Selecting the right strike price is the single most important decision when selling cash-secured puts in the wheel strategy. Choose too aggressively and you'll get assigned on stocks you don't want at bad prices. Choose too conservatively and you'll barely collect any premium, making the strategy not worth your time. Build a system for finding CSP opportunities inside QuantWheel →

After selling hundreds of cash-secured puts, I've learned that strike selection isn't about finding the "perfect" strike. It's about understanding the trade-offs between premium income, assignment probability, and the underlying stock quality. This guide breaks down exactly how to make that decision systematically.

TLDR: Cash Covered Put Strike Selection in 60 Seconds

The 3-Step Framework:

- Target 0.30 Delta - This gives you approximately 65-70% probability that the option expires worthless (you keep all premium without assignment). It balances income with reasonable safety.

- Verify IV Rank Above 50% - You want elevated volatility to collect better premiums, but not permanent business problems. High IV rank means premium is rich compared to historical levels.

- Calculate Premium Yield - Aim for 1-3% of the strike price per month (12-36% annualized). If premium is too low, the risk isn't worth the reward.

Simple Example:

- Stock: Trading at $100

- IV Rank: 65% (good for premium collection)

- 0.30 Delta Put: $95 strike, 35 days to expiration

- Premium Collected: $2.50 per share ($250 per contract)

- Monthly Yield: 2.5% ($2.50 / $100)

- Annualized: ~30%

If assigned at $95, your real cost basis becomes $92.50 after the $2.50 premium, giving you a 7.5% discount to the current price. That's the wheel strategy working as designed.

Understanding Strike Price Fundamentals

Before diving into selection criteria, let's clarify what a strike price actually represents in the context of cash-secured puts.

When you sell a cash-secured put, you're agreeing to buy 100 shares of stock at the strike price if the stock trades below that level at expiration. In exchange for taking on this obligation, you collect a premium upfront.

The Strike Price Triangle:

- Higher Strike = More premium + Higher assignment risk

- Lower Strike = Less premium + Lower assignment risk

- Sweet Spot = Balance between income and protection

The art of strike selection is finding that sweet spot for your risk tolerance and trading goals.

The Delta Method: Your Primary Selection Tool

Delta is the single most useful metric for strike selection. It represents the approximate probability that your put will finish in-the-money (ITM) at expiration, meaning you'll get assigned.

Delta Guidelines for Wheel Strategy

0.20 Delta (Conservative)

- ~80% probability of expiring worthless

- Strike typically 10-20% below current price

- Lower premium collection

- Best for: Stocks you're less confident about, volatile markets, preservation-focused traders

0.30 Delta (Standard - RECOMMENDED)

- ~70% probability of expiring worthless

- Strike typically 5-15% below current price

- Balanced premium collection

- Best for: Most wheel strategy traders, quality stocks, normal market conditions

0.40-0.50 Delta (Aggressive)

- ~50-60% probability of expiring worthless

- Strike typically 0-10% below current price

- Higher premium but frequent assignments

- Best for: Stocks you strongly want to own, the "aggressive wheel"

Why 0.30 Delta Works

The 0.30 delta target emerged through trial and error in the options trading community. It provides three key benefits:

- High success rate: About 7 out of 10 contracts expire worthless

- Meaningful premium: Typically 1-3% per month on quality stocks

- Acceptable assignment: When assigned, you're buying at reasonable discounts

In my experience tracking hundreds of wheel positions, 0.30 delta strikes generate the best long-term returns without excessive assignment stress.

Implied Volatility: The Premium Multiplier

Two stocks trading at the same price can offer vastly different premiums for the same delta strike. The difference? Implied volatility (IV).

IV Rank: Finding Rich Premiums

IV Rank compares current implied volatility to the past year's range:

- IV Rank = (Current IV - 52-week Low IV) / (52-week High IV - 52-week Low IV) × 100

Target IV Rank above 50% for cash-secured puts. This means volatility (and therefore premiums) are elevated compared to normal levels.

The IV Sweet Spot

Avoid Low IV (0-30% IV Rank)

- Premiums too small to justify risk

- 0.30 delta puts might only yield 0.5-1% monthly

- Better to wait for volatility expansion

Target Medium-High IV (50-80% IV Rank)

- Elevated premiums due to uncertainty

- Often catalyzed by earnings, market pullbacks, or sector rotation

- 0.30 delta puts can yield 2-4% monthly

Be Cautious with Extreme IV (90-100% IV Rank)

- Premiums look amazing but usually for good reason

- Often indicates serious business problems, not temporary volatility

- Verify the cause: earnings volatility is temporary, business deterioration is permanent

Real Example: IV Impact on Strike Selection

Stock: $100 per share

Low IV Environment (IV Rank: 25%)

- 0.30 delta put: $97 strike, 35 DTE

- Premium: $1.00 ($100 total)

- Monthly yield: 1%

High IV Environment (IV Rank: 70%)

- 0.30 delta put: $93 strike, 35 DTE

- Premium: $2.50 ($250 total)

- Monthly yield: 2.5%

Notice in the high IV scenario, the 0.30 delta strike is further out-of-the-money AND pays more premium. This is the power of volatility for premium sellers.

Premium Yield: Calculating Your Return

Delta tells you probability, but premium yield tells you if the trade is worth taking.

Monthly Yield Target

Calculate monthly yield: (Premium / Strike Price) × (30 / Days to Expiration)

Target ranges by trader type:

- Conservative: 1-2% monthly (12-24% annualized)

- Moderate: 2-3% monthly (24-36% annualized)

- Aggressive: 3-5% monthly (36-60% annualized)

Don't Just Chase Yield

High yield alone doesn't make a good trade. A 5% monthly premium on a deteriorating business isn't better than a 2% premium on a quality company.

Red flags for "too good" premiums:

- Fundamental problems (declining revenue, mounting debt, management issues)

- Regulatory concerns or legal troubles

- Sector-wide collapse in progress

- Recent bankruptcy rumors

Good reasons for elevated premiums:

- Temporary earnings uncertainty

- Market-wide volatility spike

- Sector rotation creating temporary selling pressure

- Short-term negative news with no long-term impact

The key question: "Am I comfortable owning this stock at this strike price if assigned?" If no, don't sell the put regardless of premium.

Time to Expiration: The DTE Factor

Days to expiration (DTE) affects both premium and strike selection strategy.

30-45 DTE: The Sweet Spot

Most wheel traders sell puts with 30-45 days until expiration. This timeframe offers:

- Accelerated theta decay (time value erosion)

- Sufficient premium to make trades worthwhile

- Reasonable time for adjustment if needed

- Monthly rhythm for position management

Strike Selection by DTE

Weekly Options (5-10 DTE)

- Need higher delta (0.35-0.40) to collect meaningful premium

- More frequent adjustments required

- Higher win rate but smaller premiums

- Better for active traders with time to manage

Monthly Options (30-45 DTE)

- Standard 0.30 delta works well

- Better premium/time balance

- Standard approach for most wheel traders

60+ DTE Options

- Can use lower delta (0.20-0.25) and still collect good premium

- Less frequent management

- More capital tied up longer

- Better for larger accounts

Personal Preference

I primarily use 30-45 DTE because it provides the best balance between premium collection and time commitment. The monthly cadence also makes it easier to track performance and adjust strategy as market conditions change.

Stock Quality: The Forgotten Factor

Strike selection isn't just about Greeks and premium—the underlying stock matters enormously.

The Assignment Question

Before selecting any strike, ask: "Do I want to own 100 shares of this stock at this strike price?"

If the answer is anything other than "yes" or "I'd be fine with it," - don't sell the put.

The wheel strategy assumes assignment is acceptable, not catastrophic.

Quality Criteria for Wheel Stocks

Strong fundamentals:

- Profitable or path to profitability

- Manageable debt levels

- Competitive advantages

- Competent management

Adequate liquidity:

- Average daily volume above 1 million shares

- Tight bid-ask spreads (under 5% of option price)

- Multiple market makers

Reasonable valuation:

- Not dramatically overvalued

- Not on the verge of collapse

- Trading at levels where assignment won't result in immediate 20-30% drawdown

Stable business model:

- Avoid companies facing existential threats

- Be cautious with speculative growth stocks

- Prefer established businesses with predictable cash flows

Strike Selection Framework: Putting It All Together

Here's my systematic approach to selecting cash-covered put strikes:

Step 1: Screen for Candidates

- IV Rank above 50%

- Stocks you're willing to own

- Sufficient liquidity (volume, open interest)

- Appropriate for account size

Step 2: Find the 0.30 Delta Strike

- Look at options chain

- Find the strike closest to 0.30 delta

- Check 30-45 DTE expirations

Step 3: Calculate Premium Yield

- Premium ÷ Strike Price = Yield

- Adjust for DTE if not exactly 30 days

- Verify yield meets your target (1-3% monthly)

Step 4: Assess Risk/Reward

- What's your effective cost basis if assigned? (Strike - Premium)

- Is that a price you're comfortable with?

- What's the downside if the stock continues falling?

Step 5: Check Technical Levels

- Is the strike near major support?

- Is the stock in a downtrend?

- Are there upcoming catalysts (earnings, product launches)?

Step 6: Make Final Decision

- If all factors align: Sell the put

- If hesitant about assignment: Choose lower strike (0.20 delta)

- If premium too low: Wait for better opportunity

Advanced Considerations

Adjusting for Market Conditions

Bull Market:

- Can be more aggressive (0.35-0.40 delta)

- Assignments less frequent

- Consider higher strikes for more premium

Bear Market:

- Be more conservative (0.20-0.25 delta)

- Protect against larger drawdowns

- Accept lower premiums for safety

Sideways/Choppy Market:

- Standard 0.30 delta works well

- Focus on high IV rank opportunities

- Be patient with strike selection

Earnings Considerations

Selling puts into earnings can increase premium significantly, but it also increases risk.

Before earnings:

- IV rank typically spikes

- Premiums can be 2-3x normal

- Assignment risk increases if earnings disappoint

My approach:

- Only sell through earnings on stocks I'm very confident about

- Use more conservative strikes (0.20-0.25 delta)

- Accept that assignment is likely if earnings miss

After earnings:

- IV typically collapses (IV crush)

- Premiums return to normal

- Often better entry timing for wheel strategy

Common Strike Selection Mistakes

Mistake 1: Chasing Premium

Selling the highest premium available without considering assignment risk. Yes, that 0.50 delta put pays nicely, but you'll get assigned constantly.

Fix: Stick to your delta targets. Premium will come from IV rank, not delta.

Mistake 2: Ignoring Stock Quality

Selling puts on stocks you'd never want to own just because premiums look good.

Fix: Only sell puts on stocks you've researched and are comfortable owning.

Mistake 3: Being Too Conservative

Selling 0.10 delta puts so far out-of-the-money that premiums become meaningless.

Fix: Accept reasonable risk. 0.30 delta strikes still give you 70% probability of success.

Mistake 4: Not Adjusting for IV

Using the same strike distance (like "always 10% below current price") regardless of volatility.

Fix: Use delta as your guide, not percentage distance. Delta accounts for volatility automatically.

Mistake 5: Forgetting About Catalysts

Selling puts without checking earnings dates, FDA decisions, or other binary events.

Fix: Always check the calendar. Know what events are coming that could move the stock significantly.

Strike Selection in Practice: Real Examples

Example 1: Conservative Blue Chip

Stock: Dividend-paying large cap at $150

- IV Rank: 55% (moderate elevation)

- Your target: Conservative income, okay with assignment

- 45 DTE options chain

Analysis:

- 0.30 delta put: $145 strike

- Premium: $3.00 ($300 per contract)

- Monthly yield: 2% ($3 / $150)

- Effective cost if assigned: $142 (5.3% discount to current)

Decision: Good trade. Reasonable premium, quality company, comfortable with assignment at $142.

Example 2: High IV Growth Stock

Stock: Tech company at $80

- IV Rank: 75% (highly elevated, post-earnings volatility)

- Your target: Aggressive premium collection

- 35 DTE options chain

Analysis:

- 0.30 delta put: $72 strike (10% below current!)

- Premium: $3.50 ($350 per contract)

- Monthly yield: 4.4% ($3.50 / $80)

- Effective cost if assigned: $68.50 (14% discount)

Decision: Attractive trade if you like the company fundamentals. High premium due to temporary volatility spike. The 0.30 delta strike being 10% OTM shows how much volatility expands option prices.

Example 3: Avoid This Trade

Stock: Struggling retailer at $25

- IV Rank: 95% (extremely elevated)

- Company guidance: Revenue declining, closing stores

- 40 DTE options chain

Analysis:

- 0.30 delta put: $22 strike

- Premium: $2.00 ($200 per contract)

- Monthly yield: 8% ($2 / $25) - WOW!

- Effective cost if assigned: $20

Decision: Pass. The premium looks amazing, but the IV rank of 95% signals serious problems. This isn't temporary volatility—it's potential business failure. Would you want to own this stock at $20? If not, don't sell the put.

Tools and Resources

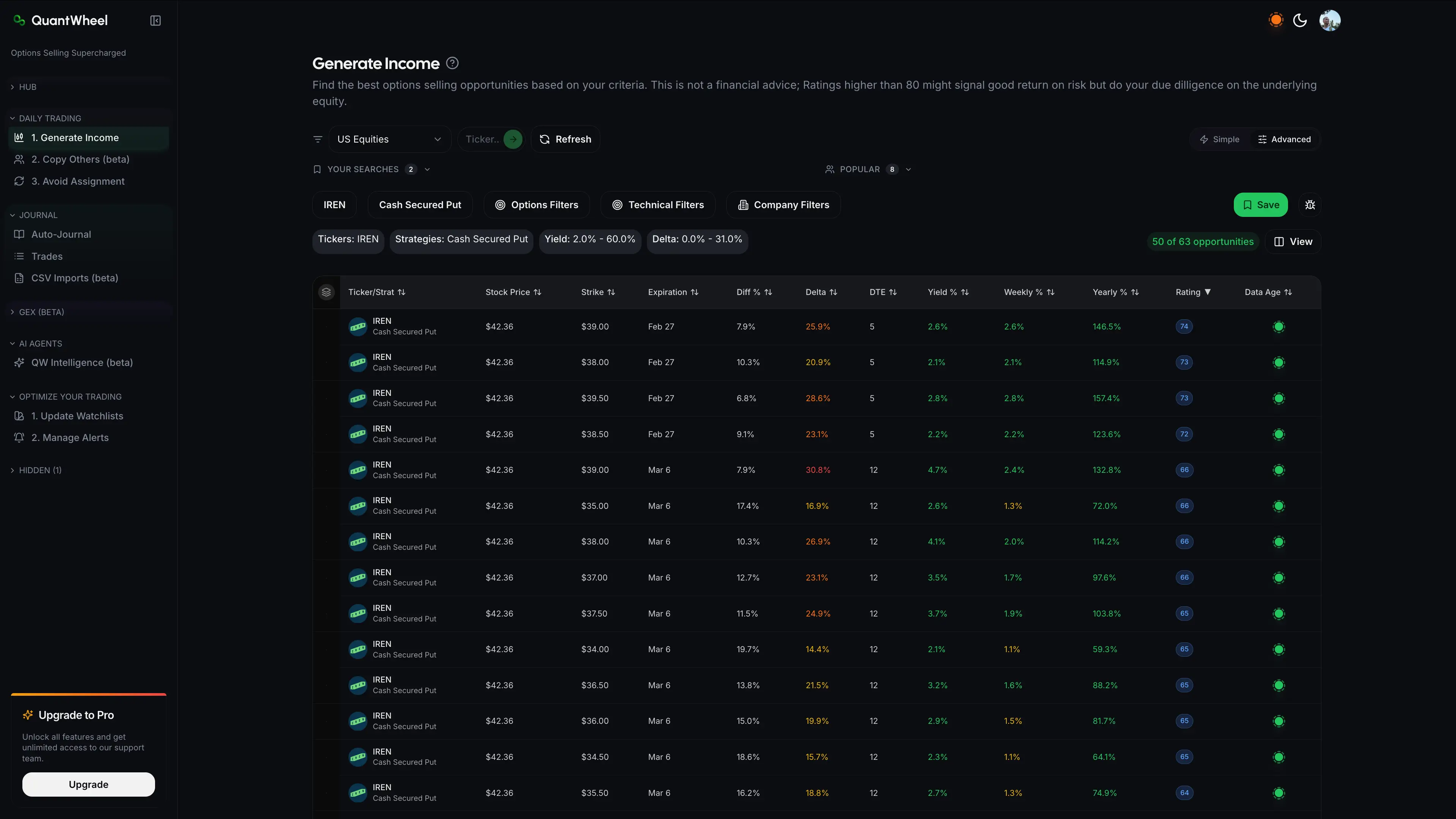

Selecting strikes efficiently requires good tools. Manually checking options chains on broker platforms is tedious when you're analyzing multiple stocks.

Here's where most traders struggle: calculating delta, IV rank, and premium yield across 20-30 potential candidates takes hours using standard broker tools. By the time you finish your analysis, market conditions have changed.

This is exactly why platforms like QuantWheel exist—built specifically for systematic options strategies. The screener analyzes 570,000+ option contracts in minutes, filtering by your exact delta targets, IV rank minimums, and yield requirements. Instead of manually checking each stock, you see ranked opportunities that meet your criteria.

When I was managing 15+ wheel positions and hunting for new opportunities, the time savings alone justified automated screening. More importantly, I stopped missing high-IV opportunities that appeared and disappeared while I was stuck in spreadsheets.

Managing Positions After Strike Selection

Strike selection is just the beginning. What happens after you sell the put?

Monitor Your Position

Track these metrics:

- P/L percentage: What's your profit relative to max profit?

- Days to expiration: How much time is left?

- Delta changes: Is your put moving closer to ITM?

- Stock price relative to strike: How much buffer do you have?

Exit Rules

Close at 50% profit if 21+ days remain. This is a common rule among experienced traders. Why? Because you've captured half the maximum profit in a fraction of the time. Closing early allows you to redeploy capital into new opportunities.

Roll when threatened if the stock is approaching your strike with time remaining. Rolling involves buying back your current put and selling a new one (typically further out in time, possibly at a different strike).

Accept assignment if the stock is below your strike at expiration. Remember, assignment was part of the plan. Your effective cost basis is Strike - Premium, not just the strike price.

Assignment Management

Here's where cost basis tracking becomes critical. Your broker shows your stock purchase price as the strike price, but your real cost basis is lower after accounting for the premium collected.

Example:

- Strike: $50

- Premium collected: $2

- Real cost basis: $48

You need to track this manually in spreadsheets—unless you're using a platform like QuantWheel that automatically adjusts your cost basis on assignment. When you eventually sell covered calls against the assigned shares, accurate cost basis determines your real breakeven and profit targets.

Conclusion: Systematic Strike Selection

Choosing cash-covered put strike prices doesn't require genius-level analysis. It requires a systematic approach:

- Start with quality stocks you're willing to own

- Target 0.30 delta for balanced risk/reward

- Focus on IV rank above 50% for better premiums

- Calculate yield and ensure 1-3% monthly

- Verify effective cost basis is acceptable if assigned

The wheel strategy works when you're disciplined about strike selection. Don't chase premium. Don't sell puts on stocks you'd hate to own. Accept that some positions will go against you—that's why we target 70% win rates, not 100%.

Most importantly, learn from each trade. Track which strikes worked and which didn't. Adjust your delta targets based on market conditions and your risk tolerance. Over time, you'll develop an intuition for good strikes versus traps.

The boring, systematic approach wins in the long run. Conservative. Consistent. Boring. Profitable.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.