Knowing how to sell a cash secured put is one thing. Knowing when to sell for maximum profit while managing risk is what separates consistent premium collectors from those who struggle. The difference between entering at the right moment versus the wrong one can mean the difference between collecting premium safely and getting assigned on a declining stock.

Author: David Romic.

QuantWheel is the platform that powers the tracking examples which you will see in the screenshots from this article, including my personal track record example at the time of writing this article.

TLDR: When to Sell Cash Secured Puts

Best conditions for selling cash secured puts: Enter when IV Rank exceeds 50% (higher premiums), the stock shows technical support near your strike price, and you’re genuinely willing to own shares at that level.

Target 30-45 days to expiration for the optimal balance of premium and time decay.

Example trade scenario: AMD is trading at $150 with IV Rank of 65% (elevated).

You’d happily own AMD at $140 or below.

Sell the $140 strike put with 35 days to expiration, collecting $4.20 premium ($420 per contract).

Your breakeven is $135.80 ($140 strike – $4.20 premium).

If AMD stays above $140 at expiration, you keep the $420 premium (3% return in 5 weeks). If assigned, your actual cost is $135.80 per share—9.5% below the current price.

The key timing factors: high implied volatility (better premiums), willing buyer at the strike price (you), adequate time premium (30-45 DTE), and technical support (reduces assignment risk).

Understanding Market Timing for Cash Secured Puts

Unlike directional traders who need to be right about price movement, put sellers profit from three scenarios: the stock goes up, stays flat, or declines less than the premium collected.

The wheel strategy begins with selling cash secured puts, making entry timing crucial for the entire cycle. Poor timing leads to unfavorable assignments on declining stocks. Smart timing means collecting solid premium on stocks you actually want to own at prices below current market value.

Why Timing Matters More Than Most Realize

A cash secured put sold during low volatility might collect $1.50 per share. The same strike on the same stock during elevated volatility could collect $4.00.

That’s 167% more premium for identical risk. Multiply this across dozens of trades annually, and timing becomes the difference between mediocre and exceptional results.

Timing also affects assignment probability.

Selling puts when a stock tests support levels differs dramatically from selling during momentum breakdowns.

Both collect premium, but assignment rates and outcomes diverge significantly.

Optimal Market Conditions for Selling Cash Secured Puts

High Implied Volatility (IV Rank Above 50%)

Implied volatility represents the market’s expectation of future price movement. Higher IV means larger expected moves, which translates directly to higher option premiums.

For cash secured put sellers, high IV is your friend—you collect more premium for the same strike and expiration.

An IV Rank of 60% means current volatility is higher than 60% of readings over the past year.

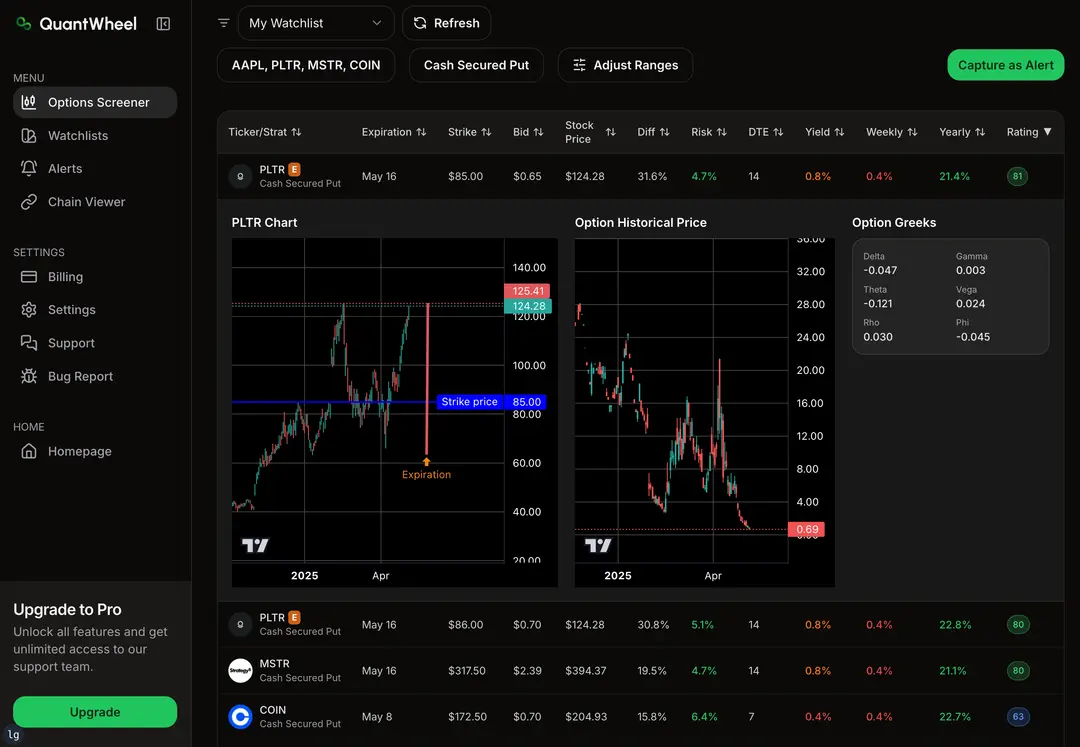

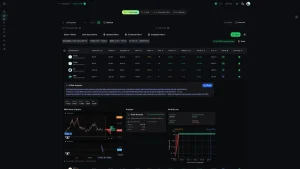

Example of a good Cash – Secured Put trade in optimal market conditions (IV Rank above 50%):

![]()

Targeting IV Rank thresholds:

- Above 50%: Good premium relative to recent volatility

- Above 60%: Excellent premium, favorable for sellers

- Above 70%: Exceptional premium, though often indicates uncertainty

When market-wide volatility spikes (VIX above 20), premiums expand across most stocks. These periods, though psychologically uncomfortable, present some of the best opportunities for cash secured put sellers who’ve done their fundamental homework.

Stocks in Uptrends or Consolidation

Technical analysis provides context for your strike selection.

Selling puts on stocks in established uptrends with clear support levels reduces assignment risk while maintaining attractive premiums.

Trade example for a Cash – Secured put on a stock in uptrend:

Trade example for a Cash – Secured put on a stock in consolidation:

Favorable technical patterns:

- Stocks consolidating after rallies (building support)

- Gentle uptrends with periodic healthy pullbacks

- Stocks testing support levels with historical buyer interest

- Price trading in upper half of recent range

Avoid selling puts on stocks in clear downtrends unless assignment is your goal.

“Catching a falling knife” often results in assignment at inflated prices relative to where the stock eventually finds support.

Learn about assignment here: What happens when you get assigned?

After Minor Pullbacks (2-5%)

Minor pullbacks in otherwise healthy stocks create temporary premium expansion due to short-term fear. These setups offer improved entry points—you’re selling puts at lower strike prices with elevated premiums.

A stock at $100 might pullback to $95 due to sector weakness or broad market volatility. If fundamentals remain strong and the pullback appears temporary, this presents an opportunity to sell the $90 or $92 strike put with better premium than existed at $100.

The key distinction: pullbacks versus breakdowns. Pullbacks retrace 3-8% before resuming trends. Breakdowns violate support, shift to downtrends, and continue falling. Wait for price stabilization signals before selling puts after significant declines.

Before Known Catalysts (Carefully)

Earnings announcements, FDA approvals, and product launches increase IV as uncertainty rises. This elevated IV inflates premiums, creating seemingly attractive opportunities. However, these situations require extreme caution.

Selling puts before earnings captures inflated premium but accepts unknown binary outcomes. A negative surprise can result in assignment at prices far above post-earnings value. Only sell pre-catalyst puts if you’re completely comfortable with worst-case assignment scenarios.

Pre-catalyst considerations:

- Would you buy shares at this strike after bad news?

- Can you handle a 20-30% post-catalyst decline?

- Does the elevated premium adequately compensate for uncertainty?

- Are you prepared for significant overnight gap risk?

Conservative traders close or roll positions before major catalysts. Aggressive traders leverage the premium expansion, understanding the tradeoffs.

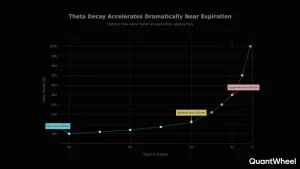

Optimal Time Frames: Days to Expiration Strategy

The 30-45 Day Sweet Spot

Research and practitioner experience converge on 30-45 days to expiration (DTE) as optimal for cash secured put selling. This timeframe balances several competing factors:

- Theta decay accelerates in final 30-45 days

- Enough time value to generate meaningful premium

- Monthly options cycle alignment (liquidity)

- Sufficient duration to manage positions if needed

- Avoids rapid gamma risk of weekly options

Time decay (theta) is non-linear. Options don’t lose value evenly over time—decay accelerates as expiration approaches.

The 30-45 day window captures the beginning of this acceleration while maintaining enough extrinsic value to collect worthwhile premium.

Selling 30-45 DTE puts also aligns with monthly option cycles, ensuring maximum liquidity and tighter bid-ask spreads. This liquidity matters when closing positions early or rolling to avoid assignment.

Weekly Options (7 DTE or Less)

Weekly options offer rapid theta decay and quick turnarounds. A 7-day put decays faster than a 45-day put, allowing you to collect similar percentage returns in less time. However, this speed comes with tradeoffs.

Weekly option characteristics:

- Faster premium collection (7 days vs 45 days)

- More transactions and monitoring required

- Higher gamma risk (rapid delta changes)

- Less time to manage adverse moves

- Better for smaller accounts wanting higher turnover

Weekly strategies work well in stable, range-bound markets. During volatile periods, the compressed timeframe provides little room to manage positions before assignment. Consider weeklies after establishing comfort with 30-45 DTE strategies.

60-90 DTE for Portfolio Stability

Longer-dated puts (60-90 DTE) collect larger absolute premium amounts but lower annualized returns. These timeframes work well when you want to reduce transaction frequency or during lower volatility environments where 30-45 DTE premiums look thin.

Longer-dated benefits:

- Larger premium per trade

- Fewer transactions (lower commissions)

- More time to manage positions

- Less monitoring required

- Smoother equity curve

The annualized return calculation reveals the tradeoff. A 30 DTE put collecting 2% returns 24% annualized (2% × 12 months). A 90 DTE put collecting 5% returns 20% annualized (5% × 4 quarters). The longer-dated option collects more per trade but less per year.

Strike Selection Timing Considerations

The Delta Approach (30 Delta vs 16 Delta)

Delta measures how much an option’s price changes for each $1 move in the underlying stock. For put sellers, delta also approximates assignment probability. A 30 delta put has roughly a 30% chance of finishing in-the-money at expiration.

Common delta targets for cash secured puts:

- 16 delta (0.16): Conservative approach, ~16% assignment probability, lower premium

- 30 delta (0.30): Balanced approach, ~30% assignment probability, moderate premium

- 50 delta (0.50): Aggressive approach, ~50% assignment probability, highest premium

When to use each approach depends on your goals and market conditions:

Use 16 delta when you primarily want premium collection with minimal assignment risk. This works well in uncertain markets or on stocks where you’d prefer to avoid ownership despite collecting premium.

Use 30 delta for balanced wheel strategy execution. This strike offers meaningful premium while maintaining reasonable distance from current price. Most wheel traders default to 30 delta as their standard.

Use 50 delta when assignment is acceptable or desired. These at-the-money strikes collect maximum premium but frequently result in assignment. Choose this when you specifically want to acquire shares at current levels.

Distance from Current Price

Beyond delta, consider the strike’s absolute distance from current price. This provides intuitive context beyond probability estimates.

A stock at $100 with these strikes illustrates the concept:

- $90 strike: 10% below current price (conservative)

- $95 strike: 5% below current price (moderate)

- $100 strike: At current price (aggressive)

Conservative traders target 8-12% below current price, providing cushion against adverse moves. Moderate traders accept 4-8% below. Aggressive traders sell at or near current price, maximizing premium while accepting frequent assignment.

Market conditions influence these targets. During high volatility, even 10% OTM strikes collect attractive premium. During low volatility, reaching for 5% OTM might be necessary for worthwhile returns.

Technical Support Levels

Incorporating technical analysis improves strike selection timing. Identify support levels where the stock historically finds buyers, then select strikes at or above these levels.

Technical support identification:

- Previous consolidation zones

- Prior swing lows that held

- Major moving averages (50-day, 200-day)

- Round number psychological levels

- High volume price clusters

Selling the $145 strike on a $160 stock might look good mathematically, but if the stock has clear support at $150, the $150 or $152 strike makes more sense. If assigned, you’re buying at a level where buyers previously appeared, improving your cost basis outlook for the covered call portion of the wheel.

Intraday Timing for Cash Secured Put Entry

Market Open Volatility (Avoid First 30 Minutes)

The first 30 minutes after market open typically shows the widest bid-ask spreads and most erratic price action. Orders placed during this window often receive poor fills due to spread width and rapid price changes.

Wait for the opening surge of volatility to settle. By 10:00-10:30 AM ET, spreads tighten, volume normalizes, and price action becomes more predictable. Your orders receive better fills, directly improving returns.

Opening volatility effects:

- Wide bid-ask spreads (lose money on entry)

- Erratic underlying price movement

- Option pricing adjusting to overnight news

- Lower liquidity in some strikes

- Market maker position adjustments

If you must enter near the open, use limit orders placed at midpoint or better. Never use market orders on options—spread width makes this costly.

Mid-Morning Opportunities (10:00 AM – 11:30 AM ET)

The mid-morning window often provides optimal entry conditions. Opening volatility has settled, but the session is young enough to have active liquidity. Spreads are tighter than at open, and you have a read on the day’s price action.

This timing works especially well when following a specific process:

- Review overnight news and pre-market price action

- Identify stocks meeting your IV and technical criteria

- Wait for market open volatility to settle (30-60 minutes)

- Enter positions with limit orders between 10:00 AM – 11:30 AM ET

Power Hour and Expiration Friday

The final hour of trading (3:00-4:00 PM ET) brings increased volume as traders position for the close. For expiring options, this “power hour” determines final settlement.

On expiration Fridays, positions near the money experience rapid premium decay as time value evaporates completely. If you’re opening new positions (not closing expiring ones), waiting until late in the day on expiration Friday can occasionally offer slight premium advantages due to reduced time value on longer-dated options.

However, power hour shouldn’t be your primary entry window. Mid-morning generally provides better conditions for most traders.

When NOT to Sell Cash Secured Puts

Understanding when to stay away is as important as knowing when to enter. Poor timing transforms a sound strategy into a money-losing mistake.

During Low Implied Volatility

When IV Rank drops below 30%, premiums compress significantly. You’re collecting minimal compensation for risk taken. Unless you specifically want to own the stock at those levels and view the premium as a bonus, low IV environments favor put buyers, not sellers.

Low IV characteristics:

- Thin premiums relative to strike distance

- Complacent market conditions

- Low VIX readings (below 15)

- Boring, steady price action

- Better opportunities in other strategies

Wait for volatility expansion before selling puts. Cash management and patience during low IV periods prevents locking capital into low-return positions.

On Stocks Breaking Down Technically

Never sell puts on stocks violating major support levels unless assignment at unfavorable prices is acceptable. Broken support often becomes resistance, meaning the stock continues falling beyond your strike.

Breakdown warning signs:

- Violation of 200-day moving average on volume

- Breaking multi-month support levels

- Deteriorating relative strength vs market

- High volume selling days

- Leadership rotation away from the sector

If you want to own a broken-down stock, wait for evidence of stabilization—multiple days of support holding, reduced selling volume, or positive divergences in momentum indicators.

Right Before Major Earnings (Unless Experienced)

Pre-earnings premium looks attractive, but unknown binary outcomes create substantial risk. A stock trading at $80 might open at $65 after disappointing results, meaning your $75 put gets assigned $10 in-the-money.

Earnings timing considerations depend on experience level:

Beginners: Close or avoid positions through earnings Intermediate: Sell post-earnings after implied volatility has contracted (reduced premium but known results) Advanced: Selectively sell pre-earnings on specific setups with risk acceptance

The conservative approach closes positions 5-7 days before earnings, avoiding the IV expansion and subsequent crush. This means you miss the elevated premium but also sidestep unknown outcomes.

When You Don’t Want the Stock

This point seems obvious but deserves emphasis: never sell cash secured puts on stocks you don’t want to own. The strategy only works when assignment is acceptable, even welcome.

Assignment isn’t failure—it’s part of the wheel strategy plan. If you’re selling puts hoping they expire worthless while dreading assignment, you’ve mismatched strategy with goals.

Pre-trade assignment test:

- Would I buy shares at this strike price today?

- Am I comfortable holding this stock long-term?

- Does this fit my portfolio allocation?

- Can I manage the position size if assigned?

- What’s my plan for covered calls after assignment?

If any answer is no, find a different stock. Thousands of opportunities exist—never force a trade on the wrong underlying.

Seasonal and Market Cycle Timing

Volatility Expansion Events

Certain events predictably increase market volatility, creating systematic opportunities for cash secured put sellers who prepare in advance.

Volatility expansion catalysts:

- Federal Reserve meeting weeks (increased uncertainty)

- Election seasons (policy uncertainty)

- Geopolitical events (unpredictable impacts)

- Broad market corrections of 5-10% (fear spikes)

- Sector-specific crises (isolated volatility)

Position yourself to sell puts during these events by maintaining cash reserves and watchlists. When volatility expands, premiums double or triple compared to normal conditions.

Tax Loss Harvesting Season (November-December)

Late year tax loss selling creates temporary weakness in stocks held at losses by investors seeking tax deductions. This phenomenon sometimes presents opportunities on quality names experiencing technical selling pressure unrelated to fundamentals.

December bottoms followed by January recoveries (“January effect”) can favor put sellers who position correctly. However, this pattern has weakened in recent years as markets have become more efficient.

Post-Earnings IV Crush Opportunities

After earnings announcements, implied volatility typically collapses as uncertainty resolves. While this IV crush hurts options held through earnings, it creates opportunities for establishing new positions.

Consider this timing sequence:

- Stock reports earnings (IV high, avoid selling)

- Results announced, stock direction clear (IV still elevated)

- 1-3 days post-earnings, IV normalizes (opportunity window)

The 24-72 hours after earnings can offer ideal setups—recent news is processed, direction is clearer, but premiums haven’t fully normalized. This window provides better risk-reward than either pre-earnings (unknown outcome) or fully normalized periods (compressed premium).

Position Management Timing After Entry

Once you’ve entered a cash secured put position, timing continues to matter through position management.

Taking Profits at 50-80%

Many successful options sellers target closing winners when they’ve captured 50-80% of maximum profit. A put sold for $2.00 could be bought back at $1.00 (50% profit) or $0.40 (80% profit).

Why close early rather than waiting for 100%:

- Accelerating time decay makes final premium sticky

- Frees capital for new opportunities

- Removes tail risk of adverse moves

- Improves risk-adjusted returns

- Reduces monitoring time

Research by tastytrade found that taking profits at 50% of max profit with 21+ DTE remaining optimized risk-adjusted returns for premium sellers. This means if you sold a 45 DTE put for $2.00, consider closing it when it reaches $1.00 with 3+ weeks remaining.

Rolling to Avoid Assignment

When a short put moves in-the-money as expiration approaches, you face a decision: accept assignment or roll to a future expiration.

Rolling timing considerations:

- Roll when you can collect additional credit

- Typically roll 7-10 days before expiration

- Roll out in time, potentially down in strike

- Ensure new position still meets your criteria

Rolling down and out—to a lower strike and later expiration—allows you to collect additional credit while reducing your cost basis further. This management technique keeps you in premium collection mode while avoiding unfavorable assignments.

Here’s where most traders struggle after getting assigned: calculating your actual cost basis. Your broker shows the strike price, but your real cost is strike minus all premium collected. You need to track this manually for tax purposes and decision making.

Tool Tip: QuantWheel automatically tracks cost basis

adjustments after assignment — useful if you're managing

10+ wheel positions simultaneously.

Knowing When to Accept Assignment

Assignment isn’t failure—it’s the transition to the covered call phase of the wheel. Accept assignment when:

Assignment is acceptable when:

- You collected solid premium on the CSP

- Stock fundamentals remain attractive

- Technical analysis shows support near strike

- You have clear covered call strategy planned

- Position size fits portfolio allocation

After assignment, immediately establish your covered call plan. Determine strike selection (resistance levels), expiration timeline (typically 30-45 DTE again), and exit criteria. Assignment begins the second half of the wheel, not a problem to solve.

Combining Indicators for Optimal Entry Timing

No single indicator provides perfect entry signals. Combining multiple factors creates a more robust timing framework.

The Timing Checklist

Before selling any cash secured put, verify these conditions:

Market conditions:

- IV Rank above 50% (preferably 60%+)

- VIX above 15 or in rising trend

- Market environment favorable for premium selling

Stock-specific conditions:

- Genuinely willing to own at strike price

- Stock in uptrend or consolidation (not breakdown)

- Strike near technical support level

- Reasonable premium-to-risk ratio

Technical timing:

- After minor pullback (improved entry)

- Support visible on chart at strike level

- Volume patterns support current trend

- No imminent earnings in next 7-14 days (unless comfortable)

Execution timing:

- 30-60 minutes after market open (avoid opening volatility)

- Limit orders at midpoint or better

- Liquid strikes with tight bid-ask spreads

Position management plan:

- Profit target defined (typically 50-80% of max profit)

- Exit strategy if position moves against you

- Assignment plan if struck

- Position size appropriate for account

When all or most factors align, you have a high-probability setup. When several are missing, the opportunity likely exists elsewhere.

Real-World Timing Examples

Example 1: High IV Opportunity

Setup: AMD trading at $165, IV Rank at 68% (elevated), stock consolidated for 3 weeks after rally, clear support at $155 level, 38 days until monthly expiration.

Analysis: All timing factors align—high IV provides premium, consolidation suggests stability, support visible at $155, adequate time to expiration.

Trade: Sell $155 strike cash secured put, collect $5.20 premium ($520 per contract).

Outcome possibilities:

- AMD stays above $155: Keep $520 premium (3.2% return in 38 days, ~30% annualized)

- AMD assigned at $155: Actual cost $149.80 ($155 – $5.20), 9.2% below current price

- Close at 50% profit: Buy back at $2.60 after 2-3 weeks, 1.6% return in ~20 days

This timing captured elevated premium during consolidation with clear support, stacking multiple factors favorably.

Example 2: Poor Timing (What to Avoid)

Setup: NVDA trading at $880, IV Rank at 22% (low), stock up 40% in 8 weeks with no pullback, earnings in 5 days, no clear support until $750.

Analysis: Multiple warning signs—low IV (thin premium), extended move without rest (reversal risk), imminent earnings (binary risk), weak support (large decline possible).

Potential trade: Sell $850 strike, collect only $8.50 premium.

Why avoid: The $8.50 premium (1% return) doesn’t compensate for earnings uncertainty and lack of support. If earnings disappoint, NVDA could gap to $750-$800, meaning assignment at $850 with immediate 6-11% unrealized loss. Better opportunities exist.

This timing ignored multiple warning signs in favor of a recognizable name, a common beginner mistake.

Advanced Timing Strategies

Scaling Into Positions

Rather than deploying all capital into a single strike, consider scaling into positions across time or strikes.

Time-based scaling: Sell one contract now, another in 1-2 weeks, a third in 3-4 weeks. This averages entry timing and captures different volatility environments.

Strike-based scaling: Sell multiple strikes simultaneously—one at 16 delta (conservative), one at 30 delta (balanced). This diversifies assignment probability while maintaining premium collection.

Pairing with Technical Analysis

Combining cash secured puts with technical entry signals improves timing precision.

Technical entry triggers:

- Stock bounces off moving average support (50-day or 200-day)

- RSI shows oversold reading (<30) then bounces

- Price tests and holds prior consolidation low

- Bullish candlestick reversal patterns at support

Wait for technical confirmation rather than selling puts during active declines. The difference between catching a falling knife and buying support is patience.

Using Volatility Skew

Volatility skew describes the difference in implied volatility between different strikes. Put skew typically shows higher IV on lower strikes (downside protection demand).

When skew is steep, lower strikes offer disproportionately high premium. When skew is flat, strikes are more evenly priced. This affects strike selection timing—steep skew favors slightly lower strikes, flat skew favors closer strikes.

Common Timing Mistakes to Avoid

Mistake 1: Chasing Premium Without Considering Assignment

High premium doesn’t automatically mean good opportunity. Often, elevated premium signals elevated risk—deteriorating fundamentals, broken technicals, or imminent catalysts.

Always ask: “Why is this premium so high?” The answer usually reveals whether the opportunity is genuine (temporary volatility spike) or warning sign (market pricing in problems).

Mistake 2: Selling Weekly Options Constantly

Weekly options seduce traders with rapid time decay, but the compressed timeframe creates challenges. One adverse move leaves no time to manage the position. Transaction costs accumulate quickly with weekly trading.

Establish consistency with 30-45 DTE positions before exploring weeklies. Speed isn’t always better.

Mistake 3: Ignoring Market Environment

Individual stock analysis matters, but broad market conditions influence outcomes significantly. Selling puts aggressively during deteriorating market environments leads to multiple simultaneous losing positions.

Monitor overall market health using indicators like VIX trend, market breadth, and sector rotation. During broad market weakness, reduce position sizing even on quality individual setups.

Mistake 4: Selling Puts During Low Volatility

Impatience during low IV periods causes traders to sell puts collecting insufficient premium. The minimal returns don’t justify the risk or capital commitment.

Accept that some market environments favor cash preservation. Waiting for proper conditions is a trading decision, not missing opportunities.

Building Your Personal Timing Framework

The “best” timing varies by individual goals, risk tolerance, and account size. Construct your framework using these components:

Define Your Criteria

Write down your specific entry requirements:

- Minimum IV Rank threshold

- Preferred DTE range

- Delta targets for strikes

- Technical indicators you follow

- Market conditions you require

- Minimum premium targets

Track and Refine

Maintain a trading journal documenting:

- Entry timing conditions for each trade

- IV Rank at entry

- Time to expiration selected

- Outcome (profit, loss, assignment)

- What worked and what didn’t

Over time, patterns emerge showing which timing combinations work best for your style and goals. Refine your criteria based on results, not opinions or single data points.

Automate Where Possible

Manual screening across hundreds of stocks for multiple criteria becomes time-consuming. Tools that scan for your specific criteria—IV Rank thresholds, technical setups, delta targets—free you to focus on analysis and execution rather than screening.

This is where QuantWheel’s screener helps—it filters specifically for wheel strategy criteria across 500+ tickers in minutes. Set your IV Rank minimum, preferred DTE, target delta, and fundamental filters, then review only qualified candidates. This automation means you catch opportunities during volatility spikes without manually checking every ticker.

Conclusion: Timing as Competitive Advantage

Knowing when to sell cash secured puts transforms the strategy from random premium collection to systematic income generation. The difference between collecting 1% monthly returns and 2-3% monthly returns often comes down to timing—entering when all factors align rather than forcing trades during suboptimal conditions.

The checklist approach—verifying IV levels, technical support, appropriate DTE, and favorable market conditions—creates consistency. Not every trade meets all criteria, but the best risk-reward opportunities align multiple factors simultaneously.

Assignment isn’t failure when you’ve timed entries well. You own a stock you wanted, at a price below where you started, with premium already collected. The wheel continues with covered calls.

Patient capital deployed at optimal times outperforms aggressive capital deployed constantly. Master timing, and cash secured puts become a reliable portfolio component rather than a speculative gamble.

Start your free trial of QuantWheel to get automated IV Rank alerts, position tracking through assignments, and faster screening for wheel strategy opportunities.

Start your free trial of QuantWheel →

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.