You want to generate income from your cash while potentially buying stocks at a discount. You've heard about cash secured puts, but you're not quite sure how cash secured puts work or whether they're right for you.

Here's what most investors don't realize: cash secured puts are essentially getting paid to set a limit buy order. Instead of waiting passively for a stock to drop to your target price, you collect immediate income for your willingness to buy a stock.

In this comprehensive guide, I'll walk you through exactly how cash secured puts work, the mechanics behind them, real examples with numbers, and the honest risks you need to understand before your first trade.

TL;DR: How Cash Secured Puts Work

What it is: A cash secured put means you sell a put option contract while keeping enough cash in your account to buy 100 shares of the underlying stock. You receive a premium (payment) upfront for taking on the obligation to potentially buy the stock.

How it works: You choose a stock, pick a strike price below the current price, and sell a put option. You immediately receive premium income. At expiration, one of two things happens: either the stock stays above your strike (you keep the premium and the trade ends), or it falls below your strike (you buy 100 shares at the strike price using your cash).

Simple example: Apple (AAPL) trades at $180. You sell a $170 put and collect $300 premium. If AAPL stays above $170 by expiration, you keep the $300. If it drops to $165, you buy 100 shares at $170, but your real cost is $167 per share ($170 strike - $3 premium collected).

Risk and reward: Your maximum profit is the premium collected. Your maximum loss is the strike price minus premium (if the stock goes to zero). You're essentially saying "I'm willing to buy this stock at this price, and I want to get paid to wait."

Best for: Investors who want income generation, are willing to own quality stocks long-term, and are comfortable with the obligation to buy shares if assigned. Not suitable for traders who fear stock ownership or volatile, low-quality stocks.

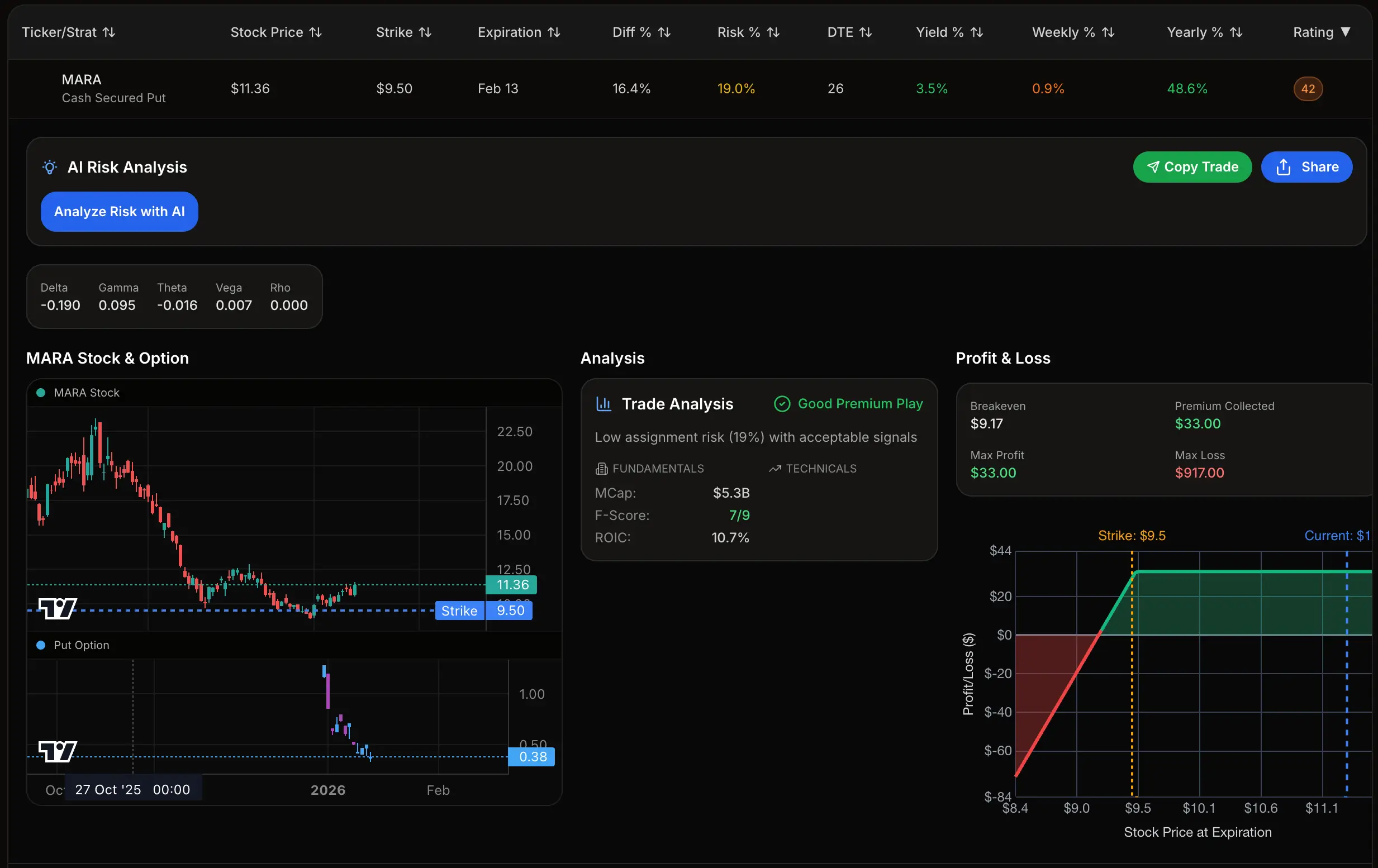

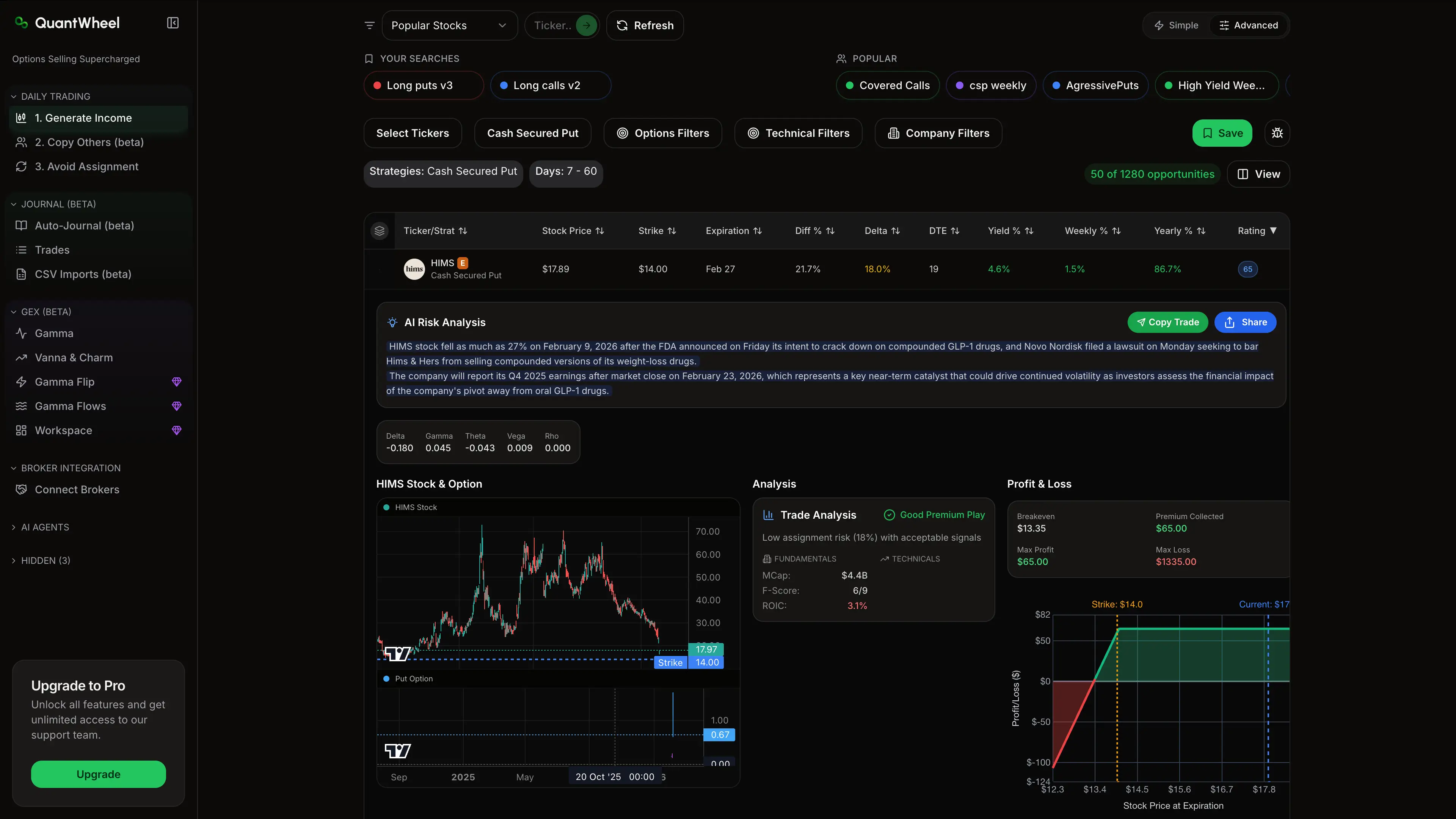

Example trade:

Other similar trades that QuantWheel has surfaced:

Find trades like this inside QuantWheel →

What Is a Cash Secured Put?

A cash secured put is an options strategy where you sell a put option contract while maintaining enough cash in your brokerage account to purchase 100 shares of the underlying stock at the strike price if you're assigned.

Let's break down what that actually means in plain language.

When you sell a put option, you're entering into a contract with another trader. That trader is buying the right to sell you 100 shares of a specific stock at a specific price (the strike price) by a specific date (the expiration date). In exchange for giving them this right, they pay you money upfront called the premium.

The "cash secured" part is crucial. Your broker requires you to have enough cash in your account to fulfill your obligation—buying 100 shares at the strike price if you're assigned. This cash acts as collateral and must remain in your account until the option expires or you close the position.

Think of it like this: You're telling the market "I'm willing to buy this stock at this price, and I want to get paid to wait." If the stock never reaches your price, you keep the payment. If it does reach your price, you buy the stock just like you planned, but at a discount because of the premium you collected.

The Key Components

Every cash secured put has four essential elements you need to understand:

The Underlying Stock: This is the company whose shares you're agreeing to potentially buy. You should only sell puts on stocks you actually want to own at the strike price you choose.

The Strike Price: This is the price at which you agree to buy 100 shares if assigned. It's typically set below the current market price. The closer to the current price, the more premium you collect but the higher your chance of assignment.

The Expiration Date: This is when the contract ends. Common timeframes range from weekly (7 days) to monthly (30-45 days) to longer-dated LEAPS. Most traders favor 30-45 days for the optimal balance between premium collection and time commitment.

The Premium: This is the money you receive immediately when you sell the put. It's yours to keep regardless of what happens. The premium is your maximum profit on the trade.

How Cash Secured Puts Differ from Regular Puts

There's an important distinction to understand: when you sell a cash secured put, you're the seller (also called the writer) of the put contract, not the buyer.

Most beginners learn about buying puts first—betting that a stock will go down. That's the opposite of what we're doing here. When you sell puts, you're taking the other side of that trade. You're betting the stock will stay flat or go up, and you're collecting money from the person who thinks it might go down.

The "cash secured" designation distinguishes this from a "naked put," which is when you sell puts without having the cash to cover assignment. Naked puts involve margin and unlimited risk potential. Cash secured puts are defined-risk because you have the full cash amount set aside.

The Mechanics: Step-by-Step How Cash Secured Puts Work

Let's walk through the complete lifecycle of a cash secured put trade so you can see exactly how this strategy works in practice.

Step 1: Select Your Stock and Strike Price

The first step is choosing a stock you genuinely want to own. This isn't about speculation—it's about identifying quality companies you'd be comfortable holding long-term.

Let's use Microsoft (MSFT) as our example. Suppose MSFT is currently trading at $380 per share. You believe it's a solid company, and you'd be happy to own it at $370 or lower.

You look at the options chain and see that the $370 put expiring in 30 days is trading for $5.00. This means if you sell one contract (representing 100 shares), you'll collect $500 in premium ($5.00 × 100 shares).

Your strike selection should be based on several factors: your desired purchase price, the premium you want to collect, and the probability of assignment. Strikes closer to the current stock price pay more premium but have higher assignment probability.

Step 2: Sell the Put Option

When you're ready to enter the trade, you sell to open one put contract. Here's what happens at execution:

Your account immediately receives: $500 premium (minus commission, typically $0.65)

Your broker sets aside: $37,000 in cash ($370 strike × 100 shares)

Your obligation: Buy 100 shares of MSFT at $370 if assigned before expiration

You now have an open short put position. The $500 is yours to keep no matter what happens next. This money hits your account instantly and is available for withdrawal or reinvestment (though you'll want to keep it as part of your cash cushion).

Step 3: Wait Until Expiration

Now you wait. During this waiting period, three scenarios can unfold, and understanding each is essential.

Scenario A: The stock stays above your strike price. This is your best-case scenario. If MSFT remains above $370 through expiration, the put expires worthless. You keep the full $500 premium, your $37,000 is released back to you, and you can repeat the process with a new put sale if desired. This is a profitable trade with a 100% return on the premium collected.

Scenario B: The stock drops below your strike price but you close early. If MSFT drops to $365 before expiration, your put is now "in the money" and has increased in value. You have the option to buy it back (buy to close) to exit the position. You might do this if you no longer want to own the stock or if you can roll the position to a later date for additional premium.

Scenario C: The stock is below your strike at expiration. If MSFT is trading at $365 on expiration day, you'll be assigned. Your broker automatically uses your $37,000 cash to purchase 100 shares at $370 per share, even though the market price is lower.

Here's a good trade that QuantWheel has found.

Find trades like this inside QuantWheel →

Step 4: Assignment and Cost Basis (If Below Strike)

If you're assigned, here's what happens in your account:

Debit: $37,000 (to purchase 100 shares at $370 each)

Credit: 100 shares of MSFT added to your portfolio

Your actual cost basis: $365 per share ($370 strike - $5 premium collected)

This is a critical point that many brokers get wrong in their accounting. Your broker will show your purchase price as $370, but your real economic cost is $365 because you already collected $500 in premium upfront. This $5 per share discount is your edge.

Here's where most wheel traders struggle: calculating your actual cost basis after assignment. Your broker shows $370, but your real basis is $365 after the $500 premium. This becomes critical for tracking performance, making roll decisions, and tax reporting.

This is exactly why platforms like QuantWheel exist—to automatically track your true cost basis through assignments so you don't have to maintain complex spreadsheets. QuantWheel adjusts your cost basis automatically when assignments happen, saving you the manual math and potential errors.

Step 5: What to Do After Assignment

Once you own the shares, you have several choices for your next move:

Hold the shares long-term. If you still like the stock at your adjusted cost basis, simply hold. You now own a quality company at a discount to where it was when you started the trade.

Sell covered calls. This is where the "wheel strategy" continues. You can sell call options against your shares to generate additional income. This strategy of selling puts, getting assigned, then selling calls is called "running the wheel."

Sell the shares. If the stock has recovered or you've changed your thesis, you can simply sell the shares at market price. Your profit or loss will be based on your actual $365 cost basis, not the $370 strike.

The key insight: assignment isn't failure. It's part of the plan. You collected premium to buy a stock you wanted at a price you chose. That's a successful trade execution, even if you're temporarily showing an unrealized loss.

Cash Secured Put Example with Real Numbers

Let's walk through three complete examples showing the different outcomes so you can see exactly how the math works in practice.

Example 1: Stock Stays Above Strike (Win)

Setup:

- Stock: Advanced Micro Devices (AMD)

- Current price: $155

- Strike sold: $145 (30 days to expiration)

- Premium collected: $380 ($3.80 per share)

- Cash required: $14,500

At Expiration (30 days later):

- AMD closes at $160 (above your $145 strike)

- The put expires worthless

- You keep the full $380 premium

Results:

- Profit: $380

- Time: 30 days

- Return on capital: 2.62% ($380 / $14,500)

- Annualized return: ~31.4%

- Cash released: $14,500 (available for next trade)

This is your ideal outcome. You collected income, tied up your capital for 30 days, and now have everything back plus profit to deploy again.

Example 2: Stock Drops Below Strike (Assignment)

Setup:

- Stock: Palantir Technologies (PLTR)

- Current price: $28

- Strike sold: $25 (45 days to expiration)

- Premium collected: $150 ($1.50 per share)

- Cash required: $2,500

At Expiration (45 days later):

- PLTR closes at $23 (below your $25 strike)

- You are assigned 100 shares at $25

Results:

- Shares owned: 100 PLTR at $25 strike

- Actual cost basis: $23.50 ($25 - $1.50 premium)

- Current market price: $23

- Unrealized loss: $50 ($23 market - $23.50 cost basis)

- But you're still better than buying at $28 originally (saved $5/share = $500)

Next move: You now own 100 shares. You can:

- Hold PLTR long-term (down only $50 vs down $500 if bought at original price)

- Sell covered calls at $26-27 strike to generate income

- Sell shares if your thesis changed (realize the $50 loss)

Even though you're showing a small unrealized loss, you're in a much better position than someone who bought shares at $28. You effectively bought at an 8% discount to the original price.

Example 3: Early Management (Stock Drops, You Close)

Setup:

- Stock: Nvidia (NVDA)

- Current price: $480

- Strike sold: $450 (30 days to expiration)

- Premium collected: $800 ($8 per share)

- Cash required: $45,000

15 Days Later:

- NVDA drops to $440 (below your strike)

- Your put is now worth $14 (has increased in value)

- You decide you no longer want to own NVDA at this price

Results:

- You buy back the put for $1,400 to close

- Your net result: -$600 ($800 collected - $1,400 paid to close)

- Loss: $600

- Cash released: $45,000

- No assignment occurred

This example shows active management. You took a $600 loss to avoid a $45,000 stock purchase you no longer wanted. This is a risk management decision—you controlled your position rather than being forced into ownership.

The key learning: you can always close a cash secured put before expiration by buying it back. This gives you flexibility to manage risk, but it will cost more than you collected if the stock moved against you.

The Risk and Reward Profile of Cash Secured Puts

Let's be completely honest about what you're risking and what you stand to gain with this strategy. Conservative positioning means understanding both sides clearly.

Maximum Profit Potential

Your maximum profit is limited to the premium you collect when selling the put. That's it. No matter how high the stock goes, you don't make any more money than the premium.

Using our MSFT example: if you collect $500 selling the $370 put, your maximum profit is $500. Even if MSFT rockets to $500 per share, you still only keep the $500 premium.

This is the key trade-off: limited upside in exchange for immediate income and high probability of profit. Cash secured puts typically have a 60-80% probability of expiring worthless (profitable) depending on your strike selection.

For context on returns: if you're tying up $37,000 to collect $500 over 30 days, that's a 1.35% return in one month, or roughly 16.2% annualized if you could repeat this monthly. These are solid returns, but they're not explosive. This is a consistency play, not a home run strategy.

Maximum Loss Potential

Your maximum loss occurs if the stock drops to zero. In that scenario, you'd be forced to buy worthless shares at your strike price, losing nearly your entire cash.

Maximum loss formula: (Strike Price × 100) - Premium Collected

Using our MSFT example: ($370 × 100) - $500 = $36,500 maximum loss

However, this maximum loss scenario is extremely unlikely with quality stocks. Microsoft going to zero would require catastrophic business failure. Still, you need to acknowledge this theoretical risk.

The more realistic risk is moderate drawdown. If MSFT drops to $340 (an 8% decline from $370), you'd be sitting on an unrealized loss of $2,500 on your shares: ($370 cost - $340 market value) × 100 shares - $500 premium = $2,500 loss.

This is where many beginners panic. You're down $2,500 on paper. But remember: you chose to potentially buy MSFT at $370 because you believed in the company long-term. The stock being temporarily below your cost basis doesn't mean the trade was wrong—it means you now own shares you wanted.

The Honest Risk Discussion

Here's what can actually go wrong with cash secured puts, beyond the theoretical scenarios:

Capital tie-up risk: Your cash is locked up for the duration of the trade. If a better opportunity appears or you need the money, you're either stuck waiting or paying to close the position at a loss.

Assignment at the worst time: Stocks often drop during market sell-offs. You might get assigned when everything looks scary and you're least comfortable deploying capital. This tests your conviction.

Declining stock risk: If you're assigned on a stock that continues declining, you can face substantial unrealized losses. A stock that drops from $370 to $320 means you're sitting on a $5,000 unrealized loss (minus the $500 premium = $4,500 net loss).

Opportunity cost: In a raging bull market, your cash sits aside earning small premiums while stock owners enjoy larger gains. You miss the upside beyond your premium.

Black swan events: Dramatic drops, bankruptcy rumors, fraud revelations—rare but catastrophic events can decimate your position overnight. This is why stock selection is critical.

The bottom line: cash secured puts are conservative compared to many options strategies, but they're not risk-free. You're taking on stock ownership risk in exchange for upfront income. If you're not comfortable owning the stock at your strike price, don't sell the put.

When to Use Cash Secured Puts (and When Not To)

Cash secured puts aren't appropriate for every situation. Here's an honest framework for when this strategy makes sense and when it doesn't.

When Cash Secured Puts Work Well

You want to own the stock anyway. This is the golden rule. If you were planning to buy shares of Apple at $170 or below, selling the $170 put means you get paid to wait for your target price. Best case: the stock never hits $170 and you keep the premium. Worst case: you buy shares at the exact price you wanted.

You're neutral to bullish on a quality stock. Cash secured puts profit when stocks stay flat or rise. If you believe a stock will hold its current level or drift higher over the next 30-45 days, selling puts captures time decay (theta) while the stock proves you right.

You want to generate income from cash. Instead of letting $25,000 sit in your account earning 4-5% in a money market fund, you can rotate that capital through cash secured puts earning 1-3% per month (12-36% annualized) on quality stocks. The risk is higher than cash, but so is the return potential.

Volatility is elevated. When implied volatility (IV) is high, option premiums are expensive. This is ideal for sellers. If you're selling puts when IV is in the 60th percentile or higher, you're collecting above-average premium for the same risk. After earnings announcements or market sell-offs are often good times.

You have patience and discipline. Cash secured puts require you to stick to your plan. If you're the type who panics when stocks drop or constantly second-guesses your entries, this strategy will be frustrating. But if you can set your price, collect premium, and wait without emotional interference, this strategy fits your temperament.

When Cash Secured Puts Don't Work

You don't actually want to own the stock. Selling puts on meme stocks, speculative biotechs, or companies you haven't researched is gambling. If you'd never buy shares, don't sell puts. Assignment will leave you owning something you don't understand.

The stock is in a clear downtrend. Fighting a downtrend by selling puts is dangerous. If a stock is dropping 3-5% per week consistently, your premium won't compensate for assignment risk. Respect the trend. Wait for stabilization before selling puts.

You need the cash soon. Don't sell puts with money you need in the next 30-60 days. If your money is locked up as collateral and you need it for an emergency, you'll be forced to close at an inopportune time, likely at a loss.

Volatility is extremely low. When IV is in the 20th percentile or lower, premiums are tiny. You might collect $50-100 for tying up $25,000 for a month. The juice isn't worth the squeeze. Wait for IV to expand.

You're trying to "make up" for losses. Revenge trading by selling aggressive puts on declining stocks rarely works. If you lost money elsewhere and need to recover quickly, cash secured puts won't provide the explosive returns you're hoping for. Stick to your process.

You don't have enough capital. Each put requires 100 × strike price in cash. For a $100 stock, that's $10,000 per contract. If you only have $5,000 total, you can't properly implement this strategy on most stocks. You need adequate capital per position.

The Stock Selection Criteria

Not all stocks are created equal for cash secured puts. Here's what to look for:

Quality fundamentals: Strong balance sheets, positive earnings, reasonable valuations. You want companies that will still exist and thrive in 5 years.

Adequate liquidity: The options should have tight bid-ask spreads and daily volume. Aim for stocks with at least 500+ options contracts traded daily in your target strike.

Reasonable volatility: Some volatility is good (generates premium), but extreme volatility means extreme risk. Target stocks with IV rank between 40-70th percentile for the sweet spot.

You understand the business: Don't sell puts on complex sectors you can't evaluate. Stick to companies whose products, competitive advantages, and risks you can articulate.

Long-term bullish outlook: Even if the stock dips short-term, you believe it will recover and grow over months and years. This conviction allows you to hold through temporary drawdowns.

Cash Secured Puts vs Other Strategies

Understanding how cash secured puts compare to alternative approaches helps you know when to use this strategy versus others.

Cash Secured Puts vs Buying Stock Outright

Buying stock: You pay $370 per share to own MSFT immediately. You participate in all upside. If MSFT goes to $420, you gain $50 per share ($5,000 total). Your breakeven is your purchase price.

Selling puts: You collect $5 per share to potentially buy at $370. If MSFT goes to $420, you only keep your $500 premium (the stock never reaches your strike). If MSFT drops to $360, you buy at $370 but your real cost is $365 (better than buying at $370, worse than buying at $360).

The tradeoff: Cash secured puts give you income and a slightly better entry price, but you sacrifice unlimited upside. You're trading the chance of large gains for higher probability of smaller gains plus downside protection.

When to buy stock instead: If you're highly bullish and expect significant upside (10%+ moves), just buy the stock. Don't cap your gains for a small premium. Cash secured puts work best in neutral to moderately bullish environments.

Cash Secured Puts vs Covered Calls

These are opposite sides of the wheel strategy.

Covered calls: You own 100 shares and sell call options, generating income while capping upside. Risk: you own the shares, so if the stock drops $20, you lose $2,000 (minus your call premium).

Cash secured puts: You hold cash and sell put options, generating income while potentially acquiring shares at a discount. Risk: you might be forced to buy shares in a declining stock.

The relationship: Many traders use both in sequence. Sell puts to acquire shares, then sell calls on those shares for additional income. This is the wheel strategy. The put phase generates income while waiting to own shares. The call phase generates income on shares you own.

Cash Secured Puts vs Credit Spreads

A credit spread involves selling a put and simultaneously buying a further out-of-the-money put for protection.

Credit spread example: Sell the $370 put, buy the $360 put. Your max loss is now $1,000 (the $10 width minus premium collected) instead of $36,500. But you collect less premium—maybe $200 instead of $500.

The tradeoff: Credit spreads reduce risk and capital requirements but also reduce profit potential. You're buying insurance on your trade. With cash secured puts, you take full risk to collect full premium.

When to use credit spreads instead: If you want to trade more contracts with less capital, or if you're trading on stocks you don't want to own (more speculative). Credit spreads are position-trading tools. Cash secured puts are stock acquisition tools.

Cash Secured Puts vs The Wheel Strategy

Cash secured puts are actually the first step in the wheel strategy, not a separate strategy.

The Wheel: Sell puts → Get assigned → Sell calls → Shares called away → Sell puts again. It's a complete cycle designed to generate consistent income on quality stocks you're willing to own.

Cash secured puts alone: You're just doing the first step repeatedly. You might never get assigned, in which case you're collecting premium perpetually without ever owning shares.

Most serious options income traders eventually transition from just selling puts to running the full wheel because it provides more opportunities to collect premium and works in more market conditions.

Common Mistakes When Selling Cash Secured Puts

Here are the costly errors beginners make and how to avoid them.

Mistake 1: Selling Puts on Stocks You Don't Want to Own

This is the #1 mistake. Traders get attracted by large premiums on volatile, risky stocks. They sell puts thinking "I'll just collect the premium and never get assigned."

Then the stock drops 30%, they're assigned, and they're stuck holding shares of a company they never wanted in the first place. Now they're facing losses they can't tolerate.

The fix: Only sell puts on stocks you've researched and genuinely want to own at your strike price. Ask yourself: "If I'm assigned tomorrow, am I happy owning this stock?" If the answer isn't yes, don't sell the put.

Mistake 2: Chasing High Premiums

Big premiums are tempting. But there's usually a reason a put pays 10% premium in 30 days—the stock is extremely risky or in a downtrend.

High premium = high implied volatility = high risk. You're being paid more because the probability of assignment is higher and the potential drawdown is larger.

The fix: Target premiums in the 1-3% monthly range on quality stocks. That annualizes to 12-36% returns, which is excellent without excessive risk. Don't reach for 5-8% monthly premiums unless you truly understand and accept the risk.

Mistake 3: Not Having an Assignment Plan

Many traders sell puts without thinking through what happens if they're assigned. They panic when they see 100 shares appear in their account, especially if the stock has dropped further.

The fix: Before selling any put, decide: "If I'm assigned, will I hold the shares long-term, sell covered calls, or exit immediately?" Having this plan prevents emotional decisions during assignment.

Mistake 4: Letting Winners Turn into Losers

You sell a put, collect $500 premium, and two weeks later it's up 80% (the put is now worth only $100). Instead of closing for a $400 profit, you hold for the last $100.

Then the stock drops, the put moves back against you, and your $400 profit turns into a $200 profit or even a loss.

The fix: Consider closing puts when you've captured 50-75% of the maximum profit with 21+ days to expiration remaining. You free up capital faster and can redeploy into new trades. The last 25% of profit often isn't worth the risk.

Mistake 5: Over-Concentrating in One Stock

You sell 5 put contracts on the same stock because you're very bullish. Then the stock drops and you're assigned on all 5 contracts, meaning you own 500 shares (potentially $50,000+) in one position.

This concentration risk can devastate your portfolio if that one company underperforms.

The fix: Limit position size. A good rule: no single stock should represent more than 10-15% of your portfolio. If you have $100,000, don't sell more than 2-3 puts on any single stock (depending on strike price).

Mistake 6: Ignoring Earnings Dates

Earnings announcements cause volatility spikes. If you sell a put 3 days before earnings without realizing it, you might experience a 10-20% drop overnight if results disappoint.

The fix: Always check earnings dates before selling puts. Many traders avoid holding through earnings entirely. If you do hold through earnings, reduce position size to account for the additional risk, or close before the announcement.

Mistake 7: Not Tracking Your Real Cost Basis

Your broker shows you were assigned at $370. But you collected $5 premium, so your real cost is $365. If you don't track this properly, you might make poor decisions about when to exit or sell calls.

Here's where most wheel traders struggle: calculating your actual cost basis after assignment. Your broker shows $370, but your real basis is $365 after the $500 premium. This becomes critical for tracking performance, making roll decisions, and tax reporting.

This is exactly why platforms like QuantWheel exist—to automatically track your true cost basis through assignments so you don't have to maintain complex spreadsheets. QuantWheel adjusts your cost basis automatically when assignments happen, eliminating the manual tracking headache.

The fix without automation: Maintain a spreadsheet tracking: strike price, premium collected, assignment date, and calculated real cost basis. Refer to this for all position management decisions, not your broker's numbers.

Advanced Tactics for Cash Secured Puts

Once you understand the basics, these advanced techniques can improve your results.

Rolling Puts for Additional Credit

If your put is in danger of assignment and you want to avoid it or delay it, you can "roll" the position.

How rolling works: You simultaneously buy back your current put (closing it) and sell a new put at a later expiration date, potentially at a different strike. The goal is to collect additional premium and give the trade more time to work.

Example: You sold the MSFT $370 put for $5. MSFT drops to $365 with one week to expiration. Your put is now worth $7 (you'd lose $200 to close).

Instead, you roll: Buy back the $370 put for $7, simultaneously sell the $370 put expiring 30 days later for $9. Your net credit is $2 ($900 - $700). You've collected $200 more premium and extended your trade by 30 days.

When to roll: Consider rolling when you still want to own the stock, but you want to collect more premium or give the trade time to recover. Rolling works best when you can collect additional credit.

When not to roll: If your thesis on the stock has changed and you no longer want to own it, rolling just delays the inevitable. Take your loss and move on rather than doubling down on a bad trade.

Selling Puts During High IV Events

Implied volatility spikes during market sell-offs, earnings season, or company-specific news. These are often excellent times to sell puts because premiums are elevated.

The strategy: When a quality stock drops 5-10% on broad market fear (not company-specific problems), IV often spikes to the 70th-80th percentile. This is when puts are "expensive" and you're getting paid well above normal premium.

Example: Tech stocks sell off because of Fed rate concerns. NVDA drops from $480 to $440, and the 30-day $420 put that normally pays $6 is now paying $11 due to elevated IV. If you believe the sell-off is temporary, this is a prime opportunity to sell puts at inflated premiums.

The caution: High IV usually means high actual volatility is expected. Don't assume volatility is "wrong"—the market might know something you don't. Only sell puts on stocks you've researched and believe are overreacting.

Laddering Expirations

Instead of selling all your puts at the same expiration, stagger them across multiple dates. This creates a smoother premium collection schedule and reduces timing risk.

Example with $50,000 capital:

- Week 1: Sell 1 put expiring in 30 days

- Week 2: Sell 1 put expiring in 30 days

- Week 3: Sell 1 put expiring in 30 days

- Week 4: Sell 1 put expiring in 30 days

Now you have puts expiring every week, creating weekly premium collection and allowing weekly capital redeployment. This smooths out your income stream and gives you multiple chances to adjust if market conditions change.

Pairing Puts with The Wheel Strategy

Cash secured puts work best as the entry mechanism for the full wheel strategy.

The complete wheel:

- Sell cash secured puts on quality stock (you want to own it)

- If assigned, own the shares at your strike (minus premium)

- Sell covered calls on the assigned shares above your cost basis

- If shares are called away, return to step 1

- If shares aren't called away, keep selling calls and collecting premium

This creates a perpetual income cycle. You're collecting premium whether you own shares or not. When you own shares, you sell calls. When you don't, you sell puts. The wheel keeps turning.

The cash secured put phase is often the most comfortable because you haven't deployed capital yet—you're just collecting premium while waiting to own stocks you want.

Getting Started with Cash Secured Puts

If you're ready to start implementing this strategy, here's a practical step-by-step approach.

Step 1: Ensure You're Qualified

Check with your broker that you have Level 2 options approval (selling cash secured puts). Most brokers require you to:

- Have a margin account (even though you're using cash)

- Complete an options trading application

- Acknowledge understanding of options risk

- Sometimes meet minimum account value requirements ($2,000-5,000)

If you don't have approval, apply through your broker's website. Approval usually takes 1-2 business days.

Step 2: Set Up Your Watchlist

Create a list of 10-15 quality stocks you'd be happy to own long-term. Consider:

- Large-cap, financially stable companies

- Stocks you understand and have researched

- Companies with decent options volume (check daily volume on the options chain)

- Mix of sectors to maintain diversification

Example starter watchlist: AAPL, MSFT, GOOGL, AMD, NVDA, PLTR, DIS, COST, JPM, V

Step 3: Learn to Read the Options Chain

Open your broker's options trading interface and pull up the options chain for one of your watchlist stocks. You'll see:

- Calls on one side, puts on the other

- Strike prices down the middle

- Bid and ask prices (the "bid" is what you'll receive when selling)

- Volume and open interest (higher is better for liquidity)

- Greeks (delta, theta, etc.—we'll get to these later)

For cash secured puts, you're looking at the put side. Find strikes below the current stock price with reasonable bid prices.

Step 4: Run Your First Paper Trade

Before risking real money, paper trade (simulate) for 2-4 weeks:

- Pick a stock from your watchlist

- Select a strike 5-10% below current price, 30-45 days out

- Record the premium you would collect

- Track what happens over the trade's life

- Note whether you'd have been assigned

- Calculate your return or loss

Do this with 3-5 positions simultaneously. This gives you a feel for position management, the emotional experience of watching puts move against you, and the decisions you'll face.

Step 5: Start Small with Real Money

When you're ready for real trades, start with just 1-2 contracts using 10-20% of your total capital.

Example with $25,000 account:

- Sell 1 put requiring $10,000 cash (40% of capital)

- Keep $15,000 in reserve

- After successfully managing this for 2-3 months, scale to 2-3 positions

Don't jump in with your entire portfolio. Build confidence and skill first.

Step 6: Track Your Trades Systematically

From day one, track every trade in a journal or spreadsheet. Record:

- Stock ticker and strike price

- Expiration date

- Premium collected

- Entry date

- Whether you were assigned

- If assigned: your actual cost basis

- Exit date and final profit/loss

This data helps you identify what's working, learn from mistakes, and calculate your real returns over time.

Start your free trial of QuantWheel to automate this entire tracking process. QuantWheel syncs with your broker, automatically logs every trade, adjusts cost basis on assignments, and calculates your real performance without manual spreadsheets.

Tools and Resources for Cash Secured Put Traders

Success with cash secured puts requires the right tools for research, trade execution, and position management.

Options Screeners and Analysis Tools

You need a way to quickly scan hundreds of stocks for put-selling opportunities that meet your criteria.

What to look for in a screener:

- Filter by delta (probability of assignment)

- Filter by DTE (days to expiration)

- Filter by premium yield (return on capital)

- Sort by IV rank or percentile

- Real-time data (not delayed 15-20 minutes)

Most broker platforms (ThinkorSwim, TastyTrade, Interactive Brokers) have built-in screeners, but they're often slow and clunky. Screening 500+ tickers can take 5-10 minutes.

QuantWheel's options screener was built specifically for put sellers and wheel traders. It scans 570K+ option contracts in under 5 minutes, filtering for DTE, delta, yield, IV rank, and fundamental quality simultaneously. Instead of manually checking 30 tickers, screen the entire market and find the best opportunities in minutes.

Position Tracking and Portfolio Management

Once you have multiple positions running, tracking becomes critical. You need to know:

- Which positions are up or down

- When each position expires

- Your real cost basis on assigned stocks

- Total premium collected across all positions

- Aggregate portfolio Greeks and risk

Manual tracking in spreadsheets works for 1-2 positions but breaks down at 5-10+ positions. You'll spend 30-60 minutes per week updating your sheet, and errors creep in (especially with cost basis after assignments).

QuantWheel's Wheel Native Journal automates this completely. It syncs with your broker, tracks every put sale and assignment, automatically adjusts cost basis, and shows your complete position status in real-time. No manual spreadsheet updates required.

Educational Resources Worth Your Time

Books:

- "Trading Options Greeks" by Dan Passarelli (understand delta, theta, implied volatility)

- "The Options Playbook" by Brian Overby (free PDF, excellent beginner resource)

Communities:

- r/thetagang on Reddit (active community of put/call sellers sharing strategies)

- r/options on Reddit (broader options discussion, more technical)

Data and Research:

- CBOE (Chicago Board Options Exchange) for volatility data and options education

- Your broker's education center (most offer free options courses)

The key is consistent education combined with real trading experience. Theory without practice doesn't work. Practice without understanding theory leads to costly mistakes.

Conclusion: Is Selling Cash Secured Puts Right for You?

Let's bring this all together with an honest assessment.

Cash secured puts are a conservative income strategy that works well for investors who want to generate returns from cash while potentially acquiring quality stocks at a discount. You're essentially getting paid to set limit buy orders.

This strategy is likely a good fit if:

- You have $10,000+ in capital you can allocate to options

- You want to own quality stocks long-term, not just speculate

- You're patient and disciplined with predetermined rules

- You're comfortable with temporary unrealized losses on assigned positions

- You want to generate 12-25% annualized returns with defined risk

- You have time to monitor positions at least a few times per week

This strategy probably isn't right if:

- You have very limited capital (under $5,000)

- You don't want to own stocks, just trade options

- You need your cash liquid and available on short notice

- You panic when positions move against you

- You're hoping for explosive 100%+ returns (this isn't that)

- You don't have time to learn and manage positions properly

The honest truth: selling cash secured puts is boring. You're grinding out 1-2% returns per month on quality stocks. There are no home runs. But there's also no blown-up account if you follow proper position sizing and stock selection.

This is a consistency play. It's the tortoise strategy, not the hare. If you can sell puts monthly on good stocks for years, collecting small premiums and occasionally getting assigned on positions you want to own anyway, you'll build wealth steadily.

The key is treating it like a business, not gambling. Have a systematic process for stock selection, strike selection, position sizing, and assignment management. Track your results honestly. Adjust what doesn't work.

Cash secured puts are a powerful tool in your investing arsenal, but they're just one tool. Combine them with long-term stock ownership, portfolio diversification, and continuous learning, and you'll have a robust approach to building wealth in the markets.

If you're ready to implement this strategy systematically, consider using QuantWheel to automate the tedious tracking, cost basis calculations, and position management. It's the platform built specifically for cash secured put sellers and wheel strategy traders.

Start your free trial of QuantWheel and see how automated tracking transforms your options trading from spreadsheet chaos to systematic income generation.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.