You keep the premium regardless of what happens, but risk having shares called away if the stock rises above the strike. This is perfect for neutral-to-bullish stocks you already own and don't mind selling at a target price.

Many beginners think covered calls are "free money" on stocks they hold—but they're really about trading upside for immediate income. You own shares, sell a call option giving someone else the right to buy them at a set price, and pocket the premium either way. This guide walks through exactly when it boosts returns versus when it caps your profits.

So if you own at least 100 shares of a stock and it's been sitting in your portfolio for months, you could generate extra income from those shares while you hold them.

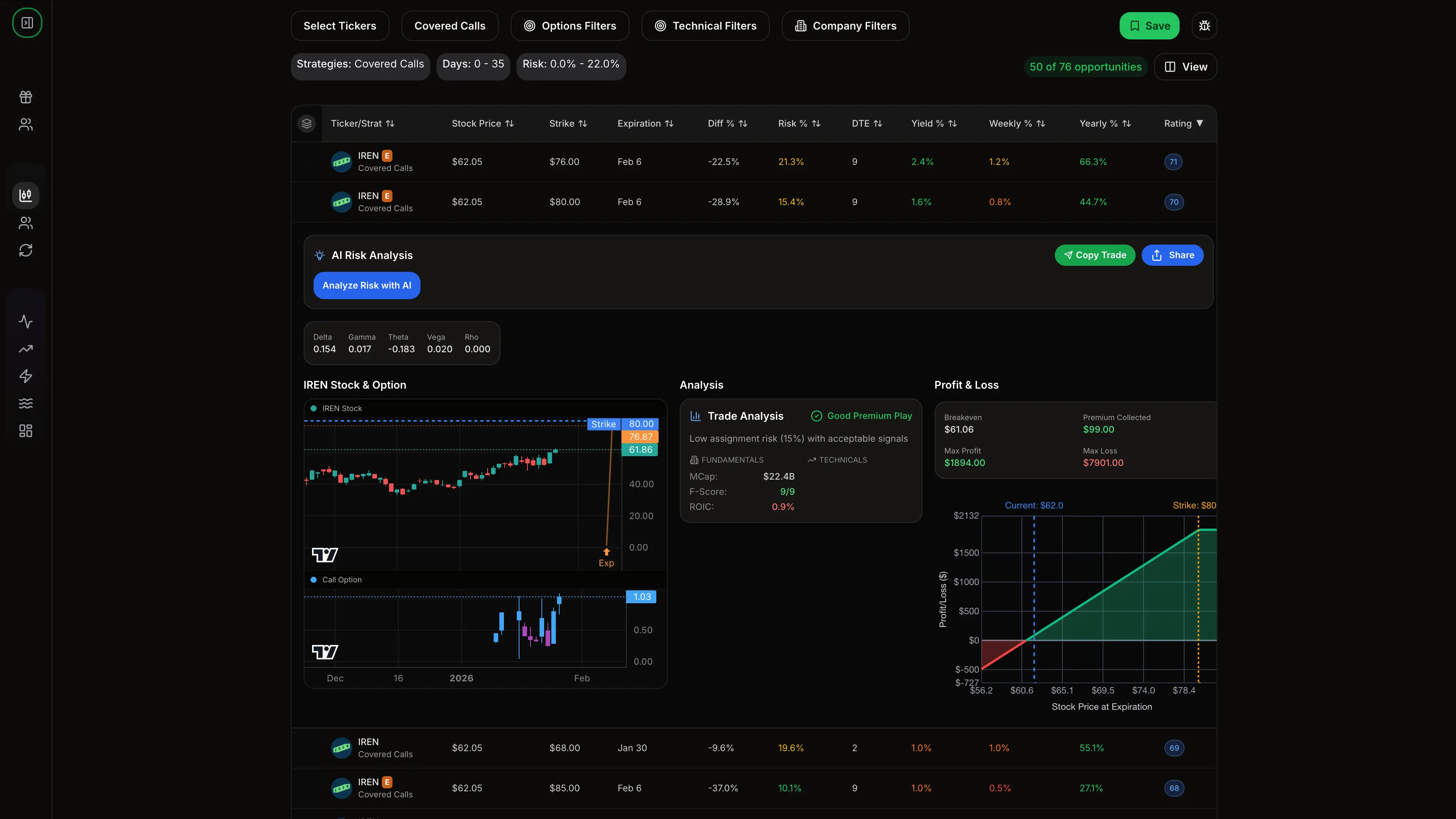

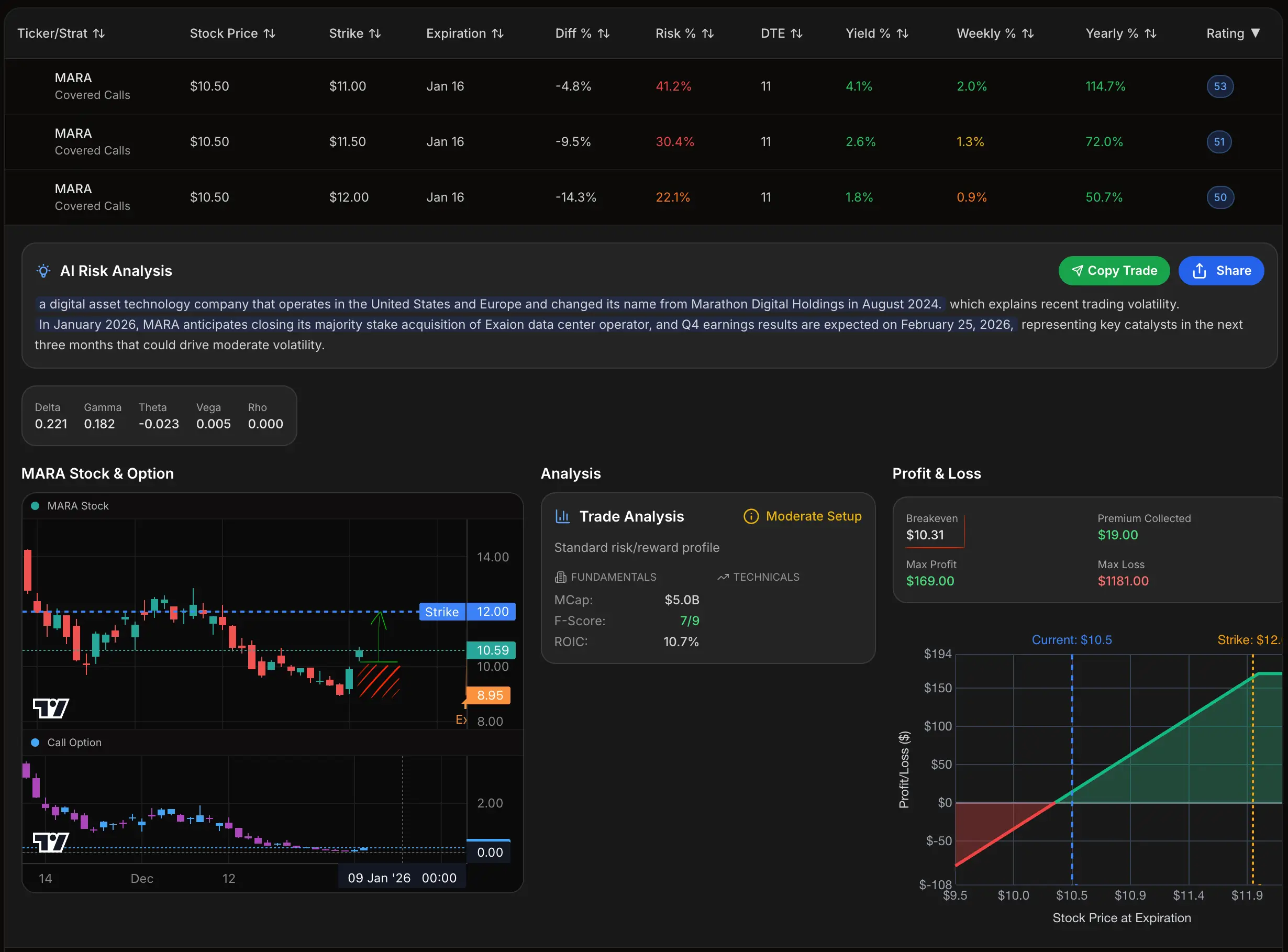

To make a process of finding better covered call opportunities less time consuming, you can start your free trial of QuantWheel..

TLDR: What Are Covered Calls?

Covered calls are an income-generating options strategy where you sell call options on stocks you already own. You receive immediate cash (premium) in exchange for giving someone else the right to buy your shares at a predetermined price (strike price) before a specific date (expiration).

Here's how it works in simple terms:

You own 100 shares of ABC stock trading at $50. You sell a covered call with a $55 strike price expiring in 30 days and collect $200 in premium. Three outcomes are possible:

- Stock stays below $55: The call expires worthless, you keep your $200 premium AND your 100 shares. You can sell another call immediately.

- Stock goes to $55-57: The call expires worthless or gets assigned. Either way, you made money from both the stock appreciation ($5/share = $500) plus the $200 premium = $700 total.

- Stock rockets to $70: Your shares get called away at $55. You made $500 on the stock (bought at $50, sold at $55) plus $200 premium = $700 total. However, you missed out on the $15/share extra gain ($1,500 opportunity cost).

The trade-off: You generate consistent income (premium) but cap your upside potential. If the stock explodes higher, you miss those gains because you're obligated to sell at the strike price.

Why it's called "covered": You own the underlying shares, so you're "covered" if the option gets exercised. This makes it much safer than selling "naked" calls where you don't own the stock.

Understanding Covered Calls: The Basics

What Is a Covered Call?

A covered call is an options strategy that combines two positions:

- Long stock position: You own 100 shares of the underlying stock

- Short call option: You sell one call option contract on those same shares

By selling the call option, you collect premium (cash) upfront. In exchange, you give the buyer the right—but not the obligation—to purchase your 100 shares at the strike price before the expiration date.

The "covered" part is crucial. You own the actual shares, so if the option buyer exercises their right to buy, you simply hand over shares you already own. This is completely different from a "naked call" where you sell a call without owning the stock—a much riskier strategy that can lead to unlimited losses.

Here's a visual example of a real trade:

The Mechanics: How Covered Calls Work

Let's break down exactly what happens when you sell a covered call.

Before you start, you need:

- At least 100 shares of the underlying stock (or multiples of 100)

- A brokerage account with options approval

- Understanding of your cost basis and target exit price

When you sell the call:

- You receive premium immediately (cash deposited in your account)

- The premium is yours to keep regardless of what happens

- You create an obligation to sell your shares at the strike if assigned

Three possible outcomes at expiration:

- Stock below strike (Out-of-the-Money): The call expires worthless. You keep your premium and shares. You can sell another call on the same shares—this is called "rolling" or simply selling a new call.

- Stock near strike (At-the-Money): The call might get exercised or expire worthless. If exercised, you sell your shares at the strike price and keep the premium. Your total profit is: (strike price - original cost) + premium collected.

- Stock above strike (In-the-Money): The call will almost certainly be exercised. Your shares get "called away" at the strike price. You keep the premium but miss out on any gains above the strike.

If you understand how buying calls works, here's how selling calls compares next to it.

Real-World Covered Call Example

Let's use actual numbers to see how this works:

Your position:

- You own 100 shares of Microsoft (MSFT)

- Your cost basis: $400 per share

- Current stock price: $420 per share

- Current unrealized gain: $2,000 ($20 × 100 shares)

You sell a covered call:

- Strike price: $440 (about 5% above current price)

- Expiration: 45 days out

- Premium collected: $600 ($6.00 per share × 100)

Scenario 1: MSFT stays at $420 (below strike)

- Call expires worthless ✓

- You keep: $600 premium

- You still own: 100 shares at $420

- Total value: $42,000 + $600 = $42,600

- Return: 1.43% in 45 days (11.6% annualized)

You can immediately sell another call on the same shares.

Scenario 2: MSFT rises to $435 (still below strike)

- Call expires worthless ✓

- You keep: $600 premium

- Stock appreciation: $1,500 ($15 × 100 shares)

- Total gain: $2,100 in 45 days

- Return: 5% in 45 days (40.5% annualized)

Scenario 3: MSFT rises to $460 (above strike)

- Call gets exercised ✗

- You must sell at $440: $44,000

- Premium kept: $600

- Total proceeds: $44,600

- Total profit from original $400 cost: $4,600 (11.5% gain)

- Opportunity cost: You missed $2,000 in gains above $440

Scenario 4: MSFT drops to $400 (below your cost)

- Call expires worthless ✓

- You keep: $600 premium

- Stock loss: -$2,000

- Net loss: -$1,400

- Without the call: Would have lost $2,000

The premium provided $600 of downside protection.

Why Investors Sell Covered Calls

Income Generation on Existing Holdings

The primary reason investors sell covered calls is simple: generate additional income from stocks they already own.

If you're holding shares long-term, they might just sit in your account going up and down. By selling calls against them, you create a regular income stream. Many investors treat this as a "dividend enhancement strategy"—they collect actual dividends from the stock PLUS premium from covered calls.

The math can be compelling. If you can collect 2-3% per month in premium (not uncommon on volatile stocks), that's 24-36% annualized income on top of any stock appreciation or dividends. Even conservative 1% monthly premiums add up to 12% annual income.

This is where QuantWheel shines, it's a income generation finding machine. It helps you find trades and also decide what's a better deal. You save time and the headache.

Lower Your Cost Basis

Every time you collect premium, you effectively lower your cost basis in the stock.

If you bought shares at $50 and collect $2 in premium, your new effective cost basis is $48. Collect another $2 next month, and it's $46. Over time, this can significantly reduce your downside risk.

Some investors use this strategy specifically to lower the cost basis on positions that went against them. If you bought a stock at $60 and it's now at $50, selling calls might not generate huge premiums (since the stock isn't moving much), but each dollar collected brings your breakeven point closer.

Here's where tracking becomes critical: your broker still shows your original cost basis, but your real economic basis includes all the premium collected. This is exactly why platforms like QuantWheel exist—to automatically track your true cost basis as you sell calls, get assigned, and continue through complete wheel cycles.

Defined Exit Strategy

Some investors use covered calls as a disciplined way to take profits at predetermined prices.

Let's say you bought a stock at $40, it's now at $50, and you'd be happy to sell at $55. Instead of just setting a limit order to sell at $55, you can sell a $55 call and collect premium. If the stock hits $55, you sell your shares AND keep the premium. If it doesn't, you keep your shares and the premium, then can sell another call.

This turns "selling for profits" into an income-generating activity rather than just an exit event.

Lower Volatility, Lower Risk

Selling covered calls mathematically reduces your position's volatility. You're exchanging unlimited upside for certain premium, which smooths out your returns.

Research shows that covered call strategies tend to have lower standard deviation of returns compared to simply owning stocks. You won't see the massive gains when stocks rally 50%, but you also collect income during the boring flat periods when stock ownership generates no returns.

For risk-averse investors or those nearing retirement, this volatility reduction can be valuable even if it means capping upside.

The Risks of Covered Calls You Need to Know

Let's be honest: covered calls aren't risk-free. Here are the real risks you need to understand before you start selling calls.

Capped Upside Potential

The biggest "risk" isn't losing money—it's missing out on big gains.

If you sell a $55 call on a stock trading at $50, and that stock rallies to $80, you only make money up to $55 plus the premium. You watch the stock soar 60% but your gain is capped at 10% plus premium (maybe 15% total). This hurts psychologically even though you made money.

This is especially painful during bull markets or on growth stocks that can double quickly. Covered calls work best on stocks you believe will rise modestly or trade sideways, not on stocks you expect to explode higher.

Management tip: If the stock rallies significantly and your call goes deep in-the-money, you can "roll" the call—buy it back and sell a new one at a higher strike and/or later date. This lets you stay in the position and collect more premium, though it costs money to close the original call.

Stock Can Still Drop

Selling a covered call doesn't protect you from the stock declining. The premium you collected provides only limited downside protection.

If you collect $2 per share in premium and the stock drops $10, you're still down $8 per share. The call expires worthless (which is good), but you still lost money on the stock.

Covered calls are NOT a hedge. They provide a small cushion, but if you're bearish on a stock, selling it is better than selling a covered call on it.

Assignment Risk (For Dividend Stocks)

If you own dividend-paying stocks and sell in-the-money covered calls, you might get assigned early—especially right before the ex-dividend date.

Here's why: If the call buyer can exercise early, buy your shares, and collect the dividend, they might do it if the dividend is larger than the remaining time value in the option.

What happens: You sell your shares before the ex-dividend date and miss the dividend. You still keep the premium, but you lose the dividend you were expecting.

Solution: Be extra careful selling calls right before ex-dividend dates, especially on high-yield stocks. Either sell out-of-the-money calls with plenty of cushion, or avoid selling calls entirely in the week before ex-dividend.

Opportunity Cost During Bull Markets

Covered calls can underperform in strong bull markets when stocks consistently rise.

If the market rallies 30% in a year and your covered call stocks get called away repeatedly at smaller gains, you might have been better off just holding. You're constantly being forced to sell your winning positions.

Behavioral finance studies show this is frustrating for investors. You're "right" about the stock going up, but you don't get to fully participate.

Strategy adjustment: During obvious bull markets, you might sell calls further out-of-the-money (lower premium, but more participation in upside) or sell calls on only a portion of your holdings.

Tax Implications

Covered calls can create tax complications:

Short-term gains: If you get assigned on a call, you're selling your shares. If you've held them less than a year, it's a short-term capital gain taxed at ordinary income rates (up to 37%).

Wash sales: If you sell shares via assignment at a loss, then buy them back within 30 days, the loss is disallowed for tax purposes due to wash sale rules.

Qualified dividends: Holding periods for qualified dividend treatment can be affected by options activity in complex ways.

This is another area where professional tracking helps. QuantWheel automatically logs all your covered call activity with dates, making tax time much simpler. You'll have a complete record of premiums collected, assignment dates, and holding periods.

Strike Selection: Choosing the Right Strike Price

The strike price you choose determines your risk/reward profile. Here's how to think about it.

Out-of-the-Money (OTM) Strikes

Strike above current stock price

Example: Stock at $50, you sell $55 call

Pros:

- Lower assignment risk (call might expire worthless)

- Keep your shares more often

- Participate in stock appreciation up to strike

- Better for bullish outlook

Cons:

- Lower premium collected

- Lower yield

- Might miss out if stock rallies past strike

Best for: Investors who want to keep their shares and are willing to accept lower income in exchange for upside participation.

Typical premium: 0.5-2% of stock price for strikes 5-10% OTM

At-the-Money (ATM) Strikes

Strike at or very near current stock price

Example: Stock at $50, you sell $50 or $51 call

Pros:

- Higher premium than OTM

- Balanced risk/reward

- Decent probability of expiring worthless

- Good yield

Cons:

- Higher assignment risk

- Little room for stock appreciation

- Can be frustrating if stock just hovers at strike

Best for: Neutral outlook on the stock. You're fine selling if it rises slightly, fine keeping it if it stays flat.

Typical premium: 2-4% of stock price

In-the-Money (ITM) Strikes

Strike below current stock price

Example: Stock at $50, you sell $45 call

Pros:

- Maximum premium collection

- Highest income generation

- Already profitable on the stock

Cons:

- Very high assignment risk (likely to be exercised)

- Essentially locking in sale of shares

- Miss any further appreciation

Best for: When you want to sell shares anyway. This is like setting a limit order to sell, but you get paid extra premium for using an option instead.

Typical premium: 5-10% or more of stock price

Delta as Your Guide

Options traders use "delta" to estimate assignment probability:

- 0.10-0.20 delta (far OTM): ~10-20% chance of being ITM at expiration, lower premium

- 0.30-0.40 delta (OTM): ~30-40% chance, moderate premium—sweet spot for many traders

- 0.50 delta (ATM): ~50% chance, higher premium

- 0.70-0.80+ delta (ITM): ~70-80%+ chance, very high premium but almost certain assignment

Many covered call sellers target the 0.30-0.40 delta range as a balance between income and keeping shares.

Time to Expiration: Weekly vs Monthly Covered Calls

How far out should you sell your calls? This is a crucial decision that affects your returns and management workload.

Weekly Covered Calls (7-14 DTE)

Days to expiration: 0-14 days

Pros:

- Fastest theta decay (time decay accelerates near expiration)

- Can collect premium 52 times per year vs 12

- More flexibility to adjust based on market conditions

- Lower absolute premium but higher annualized returns

Cons:

- More active management required

- More transaction costs (commissions add up)

- Higher probability of assignment on each trade

- Can be time-consuming

Best for: Active traders who can monitor positions daily and are comfortable with frequent rolling or adjustments.

Typical strategy: Sell calls every Friday (or Monday) at 7-14 days out, targeting 0.5-1% premium per week (26-52% annualized).

Monthly Covered Calls (30-45 DTE)

Days to expiration: 30-45 days

Pros:

- Less management required (12 trades per year)

- Lower transaction costs

- More time for stock to recover if it dips

- More premium per trade

Cons:

- Slower theta decay initially

- Locked into position longer

- Less flexibility to adapt to news

- Capital tied up longer

Best for: Investors who want income with minimal time commitment. Set it and forget it (mostly).

Typical strategy: Sell calls 30-45 days out, target 2-4% premium per month (24-48% annualized).

The Sweet Spot: 21-30 Days

Many experienced covered call sellers target 21-30 days to expiration as the optimal balance:

- Theta decay starts accelerating

- Enough time for stock to move in your favor

- Not too much time that you're locked in forever

- Premium/time ratio is attractive

- Can manage ~17 trades per year (manageable workload)

Research-backed insight: Studies show the 21-45 day window tends to produce the best risk-adjusted returns for covered call strategies. You're in the "sweet spot" where theta decay accelerates but you still have enough time cushion.

Managing Your Covered Calls: What to Do When...

When the Call Is Profitable (Stock Dropped or Stayed Flat)

Situation: You sold a $55 call, stock is at $50, call is worth $0.50 (you sold it for $2.00).

Options:

- Let it expire worthless: Collect full premium, sell new call

- Buy it back early (at $0.50): Lock in profit, free up shares, sell new call immediately at better strikes

- Roll to next month: Buy back at $0.50, sell next month's $55 call for $2.00, collect net $1.50 more

When to close early: If you can capture 50-80% of the premium with 21+ days left, many traders close early and sell a new call. This lets you collect premium twice in the original timeframe.

Example: You sold a 45-day call for $2.00. After 15 days, it's worth $0.40 (80% profit). Close it for $0.40, sell a new 30-day call for $1.80. You just collected $3.40 total vs $2.00 if you waited.

When the Stock Rallied (Call Is ITM)

Situation: You sold a $55 call, stock rallied to $60, call is now worth $6.00 (you sold it for $2.00).

Options:

- Do nothing: Let shares get called away at $55, keep $2.00 premium, realize gains

- Roll up and out: Buy back the $55 call (pay $6.00), sell a $65 call further out (collect $4.00), pay net $2.00 to stay in position

- Buy back and hold: Pay $6.00 to close, keep shares with no obligation

When to roll: If you're bullish and want to stay in the position, rolling "up and out" (higher strike, later date) lets you keep participating. You pay a debit to roll, but collect more premium and stay invested.

When to let it go: If the stock ran to your target price and you're fine exiting, just let assignment happen. You made money, mission accomplished.

When the Stock Dropped (Stock Below Strike but Down Overall)

Situation: You sold a $55 call at $50 stock price, stock dropped to $45, call is worth $0.20.

Options:

- Let it expire: Collect full premium, cushioned $2.00 of the $5.00 loss

- Roll down: Buy back at $0.20, sell $45 call for $1.80, collect more premium at lower strike

- Close and wait: Buy back at $0.20, don't sell new call, wait for stock to recover

The covered call hasn't saved you: The premium cushioned the fall, but you're still down on the stock. This is why covered calls aren't hedges.

Decision framework: If you still believe in the stock long-term, keep selling calls to lower your cost basis. If you've lost conviction, consider exiting the position entirely.

Covered Calls and the Wheel Strategy

Covered calls are the second step in the wheel strategy—one of the most popular mechanical approaches to options trading.

How Covered Calls Fit Into the Wheel

The Wheel Strategy has three parts:

- Sell cash-secured puts: Generate premium while waiting to buy stocks you like at lower prices

- Get assigned: Buy 100 shares when put gets exercised

- Sell covered calls: Generate premium on the shares you now own

Then repeat: Once shares get called away (covered call exercised), go back to step 1.

The covered call is how you "exit" the wheel cycle while collecting additional premium. You've already collected premium from the put, bought shares at a discount (strike minus put premium), now you collect more premium selling calls until assigned.

Cost Basis Tracking in the Wheel

Here's where tracking becomes essential—and where most traders using spreadsheets struggle.

Example wheel cycle:

- Sell $50 put, collect $2 premium → Real cost basis if assigned: $48

- Get assigned, buy shares at $50 → Your basis: $48 (not the $50 your broker shows)

- Sell $55 covered call, collect $2 premium → New basis: $46

- Sell another $55 call, collect $2 premium → New basis: $44

- Get assigned, sell shares at $55 → Your profit: $55 - $44 = $11/share

Your broker shows you bought at $50 and sold at $55 ($5 profit). But your REAL profit is $11/share because you collected $6 in total premiums.

This is why professional wheel traders use dedicated tracking tools. QuantWheel automatically adjusts your cost basis every time you collect premium or get assigned, showing your true breakeven and profit on every position. No manual spreadsheet updates, no forgetting to add in premiums—it's all tracked automatically.

Premium Stacking Strategy

In the wheel, you're stacking premiums at every step:

- Premium from cash-secured put

- Premium from first covered call

- Premium from second covered call

- Premium from third covered call

- (etc.)

Over a complete cycle, you might collect 15-25% total premium on the stock price. This is why wheel strategy traders can be profitable even if the stock goes nowhere—you're generating income through the entire cycle.

Tools and Platforms for Selling Covered Calls

What You Need to Track

To successfully manage covered calls, you need to track:

- Open positions: Which calls are active, strikes, expirations

- Premium collected: Total income per position and across portfolio

- Cost basis: Original cost plus all premiums collected

- Days to expiration: When positions need management

- P&L: Real profit/loss including all premiums and stock gains

The Spreadsheet Approach

Many beginners start with Excel or Google Sheets:

Pros:

- Free

- Customizable

- You control the data

Cons:

- Manual entry (tedious and error-prone)

- No real-time data

- Hard to scale past 5-10 positions

- Formulas break

- Cost basis tracking becomes nightmare

If you're managing 1-2 covered call positions casually, a spreadsheet can work. Past that, it becomes a headache.

Broker Platforms

Your broker (TD Ameritrade, Schwab, Interactive Brokers, etc.) provides position tracking:

Pros:

- Automatic trade import

- Real-time data

- Built into your trading workflow

Cons:

- Not designed for wheel strategy specifically

- Cost basis doesn't include premiums collected

- No aggregate wheel cycle tracking

- Limited analytics

- Can't see "true" breakeven including all premiums

Broker platforms show you positions but don't tell the complete story for covered call or wheel traders.

Professional Wheel Strategy Platforms

Platforms built specifically for wheel strategy and covered calls (like QuantWheel) solve the tracking problems:

What they do:

- Automatic position tracking from broker

- Cost basis adjustments for all premiums collected

- Real breakeven calculations

- Roll suggestions and analysis

- Portfolio-level analytics

- Complete wheel cycle tracking

When it's worth it: If you're managing 5+ covered call positions, getting assigned regularly, or running the wheel strategy, professional tracking pays for itself in time saved and accuracy.

After managing 15+ wheel positions, your spreadsheet becomes chaotic. Which calls are open? What's your adjusted cost basis? What's your total premium collected? This is exactly why QuantWheel exists—built specifically for wheel traders who need to track this without losing their minds.

Getting Started: Your First Covered Call

Ready to sell your first covered call? Here's the step-by-step process.

Step 1: Choose Your Stock

Criteria for good covered call stocks:

- You already own 100+ shares (or can afford to buy them)

- Stock you're neutral to slightly bullish on

- Moderate volatility (higher volatility = higher premiums)

- Liquid options market (tight bid/ask spreads)

- Avoid right before earnings or major news

Good starter stocks:

- SPY (S&P 500 ETF): Liquid, moderate volatility

- AAPL, MSFT: Blue chips with active options

- High-dividend stocks you hold long-term

Step 2: Check Your Broker Permissions

You need "Level 1" or "Covered Call" options approval:

- Most brokers approve this easily

- Required: Basic options knowledge

- Required: Account agreement signed

- May need: Minimum account balance ($2,000+)

If you don't have approval, apply through your broker's options application (usually takes 1-2 days).

Step 3: Choose Your Strike and Expiration

Use these guidelines for your first trade:

Conservative first trade:

- Strike: 5-10% out-of-the-money (delta 0.20-0.30)

- Expiration: 30-45 days out

- Target premium: 1-3% of stock value

Example: Own stock at $50, sell $55 call 45 days out for $1.50 (3% yield in 45 days).

Step 4: Enter the Trade

In your broker platform:

- Navigate to options chain for your stock

- Select expiration date

- Choose strike price

- Click "Sell to Open" for the call

- Enter quantity (1 contract = 100 shares)

- Choose order type (limit order recommended)

- Review and submit

Order type tip: Use a limit order at or slightly above the current "bid" price. You'll likely get filled at or near your limit, and you avoid selling for less than the market price.

Step 5: Track and Manage

What to monitor:

- Stock price relative to strike

- Days to expiration

- Option value (can you close early for profit?)

- News or events that might affect the stock

Set alerts:

- When option is 80% profitable (consider closing early)

- 7 days before expiration (decision time)

- If stock rallies close to strike (consider rolling)

Step 6: At Expiration

Three outcomes:

If stock below strike: Call expires worthless, you keep premium and shares. Celebrate and sell another call on Monday.

If stock near strike: Might get assigned or not. If assigned, shares disappear and cash appears (strike price × 100). If not, expires worthless.

If stock above strike: Shares get called away. Check your account Monday morning—shares gone, cash deposited. Mission accomplished.

Advanced Covered Call Strategies

Once you're comfortable with basic covered calls, these advanced techniques can boost returns.

Rolling Covered Calls

Rolling means buying back your existing call and simultaneously selling a new call—usually at a higher strike and/or later date.

When to roll:

- Stock rallied, your call is ITM, but you want to stay in position

- Collect additional premium by extending time

- Adjust strike up to participate in more upside

Example roll:

- Current: Short $50 call (stock at $55, call worth $6)

- Action: Buy to close $50 call for $6, sell to open $60 call 30 days out for $3

- Net cost: $3 debit to roll

- Result: Strike now $60 instead of $50, collected $3 more, 30 more days

Rolling for a credit vs debit:

- Credit roll: You receive net premium (yay!)

- Debit roll: You pay net cost (acceptable if you believe in stock)

Selling Calls on Dividend Stocks

Covered calls on dividend payers can enhance total yield:

Strategy:

- Own high-quality dividend stocks (3-5% yield)

- Sell conservative OTM calls for 1-2% monthly premium

- Total yield: Dividend (4%) + premiums (12%) = 16% annually

Watch out for early assignment before ex-dividend date. If your call is ITM near the ex-date, the buyer might exercise early to capture the dividend.

Management: Don't sell calls in the week before ex-dividend, or only sell far OTM strikes.

The Covered Call Ladder

Instead of selling one call at one strike, sell multiple calls at different strikes:

Example on 300 shares:

- Sell 1 contract at $55 strike (33% of position)

- Sell 1 contract at $60 strike (33% of position)

- Sell 1 contract at $65 strike (33% of position)

Benefit: You participate in upside at multiple levels while collecting premium on all contracts. If stock goes to $70, you sell 100 shares at each strike level, creating a graduated exit.

Complexity: More contracts to manage, but smoother overall returns.

Poor Man's Covered Call (PMCC)

For expensive stocks, you can approximate a covered call without buying 100 shares:

How it works:

- Instead of buying 100 shares, buy a deep ITM long call (LEAPS) with 1+ year to expiration

- Sell shorter-term OTM calls against the long call

- Much lower capital required

Example:

- Instead of buying 100 shares of TSLA at $250 ($25,000 required)

- Buy 1 TSLA $150 call expiring in 1 year ($10,000 cost)

- Sell monthly $270 calls against it for $500/month

Risks: If stock rallies hard, your long call might not increase as fast as the short call (negative gamma). More complex and riskier than true covered calls.

Common Covered Call Mistakes to Avoid

Mistake 1: Selling Calls on Stocks You Don't Want to Sell

If you're in love with a stock and can't stand the idea of selling it, don't sell calls on it—especially tight strikes.

Why it's bad: You'll be miserable if assigned. You'll likely buy back the call at a loss to keep the shares, negating your premium.

Better approach: Only sell calls on stocks you'd be genuinely fine selling at the strike price.

Mistake 2: Selling Calls Right Before Earnings

Earnings reports cause huge volatility. Stocks can gap up or down 10-20% overnight.

The problem:

- If stock gaps up, you cap your gains at a lower strike (frustrating)

- If stock gaps down, the premium doesn't protect enough (losing money)

Better approach: Close calls before earnings if you don't want the uncertainty, or specifically sell calls expiring AFTER earnings for higher premium (you're getting paid for the risk).

Mistake 3: Not Closing Profitable Calls Early

Many beginners wait for expiration even when they could close early and redeploy capital.

Example: Sold call for $2.00, it's now worth $0.30 with 28 days left (85% profit).

If you wait: Collect remaining $0.30 over 28 days If you close: Pay $0.30 now, sell new call for $1.80, collect $1.50 extra over those 28 days

Rule of thumb: If you captured 50-80% of max profit with 21+ days left, close and sell a new call.

Mistake 4: Selling Calls Too Far OTM

Selling 20-30% OTM strikes feels "safe" but generates almost no income.

Example: Stock at $50, sell $65 call for $0.20 premium (0.4% return).

Is 0.4% really worth the complexity and risk? You're better off just holding the stock.

Better approach: Target 1-4% premium returns. If you can't get that with comfortable strikes, don't force the trade.

Mistake 5: Not Tracking Cost Basis Properly

Your broker shows your original purchase price—but that's not your real basis if you've been collecting premiums.

Real scenario: Bought stock at $50, sold 6 covered calls over a year collecting $10 total. Your real basis is $40, but broker shows $50. If you sell at $48, broker says you lost money. Reality: You made $8/share.

This becomes incredibly complex when you're running wheel strategies with assignments. Cost basis tracking breaks down fast in spreadsheets, leading to tax errors and poor decisions.

Solution: Use professional tracking tools that adjust cost basis automatically for every premium collected and assignment. QuantWheel handles this automatically so you always know your true breakeven and profit.

Conclusion: Is Selling Covered Calls Right for You?

Covered calls are one of the most accessible options strategies for stock investors. They generate income, reduce volatility, and help you exit positions at target prices—all while keeping risk relatively low.

You're a good candidate for covered calls if:

- You own or can buy 100+ shares of quality stocks

- You're neutral to slightly bullish on those stocks

- You'd be fine selling at higher prices

- You want to generate extra income from holdings

- You can accept capped upside in exchange for premium

Covered calls might NOT be for you if:

- You're strongly bullish and want unlimited upside

- You're emotionally attached to specific stocks

- You don't have time to monitor and manage positions

- You're bearish (sell the stock instead)

- Your stocks don't have liquid options markets

The key is managing expectations. Covered calls won't make you rich overnight, but they can meaningfully enhance returns over time—especially when combined with the wheel strategy. Think of them as a tool in your toolbox, not a magic solution.

Start small: Sell your first call on 100 shares you already own. See how it feels. Watch what happens at expiration. Learn by doing.

And if you find yourself managing multiple covered call positions, getting assigned regularly, or running complete wheel cycles, consider using a professional tracking platform. Keeping everything straight in spreadsheets gets old fast.

Start your free trial of QuantWheel to automatically track your covered calls, manage cost basis through assignments, and see your true returns without spreadsheet chaos.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.