You own 100 shares of stock sitting in your account. You've heard covered calls can generate income, but you're not sure when to pull the trigger. Sell too early with low implied volatility, and you leave money on the table. Wait too long, and the stock might run away without you collecting any premium at all.

Start your free trial of QuantWheel to track your covered call positions automatically and receive alerts when optimal selling conditions appear.

The timing of when you sell covered calls can make the difference between consistent monthly income and frustrating losses. This guide covers the exact conditions, strike selection strategies, and timing frameworks that experienced options traders use to maximize covered call profitability.

TLDR: When to Sell Covered Calls

Sell covered calls when:

- You own 100 shares (or multiples) of stock you're willing to potentially sell

- Implied volatility is elevated (IV Rank above 50% ideally)

- 30-45 days to expiration for optimal theta decay efficiency

- At resistance levels where stock may stall or reverse

- After assignment from puts if running the wheel strategy

Simple example: You own 100 shares of AMD purchased at $140. The stock has rallied to $150, IV rank is 65%, and there's technical resistance at $155. You sell a 30-day covered call at the $155 strike (30-delta), collecting $3.50 premium ($350 total). Three outcomes: (1) Stock stays below $155, you keep shares and $350 profit, (2) Stock exceeds $155, you sell at $155 plus keep $350 = $1,850 total gain, (3) Stock drops, your cost basis improves to $146.50 thanks to premium collected.

Understanding the Covered Call Strategy Basics

A covered call means selling a call option against stock you already own. For every 100 shares you hold, you can sell one call contract. The buyer pays you a premium for the right (but not obligation) to purchase your shares at a specific price (the strike) before a certain date (expiration).

Why Covered Calls Work

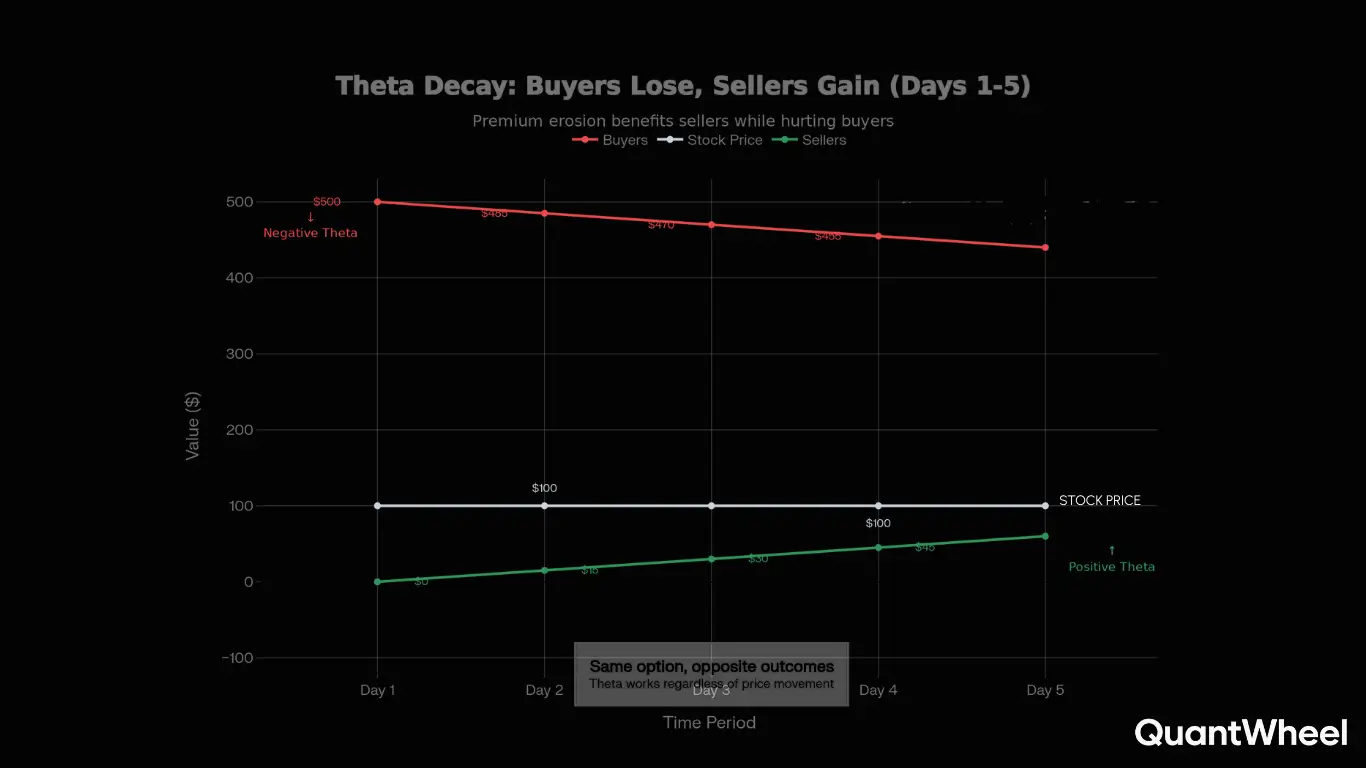

Covered calls generate income through time decay. As expiration approaches, the option's value erodes—this is called theta decay. You keep the premium whether the stock goes up slightly, stays flat, or declines moderately. The strategy works best in neutral-to-moderately-bullish markets when you don't expect explosive upside.

The key risk: you cap your upside. If you sell a covered call at $50 and the stock rockets to $70, you're obligated to sell at $50. You forfeit the gains above your strike price. This is why timing and strike selection matter enormously.

Optimal Market Conditions for Selling Covered Calls

When Implied Volatility Is Elevated

The single most important factor in covered call timing is implied volatility (IV). Higher IV means higher premiums. You want to sell when IV rank is above 50%, meaning current volatility is in the upper half of its 52-week range.

Why IV matters: A covered call on AMD might collect $2.00 in premium when IV is low (20 IV rank) versus $4.50 when IV is high (70 IV rank). That's a 125% difference in income for the exact same position and strike.

Check IV rank before selling any covered call. If IV is in the bottom quartile, consider waiting unless you have a specific tactical reason (like managing a losing position).

After Technical Rallies or at Resistance

Stock charts reveal resistance levels—price points where sellers historically emerge. These make excellent covered call strikes because the stock is more likely to stall or reverse at these levels.

If you own shares at $100 and the stock rallies to $115 approaching resistance at $120, this is an ideal time to sell the $120 call. You collect premium while the stock fights technical barriers. If it breaks through, you capture the move from $100 to $120 plus the premium. If it stalls, you keep the premium and still own the shares.

Following Assignment from Cash-Secured Puts

For wheel strategy traders, the moment you get assigned stock from a short put is an excellent time to immediately sell a covered call. You've already collected premium selling the put, and now you continue the income generation by selling a call.

Here's where most traders struggle after assignment: calculating your actual cost basis. Let's say you sold a $50 put, collected $2 premium, and got assigned 100 shares. Your broker shows a $50 cost basis, but your real basis is $48 per share after the premium collected.

This is exactly where QuantWheel's automated cost basis tracking becomes essential—it automatically adjusts your cost basis when assignments happen, showing your true breakeven and helping you select the optimal covered call strike based on your real entry price. Track trades inside QuantWheel →

Strike Selection: Choosing the Right Call to Sell

The 30-Delta Sweet Spot

Most experienced traders target the 30-delta strike for covered calls. Delta represents the probability the option finishes in-the-money. A 30-delta call has approximately 30% chance of being in-the-money at expiration (meaning 70% chance it expires worthless and you keep your shares).

Why 30-delta works:

- Balanced income vs. upside retention

- Reasonable safety margin above current price

- Decent premium collection

- Allows participation in moderate rallies

Conservative vs. Aggressive Strike Selection

Conservative approach (20-delta):

- Lower premium collected

- Higher probability of keeping shares

- Further out-of-the-money strikes

- Best when bullish on the stock

Aggressive approach (40-50 delta):

- Higher premium collected

- Greater assignment risk

- Closer to current price

- Best when neutral or ready to sell shares

Your strike selection should reflect your goal: Are you trying to squeeze maximum income from a stock you're ready to sell? Choose aggressive strikes. Do you want steady income while retaining long-term position? Choose conservative strikes.

Adjusting Strikes Based on Cost Basis

If your cost basis is well below the current price (you have significant unrealized gains), you can afford to sell closer in-the-money strikes for higher premium without worrying about assignment. The gains are already captured.

Example: You bought shares at $40, they're now $55. Selling a $52 call (slightly in-the-money) collects substantial premium. Even if assigned, you profit $12 per share plus the call premium—a strong outcome.

Conversely, if your cost basis is near or above current price, sell further out-of-the-money to avoid locking in losses through assignment.

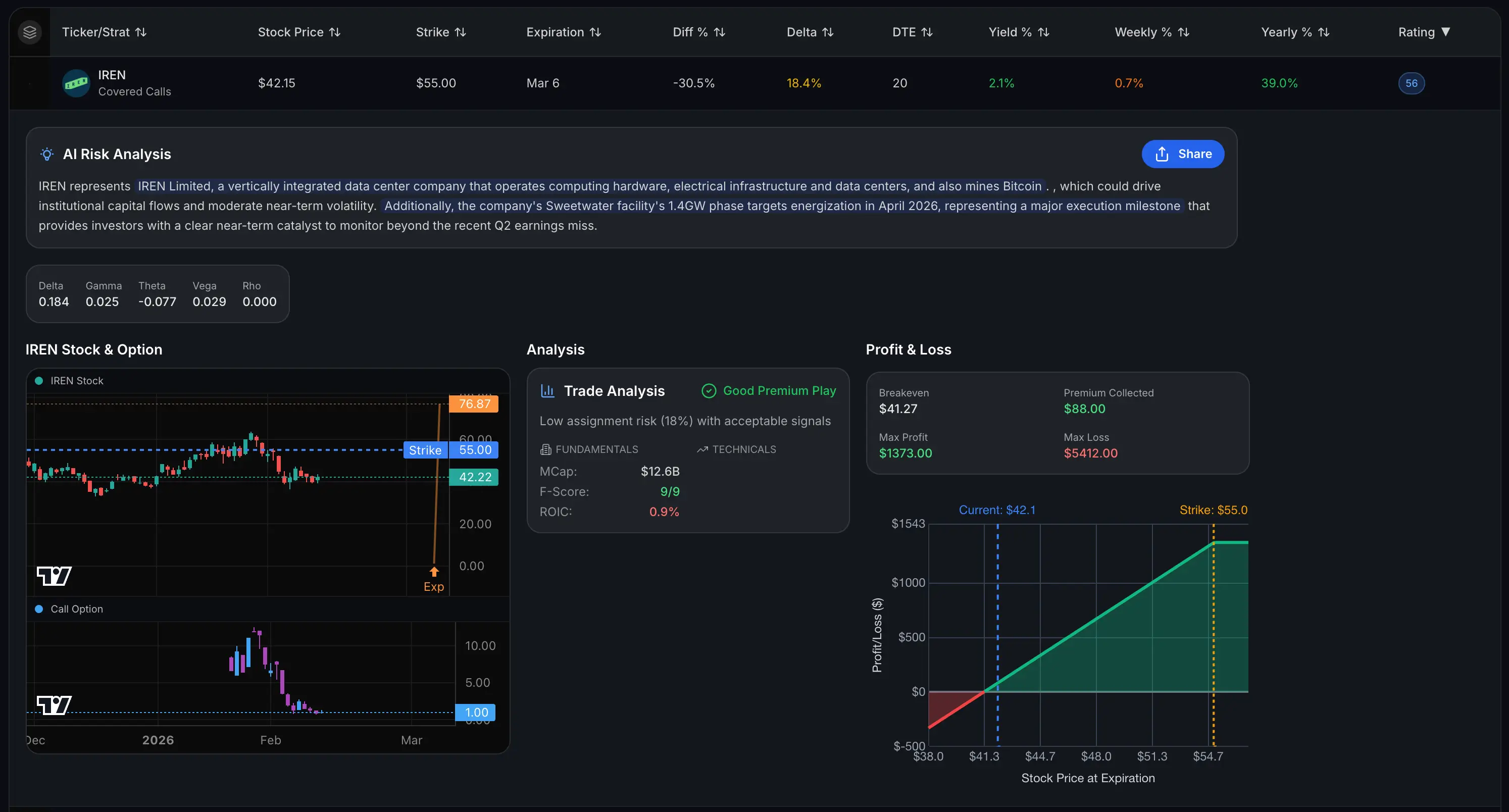

For running the wheel, traders usually go for lower chance of assignment as their goal is to stay in the stock. Here's an example of such a trade:

Find good premium trades like this inside QuantWheel →

Expiration Timing: 30-45 Days for Maximum Efficiency

Why 30-45 Days Works Best

Theta decay (time value erosion) is non-linear. Options lose value slowly with many days remaining, then accelerate as expiration approaches. The sweet spot is 30-45 days to expiration where you capture meaningful premium with reasonable time for theta to work in your favor.

Research shows options lose approximately 50% of their extrinsic value in the final 21 days. By selling at 30-45 DTE and closing at 50% profit or rolling at 21 DTE, you harvest theta efficiently while maintaining portfolio flexibility.

Weekly vs. Monthly Expirations

Weekly covered calls:

- Lower premium per contract

- More management required

- Higher annualized returns if managed actively

- Best for experienced traders

Monthly covered calls:

- Higher premium per contract

- Less management required

- Good for set-and-forget approaches

- Best for part-time traders

Many traders find 30-45 day monthly cycles strike the right balance between premium collection and time commitment.

When NOT to Sell Covered Calls

When Implied Volatility Is Crushed

If IV rank is below 30%, premiums are likely inadequate. You're locking in low prices for potentially weeks. Unless you have a defensive reason (managing a losing position), wait for IV expansion.

Before Major Catalysts (Usually)

Earnings announcements, FDA decisions, or other major catalysts spike implied volatility. Selling calls before these events captures elevated premium, but you risk assignment if the stock gaps up significantly.

Most traders close existing covered calls before earnings, wait for the volatility crush post-announcement, then evaluate whether to reopen based on the new price and IV environment.

When Highly Bullish on the Stock

If you believe the stock is about to make a significant move higher, covered calls cap your upside. It's frustrating to limit your gains for $2 premium when the stock rallies $15.

Covered calls work best in neutral-to-moderately-bullish conditions, not when you're expecting explosive growth. If you're very bullish, hold the shares uncovered or use a different strategy.

When You Can't Accept Assignment

Never sell a covered call on shares you're not willing to part with. Assignment can happen any time the call goes in-the-money, especially before ex-dividend dates. If emotional attachment or tax considerations mean you can't sell, don't write covered calls.

Managing Your Covered Calls: When to Close or Roll

Close at 50% Profit

Many traders follow the rule: close covered calls when they reach 50% profit with significant time remaining (21+ days). You've captured the majority of the theta decay, and closing frees you to sell a new call at better strikes or wait for improved conditions.

Example: You sold a call for $3.00. It's now worth $1.50 with 25 days left. Close it, book the $150 profit, and reassess whether to open a new call or wait.

Roll When Threatened by Assignment

If your stock rallies significantly above your strike and you don't want to be assigned, consider rolling: buy back the current call and sell a new call at a higher strike and/or further expiration.

Rolling criteria:

- Stock is above strike with high probability of assignment

- You can collect a net credit (or small debit) on the roll

- The new strike preserves reasonable upside potential

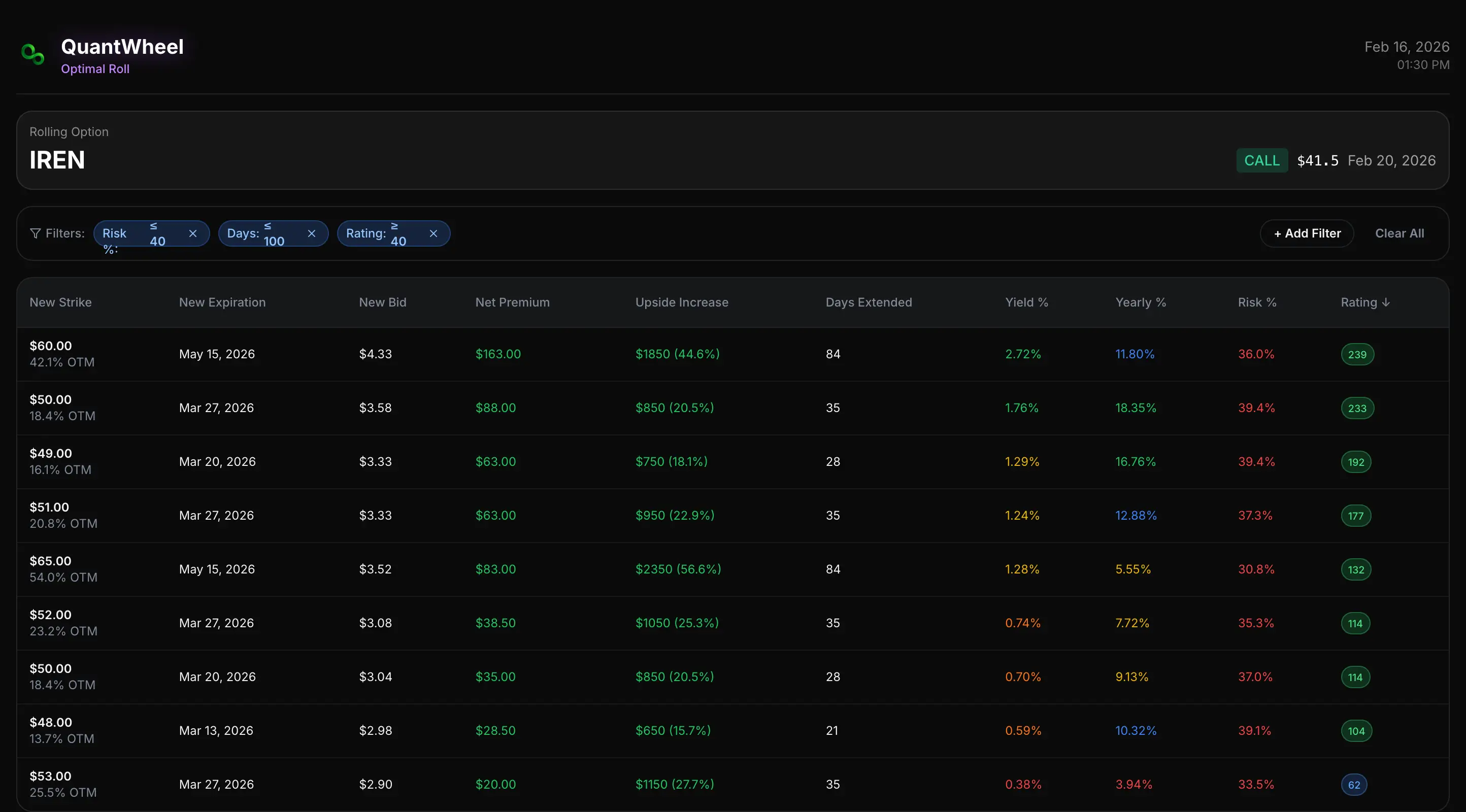

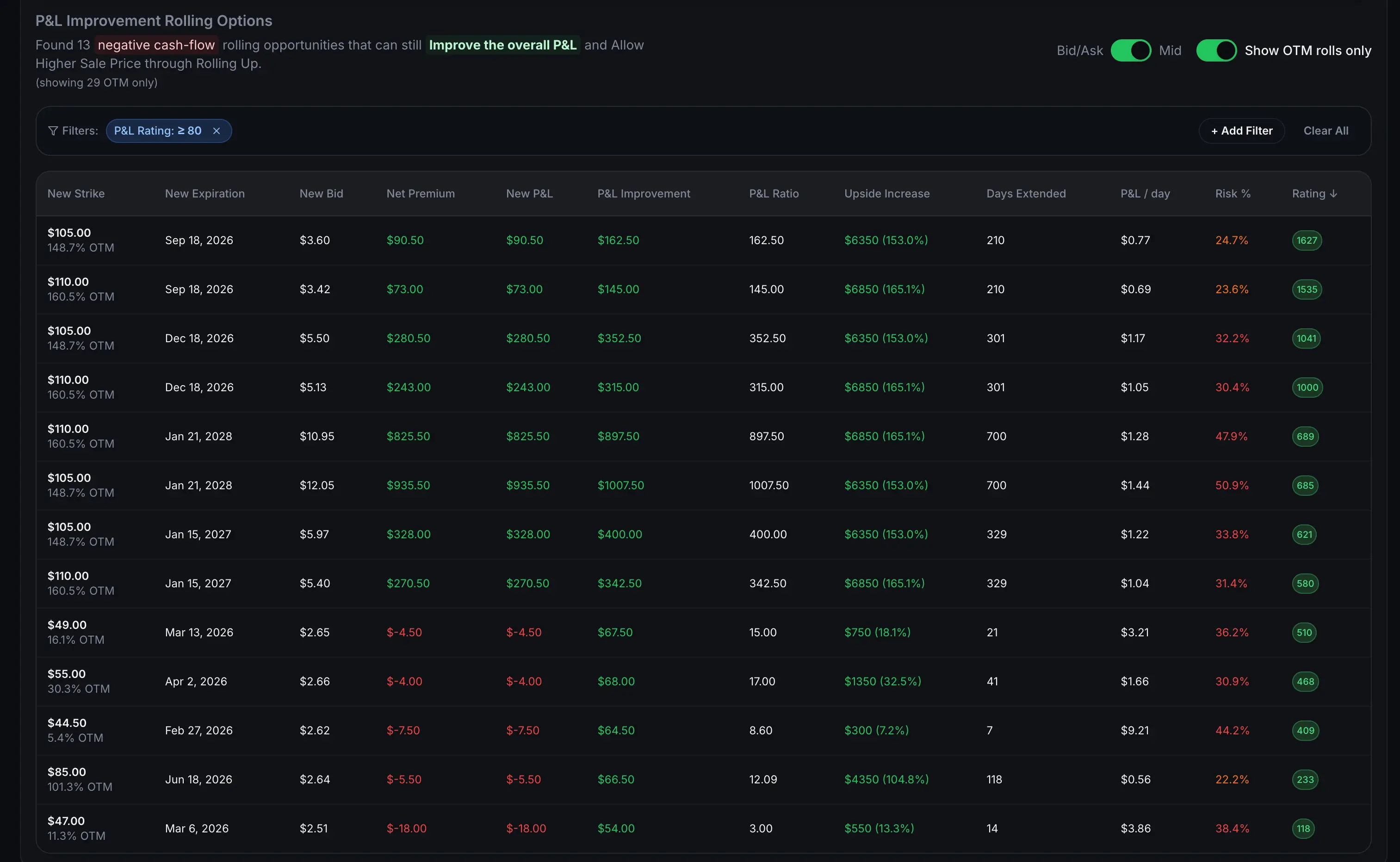

This is where QuantWheel's Roll Assistant becomes valuable—it analyzes all possible roll options, calculates the return for each combination, and recommends the optimal roll to maximize your position value while avoiding unwanted assignment. Here's a fix it recommends for rolling the $IREN trade:

Get help with rolling inside QuantWheel →

When to Take Assignment

Sometimes assignment is the right outcome. If the stock hit your target price, you captured significant appreciation plus premium, and you're ready to move capital to new opportunities, accept assignment. Close the trade, realize the gain, and search for your next wheel cycle.

Covered Calls in the Wheel Strategy

The Complete Wheel Cycle

The wheel strategy integrates covered calls as step two of a systematic process:

- Sell cash-secured put → collect premium

- Get assigned shares (or put expires worthless, repeat step 1)

- Sell covered call on assigned shares → collect more premium

- Get assigned on call (shares sold) OR call expires, repeat step 3

Covered calls in the wheel serve a specific purpose: continuing income generation on stock acquired through assignment while working toward selling the shares at your target price.

Timing Covered Calls After Put Assignment

After getting assigned from a short put, immediately evaluate whether to sell a covered call:

Sell a call if:

- IV remains elevated

- Stock has bounced from assignment price

- You're comfortable with potential assignment at higher strikes

- Your cost basis (including put premium) provides good profit margin

Wait to sell a call if:

- IV has crushed significantly

- Stock is still declining

- You expect a short-term rally that would improve call premiums

The key is not forcing the trade. Just because you got assigned doesn't mean you must immediately sell a call. Wait for favorable conditions.

Here's a good covered call trade example:

Real-World Example: Timing a Covered Call

Let's walk through a complete example with real numbers.

Setup:

- You sold a $100 cash-secured put on XYZ stock

- Collected $2.50 premium ($250)

- Got assigned 100 shares at $100

- Real cost basis: $97.50 (after premium)

Current situation:

- XYZ trades at $105 (5% gain from assignment)

- IV rank: 62% (elevated)

- 35 days until next monthly expiration

- Technical resistance at $110

Decision: Sell the $110 covered call (32-delta)

- Premium collected: $3.80 ($380)

- New breakeven: $93.70 ($97.50 - $3.80)

- Max profit if assigned: $16.30 per share ($1,630 total)

Outcomes:

- Stock stays below $110: Call expires worthless. You keep 100 shares with $93.70 cost basis and $630 total premium collected ($250 put + $380 call). Sell another call next cycle.

- Stock assigned at $110: You sell shares at $110, original cost was $100 (broker), you collected $630 total premium. Total profit: $1,630 on $10,000 position = 16.3% return in approximately 60-70 days.

- Stock drops to $95: The $380 call premium cushions the decline. Your adjusted basis is $93.70, so you're only down $1.30 per share vs. $5 without the call. Continue selling calls to work back to breakeven.

This example shows why timing matters. You waited for IV elevation, sold near resistance, captured good premium, and structured the trade to profit in two of three scenarios.

Tools and Tracking for Covered Call Success

Why Manual Tracking Breaks Down

After managing 10+ covered call positions across multiple stocks, spreadsheets become unmanageable. You need to track:

- Current positions and strikes

- Expiration dates

- Premium collected per position

- Adjusted cost basis (especially after assignments)

- P&L calculations

- Roll opportunities

- When to close at 50% profit

Missing even one of these details leads to suboptimal decisions or forgotten positions.

This is exactly why QuantWheel was built specifically for premium sellers running covered calls and the wheel strategy. The platform automatically:

- Syncs with your broker to track all covered calls in real-time

- Adjusts cost basis when you get assigned from puts

- Alerts you when positions hit 50% profit

- Shows roll opportunities with calculated returns for each option

- Tracks total premium collected across all positions

When you're managing a portfolio of covered calls, automation eliminates the tedious tracking and helps you focus on timing and strike selection—the decisions that actually impact returns.

Start your free trial of QuantWheel to see how automated position tracking and cost basis management can simplify your covered call strategy.

Key Takeaways: When to Sell Covered Calls

Optimal timing combines multiple factors:

✓ Own 100 shares of stock you're comfortable selling ✓ Implied volatility rank above 50% for maximum premium ✓ 30-45 days to expiration for theta efficiency ✓ Stock near technical resistance or after rallies ✓ Immediately after put assignment (if conditions favorable) ✓ 30-delta strike for balanced income and upside ✓ Close at 50% profit with 21+ days remaining ✓ Roll to avoid unwanted assignment

Remember: Covered calls are income enhancement, not hedges. They work best on quality stocks you're willing to hold long-term, in neutral-to-moderately-bullish conditions, when implied volatility provides adequate premium. Timing your entries and exits around these conditions separates consistent income generation from frustrating capital loss.

The key is patience. Don't force covered calls when conditions are poor. Wait for elevated IV, favorable technicals, and appropriate strikes that match your goals. Quality setups generate reliable income. Poor setups cap your upside for inadequate compensation.

Start your free trial of QuantWheel to automate covered call tracking, receive alerts when optimal selling conditions appear, and manage your positions with the only platform built specifically for wheel strategy and covered call traders.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.