TL;DR: How to Roll Options Up

Rolling options up means closing your current position and opening a new one at a higher strike price, typically done when your position is in the money and you want to collect more premium while giving the stock room to continue rising.

Simple Example

You sold a covered call on AAPL at the $180 strike for $2.00. The stock rallies to $185, and your call is now worth $5.50 (it costs $5.50 to buy it back). Instead of taking assignment, you buy back the $180 call for $5.50 and simultaneously sell the $190 call for $7.00.

Your net result: You paid $5.50 and received $7.00 = $1.50 net credit collected.

You now have 10 more points of upside ($190 strike instead of $180), and you collected an additional $150 per contract.

If AAPL continues to rise to $190, you’ll make an extra $500 in stock appreciation (from $185 to $190) plus the $150 in additional premium.

When to Roll Up

- Your covered call is in the money with 21+ days remaining

- You can roll for a net credit (collect more than you pay)

- You believe the stock has further upside potential

- Technical levels suggest more room to run

- You want to stay in the position rather than take assignment

When NOT to Roll Up

- Less than 7-10 days until expiration (time decay favors keeping current position)

- Rolling would result in a net debit (you’d pay money to roll)

- The stock shows signs of topping or reversal

- You’re satisfied with current gains and want assignment

- The new strike offers insufficient premium for the risk

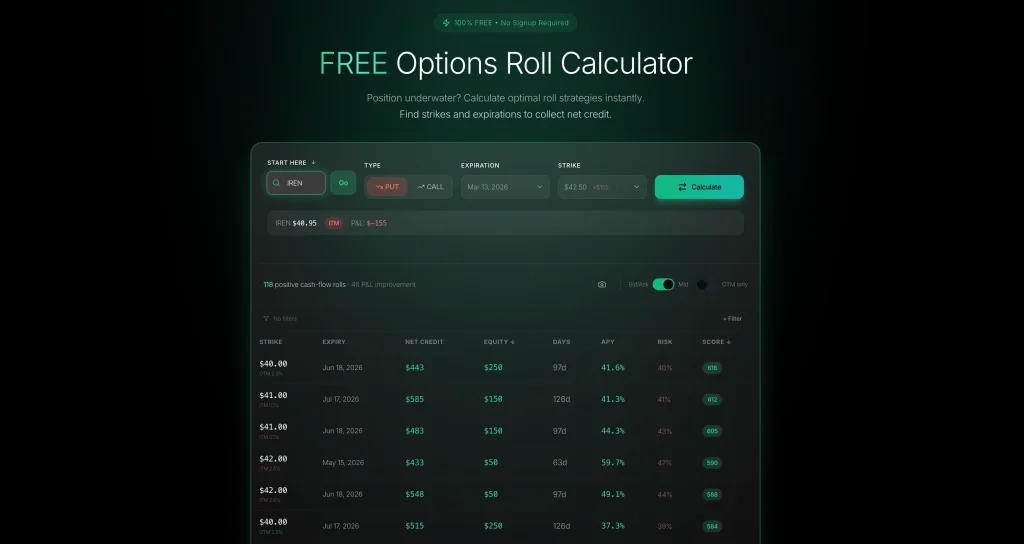

Here’s where you can get free options roll calculations that can help you decide on what is the best roll for your case.

Understanding the Mechanics of Rolling Up

Rolling up is not a single transaction—it’s two simultaneous trades executed as one order:

- Buy-to-close your current option position

- Sell-to-open a new option at a higher strike price

When you execute this as a single “roll” order with your broker, both legs happen simultaneously at the net credit or debit price you specify. This is crucial because executing them separately exposes you to price movement risk between trades.

What “Rolling Up” Actually Means

In the wheel strategy context, rolling up typically applies to covered calls when the underlying stock has appreciated. You’re moving your strike price higher to:

- Collect additional premium

- Allow more stock appreciation before assignment

- Extend time if needed (rolling up and out)

- Adjust your position to current market conditions

The key principle: Always roll for a net credit. If you can’t collect more premium than you pay to close the current position, rolling up doesn’t make financial sense.

When to Roll Options Up: The Decision Framework

The best type of roll – credit roll. Example below.

Not every in-the-money covered call should be rolled up. Here’s the systematic framework successful wheel traders use:

1. Time Remaining Check

Roll up when you have 21+ days until expiration. With significant time remaining, your current option still has substantial extrinsic value, making it expensive to buy back. However, higher strike options also have good premium, often allowing you to roll for a credit.

Avoid rolling with less than 7-10 days remaining. At this point, time decay (theta) is working heavily in your favor. Your current option is rapidly losing value, and you’re better off letting it expire or roll out (same strike, later date) rather than rolling up.

2. Net Credit Requirement

Always calculate the net credit before rolling.

Use this formula:

Net Credit = (Premium from New Strike) - (Cost to Close Current Strike)Example:

- Current position: Short $180 call, costs $5.50 to buy back

- New position: Sell $190 call for $7.00

- Net Credit = $7.00 – $5.50 = $1.50 credit ✓

If this calculation results in a debit (you pay more than you receive), don’t roll up. Consider rolling out instead or just holding your current position.

3. Stock Momentum Analysis

Ask: Does the stock have room to run to the new strike?

Look for:

- Technical resistance levels above current price

- Positive momentum indicators

- No immediate earnings or catalysts

- Uptrend continuation patterns

- Sector strength supporting further gains

If the stock looks like it’s topping out, taking assignment at your current strike might be the smarter play. Rolling up only to have the stock reverse means you collected premium but gave up assignment that would have been profitable.

4. Premium Yield Calculation

Evaluate if the additional premium is worth it:

Additional Yield = Net Credit / Current Stock PriceExample: If you collect a $1.50 net credit on a $185 stock:

- Additional Yield = $1.50 / $185 = 0.81%

For extending time by 30 days and giving up 10 points of assignment opportunity, is 0.81% adequate compensation? Some traders require at least 1-2% to make rolling up worthwhile.

Step-by-Step: How to Roll a Covered Call Up

Let’s walk through the complete process with a real example.

Starting Position

- Stock: NVDA trading at $485

- Current position: Short 1x $460 covered call

- Expiration: 23 days remaining

- Current option value: $28.50 (costs $28.50 to buy back)

- Original credit: $15.00

Analysis Phase

Step 1: Check technical levels. NVDA has support at $480 and next resistance at $500. The trend is bullish with no immediate reversal signals.

Step 2: Evaluate roll options. You compare several possibilities:

| New Strike | Expiration | Premium | Net Credit | Extra Upside |

|---|---|---|---|---|

| $480 (same exp) | 23 days | $20.00 | -$8.50 debit | $20 |

| $500 (same exp) | 23 days | $12.00 | -$16.50 debit | $40 |

| $480 (+30 days) | 53 days | $35.00 | +$6.50 credit | $20 |

| $500 (+30 days) | 53 days | $28.00 | -$0.50 debit | $40 |

Step 3: Select the optimal roll. The $480 strike, 30 days out provides:

- $6.50 net credit collected

- 20 more points of upside potential ($460→$480)

- 30 additional days of time

- 1.34% additional yield ($6.50/$485)

This roll makes sense. You collect meaningful premium, extend time, and give the stock room to run to $500 where the next resistance level sits.

Execution Phase

Step 4: Place the roll order:

- Buy-to-close: 1x NVDA $460 call at $28.50

- Sell-to-open: 1x NVDA $480 call (53 DTE) at $35.00

- Order type: Net credit order for $6.50 or better

- Execution: Filled at $6.60 net credit

Step 5: Verify the new position:

- New strike: $480

- New expiration: 53 days out

- New breakeven: $485 (current price)

- Total premium collected: $15.00 (original) + $6.60 (roll) = $21.60 total

- Maximum gain if assigned at $480: ($480 – $450 cost basis) + $21.60 = $51.60 per share

Post-Roll Management

Here’s where most traders struggle: tracking your adjusted cost basis and total premium through multiple rolls. Your broker shows your stock cost basis as $450, but your real economic cost after collecting $21.60 in total premium is actually $428.40.

This is exactly where manual tracking breaks down. After 3-4 rolls and potentially an assignment, calculating your true cost basis becomes a spreadsheet nightmare. QuantWheel’s journal automatically tracks every roll, adjusts your cost basis as you collect premium, and shows your real breakeven and profit at all times.

Rolling Puts Up (Less Common but Important)

While rolling covered calls up is common, rolling cash-secured puts up is less frequent but happens in specific scenarios.

When to Roll Puts Up

You’d roll a put up when:

- The stock has fallen significantly below your strike

- You don’t want assignment at your current strike

- A higher strike offers better premium

- You want to increase your cost basis for eventual assignment

Example:

- Stock: PLTR trading at $45

- Current position: Short $60 put (opened when stock was $65)

- Stock has fallen to $45, put is worth $15.50

- Roll up to: $50 put for $7.00

- Net result: Pay $15.50, receive $7.00 = $8.50 net debit

Wait—didn’t we say never roll for a debit? In this case, you’re paying $8.50 to reduce your assignment risk by $10 per share ($60 down to $50). If you don’t want to own PLTR at $60, paying $8.50 to lower your strike to $50 might be worth it, especially if you can extend time significantly.

However: Most wheel traders prefer to take assignment at the lower price ($45) rather than roll the $60 put up. The wheel strategy philosophy is “assignment is fine” so fighting it by rolling up (at a debit) works against the strategy.

Rolling Up vs Rolling Out vs Rolling Up and Out

Understanding these distinctions helps you choose the right adjustment:

Rolling Up

- What: Higher strike, same expiration

- When: Stock moved up, time remaining is sufficient

- Goal: Collect premium, allow more stock appreciation

- Typical result: Small credit or slight debit, more upside room

Rolling Out

- What: Same strike, later expiration

- When: Need more time, defend current strike

- Goal: Collect premium from additional time value

- Typical result: Credit received, maintains same upside limit

Rolling Up and Out (Most Common)

- What: Higher strike AND later expiration

- When: Stock moved up, want to optimize both strike and time

- Goal: Maximize credit by combining both adjustments

- Typical result: Better credit than rolling up alone, more upside + more time

Pro tip: Rolling up and out usually provides the best credit because you’re benefiting from both additional time value and volatility at the higher strike. This is why experienced traders rarely roll up without also rolling out to a later expiration.

Common Mistakes When Rolling Options Up

Mistake #1: Rolling for a Debit Without Good Reason

New traders often roll up at a debit thinking “I’ll make it back with stock appreciation.” This violates the fundamental principle of the wheel strategy: collect premium consistently. If you can’t roll for a credit, you’re speculating on stock direction rather than executing a systematic strategy.

Exception: Rolling a deep ITM put up at a small debit to avoid assignment at an unfavorable price can make sense, but recognize you’re deviating from the core strategy.

Mistake #2: Rolling Too Close to Expiration

With 3-5 days until expiration, time decay is accelerating rapidly. Your current option is losing value quickly—this is exactly what you want as an option seller. Rolling up at this point usually means buying back an option that’s about to expire worthless anyway.

Better approach: If you’re within 7 days of expiration and in the money, either let assignment happen or roll out (same strike, later expiration) rather than rolling up.

Mistake #3: Ignoring Technical Resistance

You roll your $100 call up to $110 to give the stock more room. But there’s major technical resistance at $105 that you didn’t notice. The stock stalls at $106, reverses, and now your $110 call that you paid up for expires worthless—but you could have been assigned at $100 and moved on to the next position.

Better approach: Always check resistance levels when selecting your new strike. Roll to a strike just below major resistance, not significantly above it.

Mistake #4: Chasing the Stock Up Repeatedly

The stock keeps rallying, so you keep rolling up: $50→$55→$60→$65. Each roll collects a small credit, but you’ve now rolled 3 times and extended expiration by 90 days. You’ve collected $4 in net credits across all rolls but gave up $15 in stock appreciation.

Better approach: After 1-2 rolls, consider letting assignment happen. Take your profits, move to a new opportunity, and start a fresh wheel cycle. Chasing doesn’t always optimize returns.

Mistake #5: Not Tracking Total Return Accurately

You’ve rolled 3 times, collected premium on each roll, and finally got assigned. But when you calculate your return, you forget to include all the roll credits in your cost basis. Your broker shows your cost basis wrong because they don’t track the full wheel cycle.

Choosing the Right Strike When Rolling Up

Strike selection determines your trade-off between upside potential and premium collection. Here’s the systematic approach:

The Three Strike Options

When rolling up, you typically have three choices:

1. Conservative Roll (1-2 strikes up)

- Moderate additional premium

- Stock only needs small move to reach new strike

- Lower risk of missing assignment

- Better for neutral-to-slightly-bullish outlook

2. Aggressive Roll (3-5 strikes up)

- Larger credit collected

- Gives stock significant room to run

- Higher risk of the stock not reaching new strike

- Better for strongly bullish outlook

3. At-the-Money Roll (current stock price)

- Balanced premium and probability

- 50/50 chance of assignment

- Most liquid strikes (tighter spreads)

- Good default choice when uncertain

The Delta Method

Professional traders often use delta to select strikes:

- 0.30 delta: Conservative (30% probability of finishing ITM)

- 0.50 delta: Balanced (at-the-money)

- 0.70 delta: Aggressive (70% probability of finishing ITM)

When rolling up, target the delta that matches your bullishness on the stock. More bullish = lower delta (higher strike), allowing more appreciation before assignment.

The Premium Yield Method

Some traders select strikes based on minimum premium yield:

Target: At least 1-2% of stock price in net credit for a 30-day roll

Example: Stock at $150:

- Minimum acceptable credit = $150 × 1.5% = $2.25

- Evaluate strikes until you find one delivering at least $2.25 net credit

- This becomes your new strike

This method ensures you’re adequately compensated for giving up potential assignment and extending time.

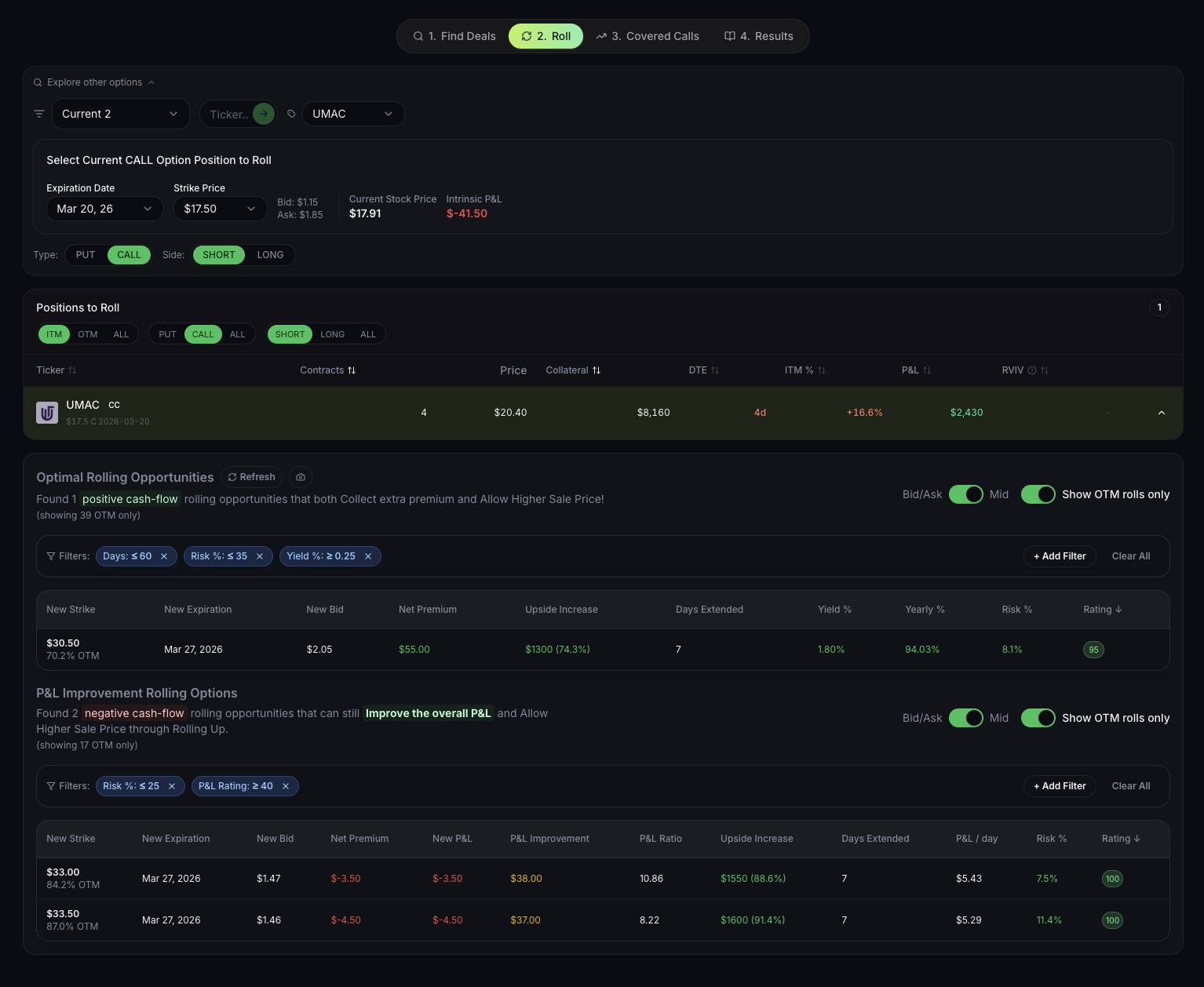

Automating Roll Analysis with QuantWheel

Here’s the reality of rolling options: calculating every possible combination manually is tedious. For a single position, you might have:

- 5-7 reasonable strike options

- 3-4 expiration dates to consider

- 20+ possible roll combinations

Manually calculating the net credit, yield, upside potential, and break-even for each option takes 15-30 minutes per position. When you’re managing 10-15 wheel positions, this becomes unsustainable.

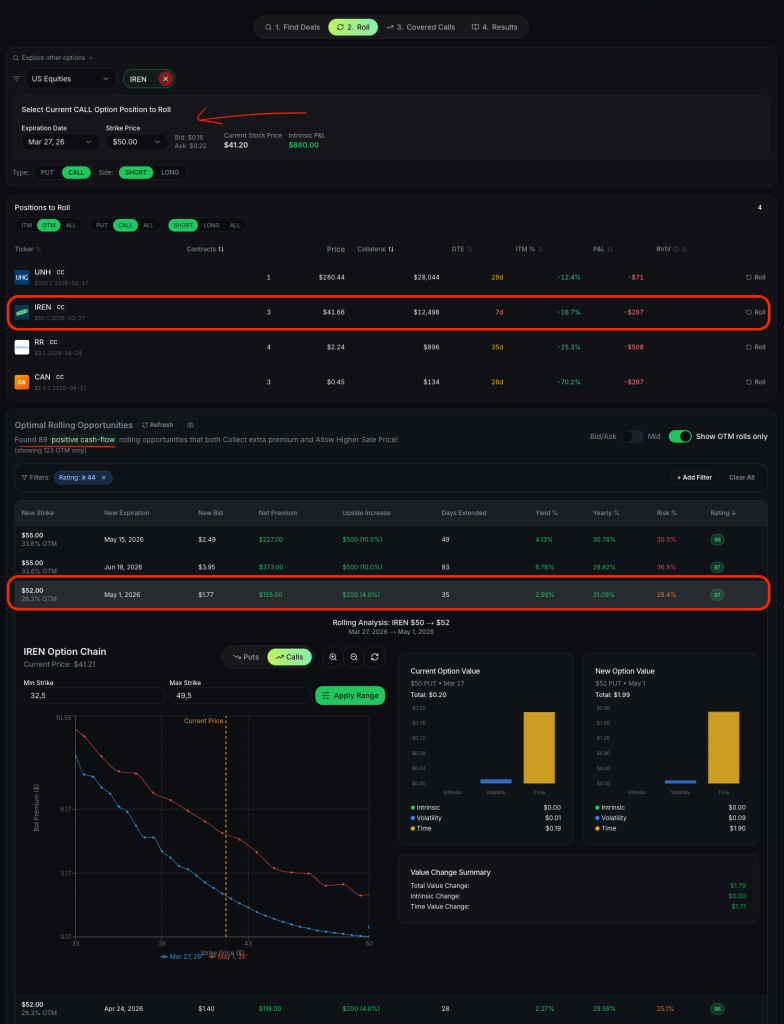

QuantWheel’s Roll Assistant solves this by:

- Analyzing all possible rolls automatically – Every strike and expiration combination

- Calculating net credit for each option – Instantly showing which rolls pay you

- Ranking by optimization goal – Max credit, max upside, or balanced approach

- Showing before/after comparison – Visual display of how the roll changes your position

- Tracking roll history – Every roll recorded with adjusted cost basis

When you’re in a position that’s a candidate for rolling, QuantWheel immediately shows you the optimal roll based on your criteria. No manual calculation, no spreadsheet updates, no missing the best opportunity because you didn’t check.

Instead of spending 45 minutes calculating 12 different roll options, you see the answer in 5 seconds and execute with confidence.

Advanced Rolling Strategies

Once you master the basics, these advanced techniques optimize roll profitability:

The Legging Strategy

Instead of rolling as one simultaneous transaction, you execute the legs separately when conditions are favorable:

- Buy back your current option when volatility spikes (option inflated)

- Wait for pullback or consolidation

- Sell the new higher strike when volatility drops (better premium)

Risk: The stock could move against you between legs. Only use this when you’re comfortable with naked call risk temporarily.

The Partial Roll

Roll only half your contracts up, leaving the other half at the original strike:

Example:

- Position: Short 4x $100 calls

- Stock at $110, considering roll to $115

- Action: Buy back 2x $100 calls, sell 2x $115 calls

- Result: If stock goes to $120, 2 contracts assign at $100 (earlier), 2 at $115 (better)

This hedges your strike selection—you capture upside from both strikes depending on where the stock finishes.

The Calendar Roll Up

Roll to a much later expiration (60-90 days) at a significantly higher strike:

Example:

- Current: Short $50 call, 15 days left, stock at $55

- Roll to: $60 call, 90 days out

- Benefit: Collect large credit from extended time, give stock long runway to $60

This works well in strong bull markets when you’re highly confident in continued appreciation but want to collect significant premium for waiting.

The Earnings Roll

If earnings approaches before your expiration, consider rolling up and past earnings:

Example:

- Current: Short $100 call, 10 days to expiration

- Earnings: In 8 days

- Roll to: $105 call, expiring after earnings (35 days out)

- Benefit: Collect elevated IV premium before earnings, position past the uncertainty

Post-earnings, IV typically drops, which benefits your new position. You’ve also given the stock room to run on positive earnings.

Tax Implications of Rolling Options

Rolling has specific tax consequences that affect your net returns:

Realized vs Unrealized Gains

When you roll:

- Closing your original position realizes a gain or loss

- Opening the new position starts a new tax position

- These are two separate tax events, not one continuous position

Example:

- Sold original $50 call for $2.00

- Bought it back for $5.00

- Realized loss: -$3.00 (taxable event)

- Sold new $55 call for $6.50

- New position: +$6.50 credit (unrealized until closed)

Many traders mistakenly view the roll as one event with a net $1.50 credit, but the IRS sees it as a $3.00 loss and a $6.50 gain (when eventually closed).

Wash Sale Considerations

If you:

- Close a losing call option

- Sell a substantially identical call within 30 days

- The wash sale rule may apply

However, options on the same underlying at different strikes are generally NOT considered substantially identical, so rolling to a different strike usually avoids wash sale issues.

Consult a tax professional for your specific situation, as options tax treatment can be complex.

When to Stop Rolling and Accept Assignment

Not every position should be rolled indefinitely. Know when to let assignment happen:

Assignment Is Better When:

- You’ve rolled 2-3 times already – Diminishing returns set in, time to move on

- The stock has hit major resistance – Unlikely to push higher in timeframe

- Earnings or catalyst approaching – Uncertainty makes rolling risky

- Premium yield is below 1% – Not worth the effort and risk

- You want to redeploy capital – Better opportunities exist elsewhere

- The wheel cycle is 120+ days old – Time to close and start fresh

- You’re no longer bullish – Don’t fight your analysis by rolling up

The Cost of Over-Rolling

Rolling up repeatedly to avoid assignment has hidden costs:

- Opportunity cost: Capital tied up in one position vs starting new cycles

- Commission costs: Each roll incurs commissions and spreads

- Time cost: Managing complex rolled positions vs simple new positions

- Mental cost: Tracking multiple rolls, adjusted strikes, varying expirations

- Assignment risk: Eventually most positions get assigned anyway

Sometimes the best decision is accepting a profitable assignment, closing the cycle, and starting fresh on a new stock with better risk/reward.

Real Example: Complete Roll Up Decision Process

Let’s walk through a real-world scenario with full analysis:

Initial Position

- Stock: AMD trading at $142

- Position: Short 2x $130 covered calls, 28 days to expiration

- Original credit: $4.50 per contract ($900 total for 2 contracts)

- Current value: $14.00 to buy back ($2,800 total)

- Stock cost basis: $125 per share (200 shares)

Analysis

Current situation: The calls are $12 in-the-money. If assigned today:

- Sell stock at $130 = $5 gain per share

- Keep $4.50 premium collected

- Total profit: $9.50 per share = $1,900 profit

This is good! But AMD is showing strength, and you believe it can reach $150.

Roll options to consider:

| Strike | Expiration | Buy Back Cost | Sell New Option | Net Credit | Extra Upside | Days Added |

|---|---|---|---|---|---|---|

| $135 | +0 days (same) | $2,800 | $2,200 | -$600 debit | $5 | 0 |

| $140 | +0 days (same) | $2,800 | $1,000 | -$1,800 debit | $10 | 0 |

| $135 | +30 days | $2,800 | $3,400 | +$600 credit | $5 | 30 |

| $140 | +30 days | $2,800 | $2,600 | -$200 debit | $10 | 30 |

| $145 | +30 days | $2,800 | $2,000 | -$800 debit | $15 | 30 |

| $150 | +30 days | $2,800 | $1,500 | -$1,300 debit | $20 | 30 |

Analysis:

- Rolling to $135 (+30 days) for $600 credit is possible

- Gives 5 more points of upside

- Collects an additional 0.42% yield ($600/$142,000)

Decision: Roll to $135 strike, 30 days out:

- Nets $600 additional credit

- If AMD reaches $150, you cap out at $135 but have collected $5.50 total premium

- Total potential profit: ($135 – $125) + $5.50 = $15.50 per share = $3,100 total

- vs taking assignment now for $1,900

By rolling, you’ve positioned yourself to make an additional $1,200 IF AMD reaches $150. If AMD stays flat or drops, you still collected an extra $600 and worst case get assigned at $135 instead of $130 (better outcome).

Execution: Place the roll order as a net credit limit order for $3.00 per contract ($600 total for 2 contracts). Filled at $3.10 ($620 total).

Six Weeks Later

AMD reached $149 and your $135 calls are now assigned. Final results:

- Stock appreciation: ($135 – $125) = $10 per share

- Total premium collected: $4.50 + $3.10 = $7.60 per share

- Total profit: $17.60 per share × 200 shares = $3,520 profit

vs the original assignment at $130 which would have yielded $1,900. The roll up netted an additional $1,620 profit for making one smart adjustment.

Start your free trial of QuantWheel to analyze roll opportunities like this instantly across all your positions.

Start your free trial of QuantWheel →

Conclusion: Mastering the Roll Up

Rolling options up is a tactical skill that separates profitable wheel traders from mediocre ones. The key principles to remember:

- Always roll for a net credit – You should collect more premium than you pay

- Give yourself time – Rolling with 21+ days remaining provides better opportunities

- Select strikes intelligently – Use technical levels, delta, or yield targets to choose

- Don’t chase indefinitely – After 2-3 rolls, consider accepting assignment

- Track everything accurately – Know your true cost basis through all adjustments

The difference between making 12% annual returns and 25% annual returns on the wheel strategy often comes down to rolling decisions. Those extra 2-3 rolls per year, done correctly, compound into significantly better performance.

But here’s the challenge: analyzing 15-20 possible rolls per position, across 10 active positions, while maintaining accurate cost basis tracking through dozens of adjustments—this is where most traders struggle. You either spend hours doing analysis and tracking, or you make suboptimal decisions because you didn’t evaluate all options.

QuantWheel eliminates this bottleneck. Every position showing roll opportunities gets instant analysis showing the optimal roll based on your goals. Every roll you execute automatically updates your cost basis. Every wheel cycle from opening put through assignment to final covered call assignment is tracked seamlessly.

Stop spending your evenings calculating roll options in spreadsheets. Start making better roll decisions in seconds.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. Always do your own research and consider consulting with a financial advisor before making investment decisions. Rolling options can result in losses if the underlying stock moves against your position, and there is no guarantee that any strategy will be profitable.