Here’s the reality: cash secured puts seem simple in theory, but small mistakes compound.

After analyzing thousands of trades and talking with wheel strategy traders, I’ve identified errors that you could learn the hard way or simply avoid by reading the text below.

This article is written by the QuantWheel team. We mentioned most often repeated mistakes based on our own trading experience, what we encountered and how we solve it.

Author: David Romic

TL;DR: Cash Secured Put Mistakes You Need to Avoid

Quick Summary for Traders:

A cash secured put is when you sell a put option while holding enough cash to buy 100 shares if assigned.

The 7 deadliest mistakes are:

- Chasing premium over quality – Selling high-premium puts on stocks you’d never actually buy

- Ignoring your true cost basis – Forgetting that premium reduces your real stock cost

- Not checking earnings dates – Getting crushed by volatility you could have avoided

- Picking strikes by premium alone – Ignoring probability of assignment and support levels

- Using all your buying power – Overleveraging leaves no room for additional opportunities

- Forgetting about assignment – Not having a plan for what happens when you own the stock

- Not tracking positions properly – Losing sight of your aggregate risk across multiple puts

A good trade takes into account picking logical strike prices, keeping track of your true cost basis, trying to avoid earnings (unless experienced) and avoiding over leveraging.

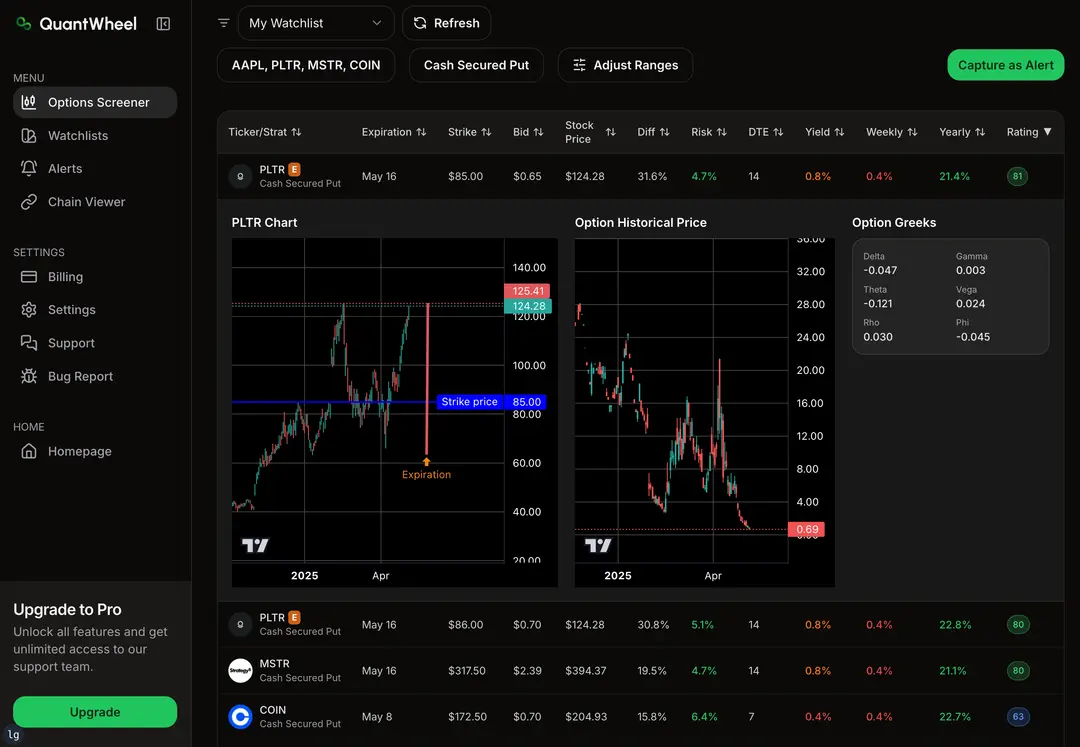

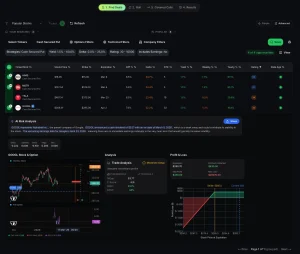

Here’s an example trade below that fits all of the above:

Why is this trade good?

- Under 20 delta = very low chance of assignment

- GEX Put Wall is at $40, our strike is even below that – $37.50. We are picking strike price at support levels and even below them = extra safety

- No earnings

- 120% IV which means more traders are trading $IREN, this means higher premium

- Getting assigned on this Cash – Secured trade would bring our cost basis even lower

- Entering with 2 contracts, which is less than 7% of portfolio avoids over leveraging (these percentages are personal preferences)

Mistake #1: Chasing Premium Without Analyzing the Underlying Stock

This is the sin that kills more option sellers than any other.

A trader sees someone on Reddit post about collecting 8% monthly premium on a “hot stock.”

They then check the option chain, see that fat premium, and sell the put without researching the company.

Two weeks later, you’re now holding a bag. But this one is heavy and it stinks.

Why This Happens

High premiums exist for a reason – the market is pricing in real risk. That juicy premium is compensation for the elevated probability that you’ll get assigned on a declining asset.

The Right Approach

Before selling any cash secured put, ask yourself:

- Would I be comfortable owning 100 shares of this stock at this price?

- Do I understand why the business makes money?

- Would I hold this stock for 6-12 months if assigned?

- Is there a fundamental reason for the high premium (upcoming earnings, sector weakness, company-specific issues)?

If you can’t answer “yes” to the first three questions, don’t sell the put – regardless of how attractive the premium looks.

Real Example

Let’s say you’re comparing two trades:

- Stock A: Solid dividend payer, $100 stock, $2 premium (2% return)

- Stock B: Speculative biotech, $50 stock, $5 premium (10% return)

The novice trader picks Stock B for the premium. The experienced trader picks Stock A because they’d actually want to own it.

In the example above, when Stock B drops to $35 post-FDA rejection, the trader is assigned at $50 (minus $5 premium = $45 cost basis) on a stock now worth $35. That’s a $10 per share loss, or -22% – far worse than the 2% they would have made on Stock A.

Here’s another example, a declining beauty stock with higher premiums versus a well established and dividend paying stock – $GOOGL.

Even if $GOOGL pays less in premiums, its a much better investment than playing with fire – $HIMS in this case.

Mistake #2: Miscalculating Cost Basis After Assignment

Here’s where most traders’ tracking breaks down completely.

Your broker shows you were assigned at $50 per share. But your actual cost basis is $48 because you collected $2 in premium when you sold the put.

This seems simple, but when you’re managing multiple positions and premiums at different times, the manual calculation becomes a nightmare.

Why Cost Basis Matters

If you don’t know your true cost basis, you can’t:

- Price covered calls correctly

- Calculate your real breakeven

- Make accurate portfolio decisions

- Report taxes correctly

The Assignment Problem

Here’s where most traders struggle: calculating your actual cost basis after assignment. Let’s say you sold a $50 put, collected $2 premium, and got assigned. Your real cost basis is $48 per share – but your broker shows $50. You need to track this manually through spreadsheets, updating formulas every time you collect more premium from covered calls.

Unless you’re using a platform like QuantWheel that automatically adjusts your cost basis when assignments happen. It tracks your full wheel cycle – from the initial put premium through assignment to covered call premium – giving you accurate breakeven calculations without manual spreadsheet updates.

The Math You Need to Track

Full wheel cycle cost basis formula:

True Cost Basis = Strike Price - Put Premium - Covered Call Premiums CollectedExample:

- Sold $100 put, collected $3 premium

- Assigned at $100 (real cost: $97)

- Sold $105 covered call, collected $2

- Called away at $105

Result: Bought at $97, sold at $105 + $2 = $107 total. Net profit: $10 per share or 10.3% return.

If you tracked cost basis as $100 (what broker shows), you’d think you only made $7 per share, a 7% return. That’s a significant tracking error that compounds across dozens of positions.

Here’s how QuantWheel automatically tracks your break even price and true cost basis so that you don’t make a mistake.

![]()

Mistake #3: Ignoring Earnings Dates and Volatility Events

Nothing ruins a cash secured put strategy faster than an earnings surprise you didn’t see coming.

Earnings announcements create volatility. That volatility creates risk. And that risk can turn your comfortable 10% OTM put into an ITM assignment overnight.

The Calendar Trap

Many traders sell puts based on expiration dates that work for them – Fridays for weekly options, end of month for monthlies. They don’t check what’s happening between now and expiration.

Then boom – the company reports earnings three days before expiration, beats revenue but misses EPS guidance, stock drops 15%, and you’re assigned on a position that was “safe” just 72 hours ago.

What Experienced Traders Do

- Check earnings calendar before selling ANY put

- Avoid expirations that include earnings unless you’re comfortable with the added risk

- If you must trade through earnings, use wider strikes or smaller position sizes

- Set alerts for company announcements, FDA decisions, or sector-specific events

Earnings Strategy Decision Tree

Option 1: Avoid Earnings Completely

- Safest approach for consistent returns

- Lower premiums but lower risk

- Best for capital preservation

Option 2: Trade Earnings Intentionally

- Higher premiums due to elevated IV

- Accept higher assignment risk

- Requires larger margin of safety in strike selection

Option 3: Close Before Earnings

- Collect partial premium

- Eliminate earnings risk

- May leave money on the table but preserves capital

There’s no “wrong” choice here, but you must make an intentional choice rather than stumbling into earnings by accident.

Mistake #4: Selecting Strikes Based Only on Premium

“I always sell the 30-delta put because that’s what everyone recommends.”

This is mechanical thinking that ignores the actual stock you’re trading.

Why Delta Isn’t Everything

Yes, a 30-delta put theoretically has about a 30% chance of finishing in-the-money. But delta is not the only consideration:

- Support levels: Is your strike below a major support level?

- Recent price action: Has the stock been trending down?

- Valuation: Is the stock overvalued at current prices?

- Your conviction: How confident are you in the company?

The Multi-Factor Strike Selection Approach

When selecting strikes for cash secured puts, evaluate:

- Technical Analysis: Support/resistance levels, moving averages

- Delta/Probability: Probability of assignment

- Premium Yield: Return if not assigned

- Your “Would Buy” Price: The price where you’d happily accumulate shares

- Risk/Reward Ratio: Potential assignment cost vs premium collected

Real Scenario

Stock: $100 per share

Option A: $95 strike, 30 delta, $2.50 premium (2.5% return)

- At support level

- You’d happily own at $92.50 net cost

Option B: $97 strike, 40 delta, $3.50 premium (3.5% return)

- Above support, in recent trading range

- Higher probability of assignment

- Net cost $93.50 – acceptable but not ideal

Option C: $90 strike, 15 delta, $1.00 premium (1% return)

- Very safe, below strong support

- Low premium doesn’t justify capital commitment

The “right” answer depends on your goals. Conservative traders pick Option A. Aggressive traders might pick Option B. Option C isn’t worth it for most wheel traders – not enough premium for the capital requirement.

Mistake #5: Using All Your Available Buying Power

Picture this: You have $50,000 in cash. You sell cash secured puts on five different stocks, using up $48,000 of your buying power. Everything’s great until you spot an amazing opportunity – a quality stock drops 15% on sector-wide weakness, offering incredible premiums.

But you can’t take advantage because you’re fully deployed.

The Overallocation Trap

Using 90-100% of your buying power creates three problems:

- No flexibility for new opportunities

- No cash to roll positions if needed

- Psychological pressure when positions move against you

The Right Allocation Strategy

Experienced wheel traders typically use:

- 60-75% deployment in normal conditions

- Reserve 25-40% for opportunities or adjustments

- Scale in gradually rather than deploying all at once

Position Sizing Framework

Account Size: $50,000

Conservative Approach:

- 5 positions × $7,000 commitment = $35,000 deployed (70%)

- $15,000 in reserve (30%)

- Can add 2 more positions or manage assignments

Aggressive Approach:

- 7 positions × $6,000 commitment = $42,000 deployed (84%)

- $8,000 in reserve (16%)

- Limited flexibility but higher premium collection

The conservative approach gives you breathing room. The aggressive approach maximizes premium but reduces your ability to adapt.

Mistake #6: Not Having an Assignment Plan

Most traders focus entirely on the put side and forget that assignment is not just possible – it’s part of the strategy.

The wheel strategy is literally named for the cycle: sell put → get assigned → sell covered call → get called away → repeat. Yet many traders panic when assignment actually happens.

The Assignment Reality Check

When you sell cash secured puts, you should want assignment at the right price. That’s the whole point. You’re setting a “buy limit order” and getting paid to wait.

What to Do When Assigned

Immediate Actions:

- Confirm your cost basis (strike – premium)

- Review the stock’s current situation

- Decide on covered call strategy

- Set alerts for the stock

Covered Call Decision Framework:

Scenario 1: Stock Above Your Cost Basis

- Sell ATM or slightly OTM covered call

- Lock in profit + additional premium

- Conservative approach

Scenario 2: Stock Below Your Cost Basis

- Sell call above your cost basis

- Collect premium while waiting for recovery

- May take multiple cycles

Scenario 3: Stock Significantly Down

- Consider selling call below cost basis if you want out

- Accept realized loss but free up capital

- Defensive position management

The Mistake: No Plan Means Panic

Traders without an assignment plan often:

- Sell calls at wrong strikes (too aggressive or too conservative)

- Panic and close positions at losses

- Hold losing positions too long without adjustment

- Don’t factor in the original put premium

Having a written plan before assignment happens removes emotion from the decision.

Mistake #7: Poor Position Tracking and Record Keeping

After your third or fourth cash secured put position, the spreadsheet tracking starts to break down.

Which position expires when? What’s your aggregate exposure? What’s your total premium collected this month? What’s your adjusted cost basis on assigned positions?

The Tracking Nightmare

Manual tracking requires:

- Updating entry dates and premiums

- Calculating cost basis adjustments

- Tracking through assignments

- Managing expiration calendars

- Calculating aggregate risk

- Maintaining tax records

After managing 20+ positions in spreadsheets, you start making errors. You forget to close at 50% profit. You miss an expiration. You miscalculate cost basis on an assigned position.

This is exactly why platforms like QuantWheel exist – built specifically for wheel traders who need systematic tracking without the manual headache. It automatically syncs with your broker, tracks full wheel cycles, adjusts cost basis on assignment, and sends alerts when positions need attention.

What You Must Track

Per Position:

- Entry date and expiration

- Strike price and premium collected

- Current P&L and breakeven

- Days to expiration

- Upcoming events (earnings, etc.)

Portfolio Level:

- Total capital deployed

- Aggregate delta exposure

- Premium collected (monthly, yearly)

- Win rate and profit factor

- Sector concentration

Through Full Cycle:

- Put premium collected

- Assignment cost basis

- Covered call premiums

- Final exit price

- Total cycle return

Without proper tracking, you can’t learn from your trades or optimize your strategy.

Bonus Mistake: Treating Cash Secured Puts as “Safe”

The final mistake is psychological: believing that cash secured puts are a safe, low-risk strategy.

They’re lower risk than naked puts because you have the cash to cover assignment. But they’re not safe. You can still lose money – potentially a lot of money if the underlying stock craters.

The Risk Reality

Maximum Loss Per Position: (Strike Price – Premium) × 100 shares

If you sell a $50 put for $2 premium and the stock goes to zero, your maximum loss is $4,800 per contract. That’s not theoretical – companies do fail, stocks do drop 80-90%.

Risk Management Essentials

- Diversification: Don’t concentrate in one sector

- Quality Over Premium: Stick to companies you trust

- Position Sizing: No single position over 10-15% of portfolio

- Stop Losses: Have rules for when to exit bad trades

- Continuous Learning: Track what works and what doesn’t

Cash secured puts can be boring and profitable (which is the goal), but only when executed with discipline and respect for the downside risk.

The Path Forward: Avoiding These Mistakes

Recognizing these mistakes is step one. Actually avoiding them requires:

1. Have a Written Trading Plan

Document your:

- Strike selection criteria

- Position sizing rules

- Assignment strategy

- Exit criteria

- Tracking methods

2. Use Proper Tools

Whether it’s QuantWheel, a detailed spreadsheet, or another platform, you need systematic tracking. Manual memory isn’t sufficient past 2-3 positions.

3. Focus on Quality Over Quantity

Better to make 5 high-quality trades than 20 mediocre ones. Quality stocks, quality strikes, quality management.

4. Review and Adjust

Monthly review process:

- What worked?

- What didn’t?

- What mistakes did I make?

- What will I change?

5. Accept That Assignment Happens

Stop treating assignment as failure. It’s part of the wheel strategy. Have a plan, execute the plan, stay systematic.

Start Tracking Your Cash Secured Puts Properly

The difference between traders who consistently profit from cash secured puts and those who give back their gains often comes down to avoiding these seven mistakes.

You don’t need to be perfect. You don’t need to catch every opportunity. You just need to be systematic, track your positions properly, and avoid the big errors that wipe out months of premium collection.

Find quality Cash – Secured puts inside QuantWheel →

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.