

Here’s what “cash-secured” means: you must have enough cash in your account to buy 100 shares at the strike price. If you sell a $50 put, you need $5,000 in your account. This cash backs your obligation to buy the shares if assigned.

Two possible outcomes:

- Stock stays above strike price: The put expires worthless, you keep the full premium, and you can sell another put if desired

- Stock falls below strike price: You’re assigned and must buy 100 shares at the strike price, but your effective cost is reduced by the premium collected

The strategy appeals to investors who want to:

- Generate income while waiting for better entry prices

- Lower their cost basis compared to buying at current market prices

- Create systematic income from their cash positions

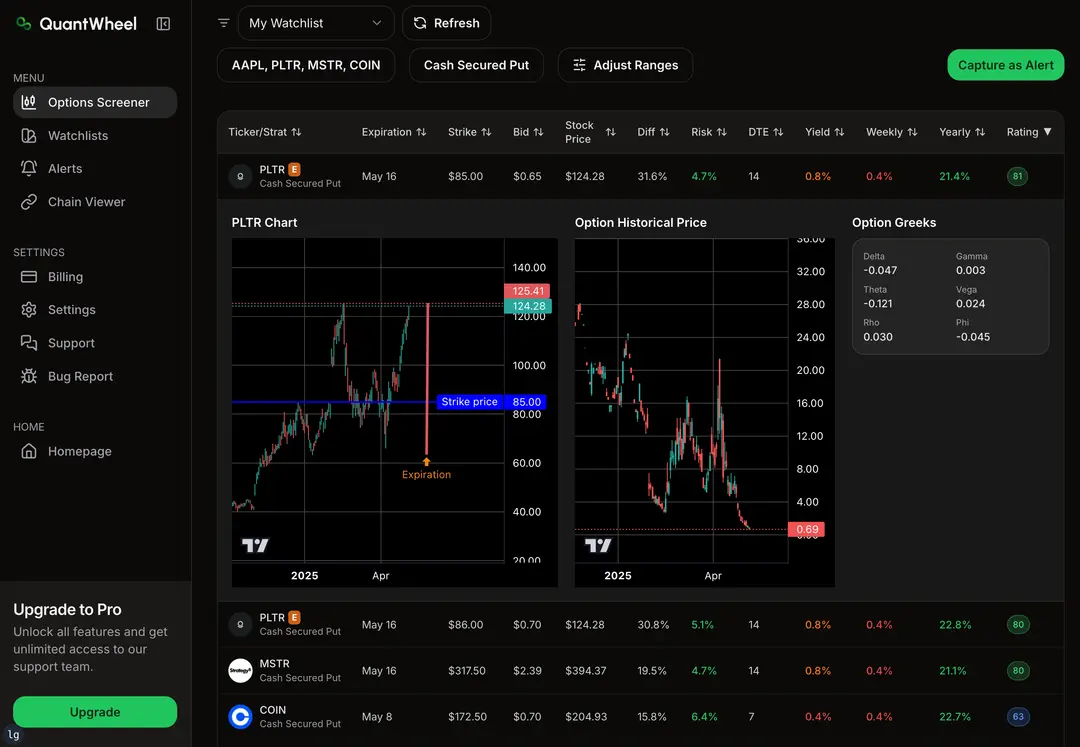

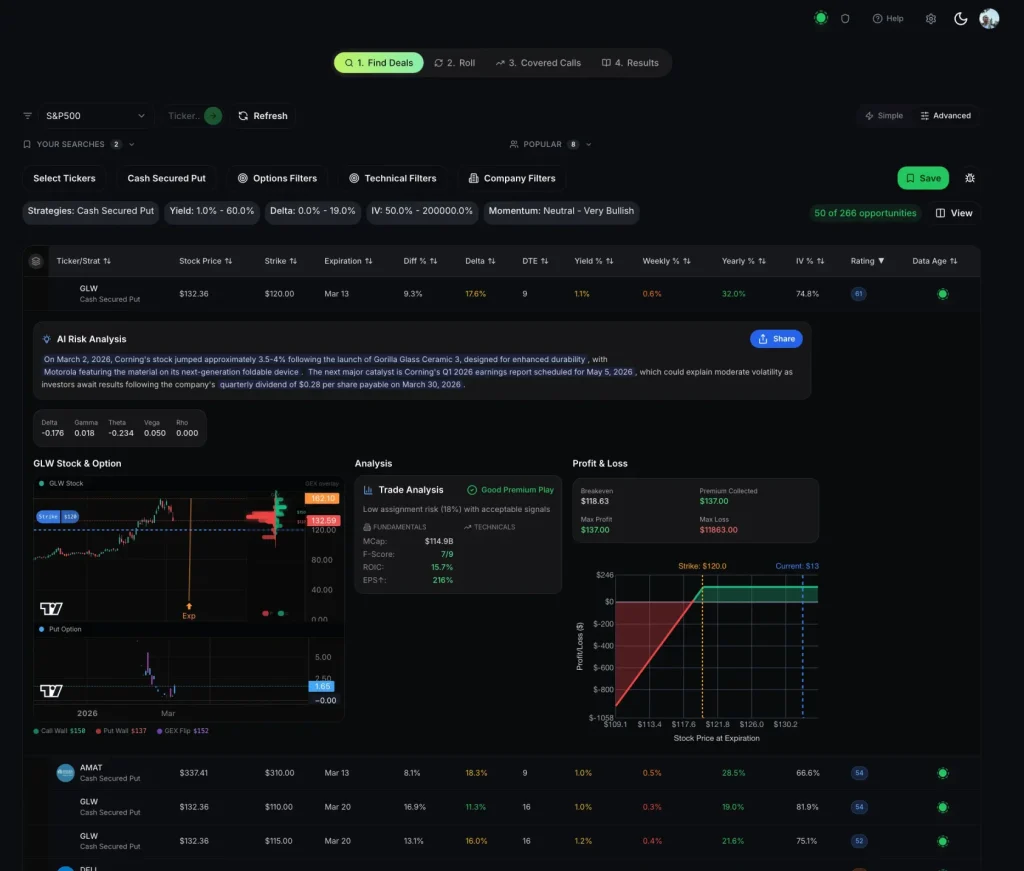

Here’s the income you can expect if you were to enter a cash – secured put on $GLW for example.

Look at more trades like this →

Capital Requirements: The Real Comparison

One common misconception is that selling puts requires less capital than buying stocks. This isn’t true for cash-secured puts.

Capital Breakdown

Buying 100 shares at $50:

- Required capital: $5,000

- Cash tied up: $5,000 until you sell

- Income generated: $0 (unless dividends)

Selling one $50 put (30 days, $2 premium):

- Required capital: $5,000 (cash-secured)

- Cash tied up: $5,000 for 30 days

- Income generated: $200 upfront (4% in 30 days)

The capital requirement is identical. The difference is what you get for that capital: immediate ownership versus obligation plus premium income.

Capital Efficiency Over Time

Where selling puts gains an edge is in repeat deployments. If the stock stays above your strike:

- Month 1: Sell $50 put, collect $200 premium, stock expires above $50

- Month 2: Sell another $50 put, collect $200 premium, stock expires above $50

- Month 3: Sell another $50 put, collect $200 premium, stock expires above $50

In this scenario, you’ve generated $600 (12% return over 90 days) without ever owning shares. The same $5,000 in cash produced income multiple times.

With stock ownership, your $5,000 would have generated profit only if the stock price increased during that period.

Risk Comparison: What Can Actually Go Wrong

Let’s be honest about the risks, because this is where a lot of content gets misleading.

Maximum Loss: Nearly Identical

Both strategies have similar maximum downside:

- Buying stock: Maximum loss is 100% if stock goes to zero

- Selling cash-secured put: Maximum loss is 100% minus premium collected

Example with $50 stock:

- Buy 100 shares at $50: Maximum loss = $5,000 if stock → $0

- Sell $50 put for $200: Maximum loss = $4,800 if stock → $0 (you lose $5,000 on assignment minus $200 premium kept)

The premium provides a tiny cushion, but both strategies are exposed to the same downside risk.

The Real Risk Difference: Assignment Timing

The meaningful difference is when you take on the risk:

Buying stock: You own shares immediately, so you’re exposed to downside from moment one

Selling puts: You don’t own shares unless assigned, so if the stock crashes quickly, you might not be assigned yet and can close the position for a loss smaller than owning shares would have generated

However, this is a minor distinction. If you’re selling cash-secured puts on stocks you genuinely want to own at the strike price, assignment should be viewed as a positive outcome (you’re buying at your target price minus premium).

Unlimited Upside vs. Capped Gains

This is the critical risk many put sellers overlook: opportunity cost.

Example scenario:

- You sell a $50 put for $2 premium (30 days)

- The stock rallies to $65 during those 30 days

- You made $2 (4% return)

- If you’d bought shares, you’d have made $15 (30% return)

When you sell a put, your maximum profit is capped at the premium collected, regardless of how high the stock rises. You miss out on explosive upside moves.

This is the trade-off: consistent, smaller income (put premium) versus unlimited appreciation potential (stock ownership).

Real Returns: Crunching the Numbers

Let’s compare realistic return scenarios across different market conditions.

Scenario 1: Stock Rises Moderately (+10% over 3 months)

Stock starts at $50, ends at $55 after 90 days

Buying Stock:

- Buy 100 shares at $50 = $5,000 cost

- Sell at $55 = $5,500

- Profit: $500 (10% return)

Selling Puts (three 30-day cycles):

- Month 1: Sell $50 put for $150 → expires worthless, keep $150

- Month 2: Sell $52 put for $150 → expires worthless, keep $150

- Month 3: Sell $54 put for $160 → expires worthless, keep $160

- Total profit: $460 (9.2% return)

Winner: Roughly tied—stock ownership slightly edges out due to price appreciation

Scenario 2: Stock Stays Flat ($50 → $50 over 3 months)

Buying Stock:

- Buy 100 shares at $50 = $5,000 cost

- Sell at $50 = $5,000

- Profit: $0 (0% return)

Selling Puts (three 30-day cycles):

- Month 1: Sell $50 put for $150 → expires worthless, keep $150

- Month 2: Sell $50 put for $150 → expires worthless, keep $150

- Month 3: Sell $50 put for $150 → expires worthless, keep $150

- Total profit: $450 (9% return)

Winner: Selling puts—significantly outperforms in flat markets

Scenario 3: Stock Rises Dramatically (+40% over 3 months)

Stock starts at $50, ends at $70 after 90 days

Buying Stock:

- Buy 100 shares at $50 = $5,000 cost

- Sell at $70 = $7,000

- Profit: $2,000 (40% return)

Selling Puts:

- Month 1: Sell $50 put for $150 → expires worthless, keep $150

- Months 2-3: Stock runs away, you collect premiums but miss the rally

- Total profit: ~$450 (9% return)

Winner: Buying stock—massively outperforms in strong bull moves

Scenario 4: Stock Falls Moderately (-15% over 3 months)

Stock starts at $50, falls to $42.50 after 90 days

Buying Stock:

- Buy 100 shares at $50 = $5,000 cost

- Current value at $42.50 = $4,250

- Loss: -$750 (-15% return)

Selling Puts:

- Month 1: Sell $50 put for $150 → stock drops, you’re assigned at $50

- Effective cost basis: $48.50 ($50 strike – $1.50 premium)

- Current value at $42.50 = $4,250

- Loss: -$600 (-12% return)

Winner: Selling puts—premium cushions the downside slightly

Time Commitment & Management Requirements

This is where the practical differences become obvious.

Buying Stocks: Minimal Active Management

- Initial decision: Research and buy

- Ongoing: Hold and occasionally check price

- Time commitment: 1-2 hours initially, then 15 minutes monthly

- Decisions required: Only when to sell

- Stress level: Low to moderate depending on volatility

You can literally buy and forget for years if following a long-term strategy.

Selling Puts: Active Management Required

- Initial decision: Research, select strike and expiration

- Ongoing: Monitor until expiration every 30-45 days

- Time commitment: 2-3 hours initially, then 30-60 minutes per position every month

- Decisions required: Strike selection, expiration choice, whether to close early, what to do if assigned, rolling decisions

- Stress level: Moderate to high, especially near expiration

You’re making decisions every 30-45 days minimum. Miss an expiration or forget to roll, and you might be assigned when you didn’t intend to be.

After managing 15+ put positions manually in spreadsheets, I realized the tracking complexity was eating up hours every week. That’s when I built QuantWheel’s Wheel Native Journal to automatically track puts through assignment, adjust cost basis, and alert me when positions needed attention. The manual management was simply unsustainable at scale.

Tax Implications: Short-Term vs. Long-Term

Taxes matter, especially for active strategies.

Stock Ownership Tax Treatment

- Hold > 1 year: Long-term capital gains (0%, 15%, or 20% depending on income)

- Hold < 1 year: Short-term capital gains (taxed as ordinary income, up to 37%)

Buy-and-hold naturally favors long-term holding, qualifying for preferential long-term capital gains rates.

Put Selling Tax Treatment

- Premium collected: Short-term capital gain when position closes

- If assigned: Premium reduces your cost basis, capital gains clock starts when you buy shares

Put premiums are always taxed as short-term gains because options rarely last beyond one year. If you’re selling monthly puts, you’re generating short-term gains each cycle.

Example:

- Sell $50 put for $200, expires worthless: $200 short-term gain (taxed at ordinary income rates)

- Sell $50 put for $200, get assigned: Your cost basis becomes $48 per share, and if you sell the shares later, capital gains treatment depends on how long you held the shares

For high-income earners, the short-term tax treatment meaningfully reduces put selling returns compared to long-term stock appreciation.

When Selling Puts Makes More Sense

Selling puts outperforms or matches buying stocks in these situations:

1. Flat or Slowly Rising Markets

When stocks grind sideways or rise modestly, premium collection outperforms price appreciation. You generate 1-3% monthly regardless of price movement.

2. High Implied Volatility Environments

When options are expensive (high IV), premiums are juicier. You collect more income for the same obligation, improving returns.

3. You Want Lower Entry Prices

If you think a $50 stock is worth buying but would prefer $47, selling a $47 put lets you get paid to wait for your target price.

4. You Have Time and Interest in Active Management

If you enjoy trading, monitoring positions, and making monthly decisions, selling puts provides more engagement than passive ownership.

5. You’re Building Positions Systematically

Some investors use put selling to build stock positions over time, collecting premium while waiting for dips to enter.

When Buying Stocks Makes More Sense

Stock ownership outperforms or is more practical in these situations:

1. Strong Bull Markets

When stocks are rallying hard, capped put premiums underperform unlimited stock appreciation. You want to be along for the ride.

2. Long-Term Hold Strategy

If your plan is to buy and hold for 5-10+ years, the simplicity and tax benefits of stock ownership beat active put management.

3. Limited Time for Management

Busy professionals who check portfolios quarterly, not weekly, are better suited to stock ownership than active put management.

4. Dividend Growth Focus

If you’re investing for growing dividend income, owning shares directly is simpler than repeatedly selling puts and managing assignments.

5. You Want Maximum Simplicity

Buying stock and holding is the simplest strategy. No expiration dates, no Greeks, no assignment surprises. Just own shares.

Can You Do Both? The Hybrid Approach

Many investors don’t choose one or the other—they use both strategically.

Core-and-Explore Strategy

- Core holdings (60-70% of portfolio): Long-term stock positions in quality companies, held for years

- Active positions (30-40% of portfolio): Sell puts on stocks you want to add to, generating income while building positions

This balances the simplicity and upside of stock ownership with the income generation of put selling.

The Wheel Strategy

Another hybrid is the wheel strategy, which combines put selling and stock ownership:

- Sell cash-secured puts to collect premium

- If assigned, own the shares

- Sell covered calls against the shares to collect more premium

- If called away, restart at step 1

This systematic approach treats assignment as part of the plan, not a failure. You’re either collecting put premium (when you don’t own shares) or call premium (when you do own shares).

The Bottom Line: What’s Actually Better?

There’s no universal answer—it depends on your goals, time, and market outlook.

Choose buying stocks if:

- You want maximum upside participation

- You prefer passive management

- You’re investing for 5+ years

- You value simplicity over optimization

- You want favorable long-term capital gains tax treatment

Choose selling puts if:

- You want to generate monthly income

- You’re willing to actively manage positions

- You want to acquire stocks at lower effective prices

- You’re comfortable with capped gains

- You have time to monitor and make decisions

For most investors: A hybrid approach makes sense. Own core positions for long-term appreciation, and sell puts on stocks you want to add at lower prices, generating income while waiting for opportunities.

The key is honest self-assessment: Will you actually manage put positions every 30 days, or will they become a source of stress and forgotten assignments? If the latter, stick with stock ownership. If you enjoy active management and want to optimize every dollar, put selling is a powerful tool.

Start your free trial of QuantWheel – automatically track cash-secured puts, cost basis adjustments after assignment, and compare your returns to buy-and-hold benchmarks.

Start your free trial of QuantWheel →

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. Always do your own research and consider consulting with a financial advisor before making investment decisions.