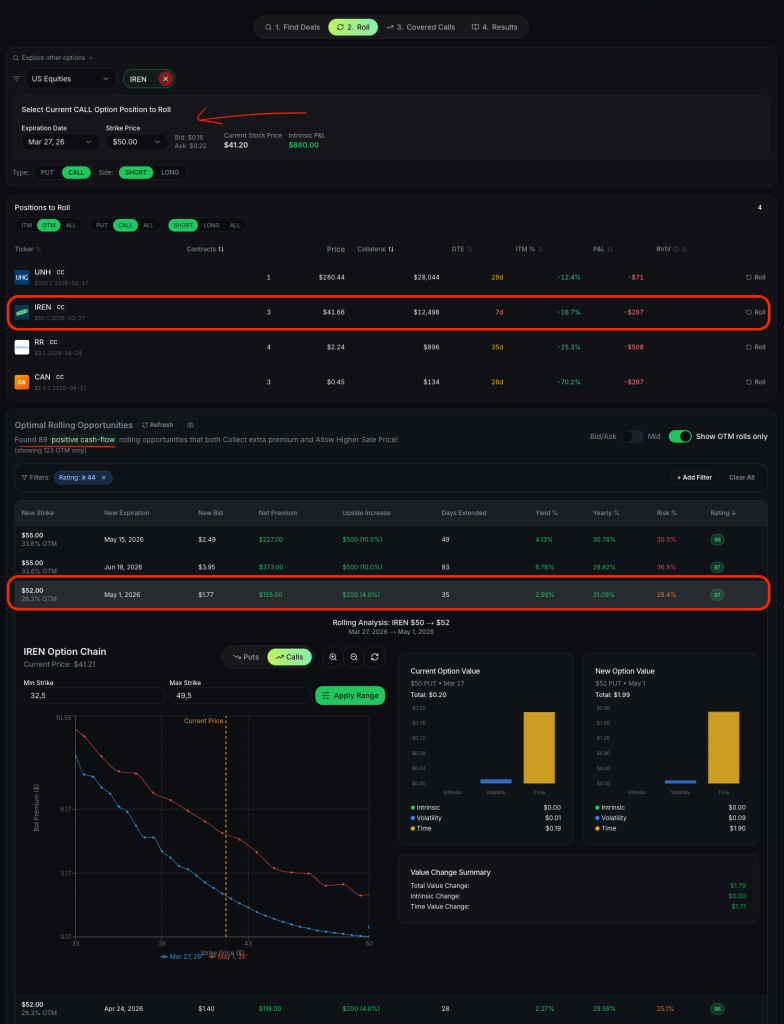

How to Roll Covered Calls for a Net Credit: A Real-World IREN Example

So, how do you turn an underperforming covered call into fresh income while simultaneously raising your profit ceiling?

Answer: Rolling options for a net credit

Take a look at this real-world example with Iris Energy (IREN).

Strike price: $50

Current stock price: $41.20

Days remaining in trade: 7 days

If you hold a $50 covered call expiring on March 27 that has lost most of its premium, you don’t have to wait for expiration to take action.

By buying back that near-term call and selling a new call (in this example $52 strike call expiring on May 1), you can instantly collect a $155 net premium per contract.

Not only does this maneuver put cash directly into your account right now, but it also increases your maximum upside potential by $200 if the stock rallies, all while extending your trade by 35 days.

Now, that’s a great example of a well timed and reasonable credit roll.

Find rolls like this for your own stocks →

Rolling Options for Credit: What You Need to Know Before Reading Further

Rolling options for credit is when you close your current short option and open a new one at a later expiration or different strike price, and you collect more money for the new option than you pay to close the old one. The difference is your net credit, and it makes your overall trade better.

Here is a simple example a 14-year-old could follow:

Imagine you agreed to buy a stock at $50 for a $2 payment (you sold a put). Now the stock dropped to $48 and your agreement is being tested. Instead of buying the stock right now, you pay $4 to cancel that agreement and immediately create a new agreement to buy at $50 next month, collecting $5. You just earned a $1 net credit ($5 received minus $4 paid). Your total collected is now $3 ($2 original plus $1 from the roll), so you really do not lose money unless the stock drops below $47. You gave yourself more time and improved your breakeven price, all without putting up extra money.

Key takeaways from this article:

- Rolling for credit means closing the old option and opening a new one while collecting net premium

- Only roll when you can collect a net credit. Never roll for a debit.

- Rolling does not fix a fundamentally broken trade. It gives you time and improves your math.

- Track every roll carefully because each credit changes your effective cost basis

- The best time to roll is when your option still has extrinsic value and the next expiration offers enough premium

- Automated tools like QuantWheel’s Roll Assistant can analyze every possible roll in seconds, saving you from analysis paralysis

What Is Rolling Options and Why Does It Matter for Premium Sellers

Rolling options is the process of closing an existing options position and simultaneously opening a new one. The new position typically has a different expiration date, a different strike price, or both. When the transaction results in a net credit to your account, you have rolled for credit.

For traders running the wheel strategy, selling cash-secured puts, or writing covered calls, rolling is not an optional skill. It is a core part of the job. The wheel strategy in particular generates situations where rolling is the most practical response to a position that has moved against you. Rather than taking assignment on a stock that has dropped below your strike, you roll the put to the next month and collect additional premium, lowering your effective purchase price if assignment eventually happens.

Rolling matters because it directly impacts three things that premium sellers care about most. First, it affects your breakeven price. Every credit you collect through a roll makes your position better on paper. Second, it affects your time in the trade. Rolling extends your exposure, which can be both a benefit (more time for the stock to recover) and a risk (longer exposure to adverse moves). Third, it affects your opportunity cost. Capital tied up in a rolled position cannot be deployed elsewhere.

Understanding when rolling makes sense and when it is better to close the trade entirely is what separates systematic premium sellers from traders who just keep rolling and hoping.

How Rolling Options for Credit Works: Step-by-Step Mechanics

The mechanics of rolling for credit are straightforward once you break them down into individual steps.

Step 1: Identify the position to roll. Look at your current short options. The candidates for rolling are positions that are being tested (the stock is near or past your strike price) but still have enough market dynamics to generate a credit on the roll.

Step 2: Close the existing position. Buy back your current short option. This costs money because you are buying something that has increased in value since you sold it (the stock moved against you). The cost to close is your buy-to-close price.

Step 3: Open a new position. Simultaneously sell a new option at the same or different strike and a later expiration date. The premium you receive for this new option is your sell-to-open price.

Step 4: Calculate the net credit or debit. Subtract the buy-to-close cost from the sell-to-open premium. If the result is positive, you rolled for a credit. If negative, you rolled for a debit. The goal is always a net credit.

Here is a concrete example with real numbers. Suppose you sold a cash-secured put on Stock XYZ at a $100 strike with 30 days to expiration and collected $3.00 in premium. The stock has dropped to $98, and your put is now worth $4.50 with 7 days left. You decide to roll.

You buy back the $100 put for $4.50 (cost) and simultaneously sell a new $100 put expiring in 37 days for $5.50 (credit). Your net credit on the roll is $5.50 minus $4.50, which equals $1.00. Your total premium collected on this trade is now $3.00 (original) plus $1.00 (roll credit) equals $4.00.

Your new breakeven price is $100 minus $4.00, which equals $96. Before the roll, your breakeven was $97. You improved your position by $1.00 while giving yourself 37 more days for the stock to recover above your strike.

Most brokers allow you to execute both legs as a single order (a roll order), which reduces execution risk compared to closing and opening separately.

Rolling Options for Credit vs. Rolling for a Debit: Why It Matters

This is the single most important rule in rolling: only roll for a credit.

When you roll for a credit, the math works in your favor. The additional premium you collect improves your breakeven and does not increase your maximum risk (assuming you keep the same strike or roll to a lower strike for puts). You are being compensated for extending the trade.

When you roll for a debit, the math works against you. You are paying money to keep a losing trade alive. Your maximum risk increases by the debit amount, and your breakeven gets worse, not better. Rolling for a debit is the options equivalent of throwing good money after bad.

There are traders who argue that rolling for a small debit can be acceptable in certain situations, such as when rolling to a significantly better strike. And yes, there are edge cases where the total expected value of the rolled position justifies a debit. But for most premium sellers, especially those running the wheel strategy, the credit-only rule is a discipline that prevents the kind of spiraling losses that destroy accounts.

If you cannot roll for a credit, that is the market telling you something. It is telling you that the position has moved far enough against you that there is not enough time value available to offset the intrinsic value you need to buy back. At that point, your options are to take the loss, accept assignment (if selling puts), or wait for a better rolling opportunity in the final days before expiration when time decay accelerates.

When to Roll Options: The Decision Framework

Knowing the mechanics is one thing. Knowing when to roll is what actually makes money. Here is a practical decision framework that many systematic premium sellers use.

Roll when all three of these conditions are true:

- The position is being tested but not catastrophically underwater. If your short put strike is $100 and the stock is at $97, that is a candidate for rolling. If the stock is at $80, rolling is likely futile because you will not find enough credit to make it worthwhile.

- There is still extrinsic value in your current option. Extrinsic value is your friend when rolling because it means you are not paying full intrinsic to close. The more extrinsic value remaining, the cheaper it is to buy back relative to the new premium you can collect.

- The next expiration cycle offers enough premium to generate a net credit. Check the option chain for the next monthly or weekly expiration. If the premium available at your strike (or a nearby strike) is higher than the cost to close your current position, you have a viable roll.

Do not roll when:

- The stock has experienced a fundamental breakdown (earnings disaster, sector collapse, regulatory action). Rolling a position on a stock in freefall just extends your pain. Sometimes taking the loss or accepting assignment is the right call.

- You have rolled the same position more than 2-3 times already. Each subsequent roll typically generates less credit than the previous one, and you are tying up capital that could be working harder elsewhere. There is a point of diminishing returns.

- The opportunity cost is too high. If you have better trades available and the capital locked in this rolled position could earn more elsewhere, closing the trade and redeploying is often the smarter move.

- Rolling would require you to extend the trade past an earnings date or other known catalyst. Earnings create massive volatility events that can overwhelm any rolling adjustment. Most experienced wheel traders prefer to close positions before earnings rather than roll through them.

Types of Rolls: Rolling Out, Rolling Down, and Rolling Down and Out

Not all rolls are created equal. The three main variations each serve different purposes.

Rolling Out (Same Strike, Later Expiration)

This is the most common type of roll. You keep the same strike price and move to a later expiration date. The credit comes from the additional time value in the new option.

When to use it: When you believe the stock will recover to your strike price given more time, and the current strike is still acceptable for assignment if it comes to that.

Example: You sold a $50 put expiring this Friday. You roll to the $50 put expiring in 4 weeks. Same strike, more time, net credit collected.

Rolling Down (Lower Strike, Same Expiration)

You move to a lower strike price at the same expiration. For puts, this means a lower purchase obligation. The credit here comes from the spread between the old and new option prices, though rolling down at the same expiration often results in a debit because you are giving up intrinsic value.

When to use it: Rarely done at the same expiration because it usually costs money. More often combined with rolling out (see below).

Rolling Down and Out (Lower Strike, Later Expiration)

This combines both adjustments: lower strike and later expiration. It is the most powerful roll for put sellers because you improve your strike price (lower risk) while extending the duration (more time to be right). The later expiration provides the time value needed to generate a credit despite the better strike.

When to use it: When you want to reduce your assignment risk and are willing to extend the trade. This is the go-to adjustment for wheel traders who want to avoid assignment on a stock that has pulled back.

Example: You sold a $50 put expiring this Friday. The stock is at $47. You roll to a $48 put expiring in 5 weeks and collect a $0.30 net credit. You now have a lower obligation ($48 vs $50), more time, and additional premium collected.

For covered call writers, the equivalent adjustments are rolling up (higher strike), rolling out (later expiration), and rolling up and out (higher strike and later expiration).

Rolling Short Puts for Credit in the Wheel Strategy

The wheel strategy generates more rolling opportunities than almost any other options approach because the strategy explicitly embraces assignment as part of the process. When you sell cash-secured puts as the first leg of the wheel, you need a plan for what happens when the stock approaches your strike.

Rolling short puts for credit is the primary defensive adjustment for wheel traders. Rather than accepting assignment immediately, many traders prefer to roll their puts to collect additional premium and lower their effective purchase price. The logic is sound: if you are willing to own the stock at a certain price, you should be even happier to own it at a lower effective price after collecting more premium through rolls.

Here is how a typical rolling sequence looks for a wheel trader:

Month 1: Sell $50 put, collect $2.00 premium. Breakeven: $48.00.

Month 2: Stock drops to $48. Put is challenged. Roll to next month $50 put for $1.00 net credit. Total premium: $3.00. New breakeven: $47.00.

Month 3: Stock is at $49. Roll again to next month $50 put for $0.75 net credit. Total premium: $3.75. New breakeven: $46.25.

Month 4: Stock recovers to $52. Put expires worthless. Total profit: $3.75 per share ($375 per contract) over 4 months. Never got assigned, never bought the stock, just collected premium.

Alternatively, if the stock had continued lower, at some point the available credit for rolling shrinks and you accept assignment. But your effective purchase price is now $46.25 instead of $48.00, which is a much better starting point for the covered call phase of the wheel.

This is where tracking becomes critical. After 2-3 rolls, keeping track of your actual cost basis, total premium collected, and effective breakeven manually is a headache. Here is where most traders struggle: calculating your actual cost basis after multiple rolls. Your broker shows the strike price as your cost, but your real cost is the strike minus all premiums collected across every roll. You need to track this manually, adjustment by adjustment. Unless you use a platform like QuantWheel that tracks full wheel cycles automatically, including every roll credit, and adjusts your cost basis in real time. It is one less spreadsheet to maintain.

Rolling Covered Calls for Credit: The Other Side of the Wheel

If rolling puts is the defensive adjustment for the first leg of the wheel, rolling covered calls is the defensive adjustment for the second leg. After you get assigned on a put and own the stock, you sell covered calls to generate premium income while waiting for the stock to recover.

Sometimes the stock rallies faster than expected and your covered call is tested. You face a choice: let the stock get called away (possibly below your cost basis) or roll the call to a higher strike or later expiration while collecting a net credit.

Rolling covered calls for credit follows the same principles as rolling puts, but in reverse. You buy back your short call and sell a new call at a higher strike or later expiration.

Example: You own Stock XYZ at an effective cost of $46.25 (after put premium from previous rolls). You sell a $48 covered call for $1.50 and the stock rallies to $49 with a week left. Your call is in the money. You can let the stock get called away at $48 for a profit of $48 minus $46.25 plus $1.50 call premium equals $3.25 per share. Or you can roll up and out.

You buy back the $48 call for $2.00 and sell a $50 call expiring next month for $2.50, collecting a $0.50 net credit. Now your call strike is $50 (higher potential exit price), you have another month of exposure, and you collected an additional $0.50 in premium. If the stock is above $50 at the new expiration, your profit is $50 minus $46.25 plus $1.50 plus $0.50 equals $5.75 per share instead of $3.25. That is 77% more profit from a single roll adjustment.

The decision to roll a covered call depends on whether you want to keep the stock. If you are happy to sell at the current strike and redeploy capital, let it get called away. If you believe the stock has more upside and you want to capture it, roll up and out for a credit.

Rolling Credit Spreads: A Different Challenge

Rolling is not limited to single-leg options. Credit spread traders (selling vertical spreads like bull put spreads or bear call spreads) also use rolling, though the mechanics are slightly more complex because you are managing two legs instead of one.

When rolling a credit spread, you close the entire spread (buy back the short leg, sell back the long leg) and open a new spread at a later expiration. The key challenge is that spreads have defined risk, so the credit available for rolling is typically smaller than with single-leg options. The long leg you own also loses value as the trade moves against you, partially offsetting the loss on the short leg.

For credit spread rolls, the same credit-only rule applies, but you may find that rolling opportunities are more limited. Spreads that are deep in the money often cannot be rolled for a credit, and the right move is usually to close and accept the loss. Credit spreads are designed to have defined maximum losses for a reason.

The Math of Rolling: How Credits Compound Over Time

Understanding the compounding effect of rolling credits is essential for evaluating whether a roll makes sense. Each credit you collect through rolling has three effects on your position.

Effect 1: Breakeven improvement. Your effective breakeven improves by the amount of the net credit. After three rolls collecting $1.00, $0.75, and $0.50, your breakeven has improved by $2.25 from your original position.

Effect 2: Annualized return adjustment. Each roll extends the duration of your trade. While the total credit collected increases, the time invested also increases. A position that earned $3.75 over 4 months has an annualized return of approximately 22.5% on a $50 stock (assuming one contract). That is a solid return, but it was earned over 4 months instead of 1. You need to compare this against what the same capital could have earned in a fresh trade.

Effect 3: Opportunity cost. Capital committed to a rolled position is unavailable for new trades. If you are rolling a $5,000 cash-secured put over and over, that $5,000 is locked up. The credits you collect need to be measured against what you could earn deploying that same $5,000 in a fresh, optimal position.

The math often favors rolling once or twice, but beyond that, the diminishing credits and rising opportunity cost usually make closing and redeploying the better choice. This is not a hard rule, but it is a useful guideline.

Common Mistakes When Rolling Options for Credit

Avoiding these mistakes will save you money and frustration.

Mistake 1: Rolling too early. If your option still has significant time until expiration and the stock is only slightly past your strike, rolling too early means you leave extrinsic value on the table. Time decay accelerates in the final 7-14 days before expiration. Often, waiting to roll until closer to expiration provides a better credit because the current option has decayed more.

Mistake 2: Rolling automatically without evaluating alternatives. Some traders develop a habit of always rolling, no matter what. Rolling should be a deliberate decision, not a reflex. Before every roll, ask: is this the best use of my capital? Would closing and opening a completely new position on a different stock be more profitable?

Mistake 3: Rolling for a debit. This bears repeating because it is the most costly mistake. If you cannot roll for a credit, that is valuable information. The market is telling you that the position has deteriorated past the point where rolling is beneficial. Take the loss or accept assignment.

Mistake 4: Ignoring earnings dates. Rolling into an expiration that includes an earnings announcement can expose you to massive gap risk. Always check the earnings calendar before rolling. A stock that was at $48 can be at $38 the morning after a bad earnings report, and no amount of rolling can fix that.

Mistake 5: Not tracking roll credits accurately. Every roll changes your effective cost basis, breakeven, and total return. If you are not tracking these meticulously, you are making future decisions based on incorrect numbers. After managing 15+ wheel positions with multiple rolls each, your spreadsheet becomes a nightmare. Which positions have been rolled? How many times? What is the total credit collected? This is exactly why platforms like QuantWheel exist, built specifically for wheel traders who need to track this stuff without losing their minds.

How to Decide: Roll, Close, or Take Assignment

When a short option is challenged, you have three choices. Here is a framework for deciding between them.

Choose to roll when:

- You can collect a net credit

- You still believe in the underlying stock (fundamentals have not changed)

- The implied volatility is elevated (better premiums for the new option)

- You have not rolled more than 2-3 times already

- There is no earnings announcement before the new expiration

Choose to close the position when:

- You cannot roll for a credit

- The stock’s fundamentals have deteriorated

- You have better opportunities for the capital

- You have rolled multiple times and credits are getting thin

- The position size has become too large relative to your portfolio

Choose to accept assignment (for put sellers) when:

- You are happy to own the stock at your effective cost basis

- The stock is a quality company you want in your portfolio

- You have a covered call plan ready for the assigned shares

- Assignment fits within your portfolio allocation rules

There is no universally right answer. The best choice depends on your specific situation, portfolio context, and market outlook. What matters is having a consistent framework for making the decision rather than reacting emotionally in the moment.

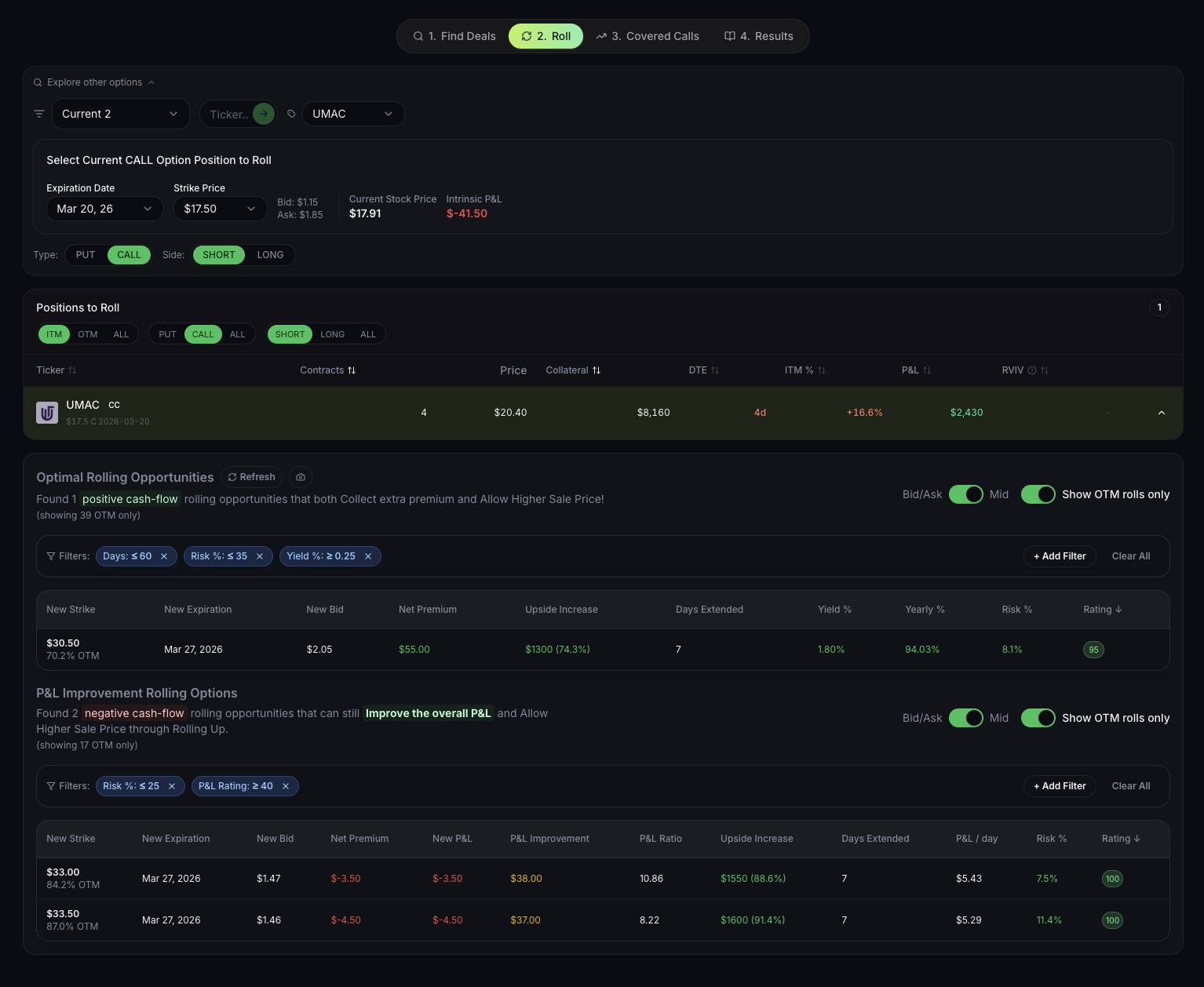

Using the Roll Assistant: How Technology Speeds Up Decision-Making

One of the biggest challenges with rolling is the sheer number of options to evaluate. For a single position, you might have 5-10 strike prices across 3-4 expiration dates. That is 15-40 potential rolls to analyze, each with different risk-reward characteristics. Doing this math manually takes 30-45 minutes per position, and by the time you have finished calculating, the prices may have changed.

When deciding whether to roll, many traders use QuantWheel’s Roll Assistant. It compares every possible strike and expiration, calculates the return for each, and recommends the optimal roll in seconds. Instead of spending 45 minutes comparing 12 different roll options on a calculator, you get a ranked list of every viable roll with the math already done. This does not replace your judgment, but it does eliminate the tedious number-crunching that leads to analysis paralysis and missed opportunities.

[QUANTWHEEL SCREENSHOT] Feature: Roll Assistant Show: Multiple roll options ranked by return with comparison Caption: “QuantWheel’s Roll Assistant analyzes every possible roll and ranks them by return, so you can make faster, data-driven decisions.” CTA: “See Roll Assistant in Action” links to /features/roll-assistant

Advanced Rolling Techniques for Experienced Traders

Once you have mastered the basics of rolling for credit, there are several advanced techniques to consider.

Technique 1: The Ladder Roll. Instead of rolling to the same strike, you systematically roll down (for puts) or up (for calls) by one strike increment each time. Each roll collects a smaller credit, but you also reduce your risk incrementally. Over several rolls, you can move your strike significantly while collecting credits at each step.

Example: Sold $50 put, rolled to $49 for $0.50 credit, then rolled to $48 for $0.40 credit, then rolled to $47 for $0.35 credit. Total credit collected: $1.25. Strike improved from $50 to $47. Much safer position, and you got paid $1.25 to get there.

Technique 2: The Split Roll. If you have multiple contracts, roll half and close half. This reduces your exposure while maintaining some upside from the rolled portion. It is a compromise between fully rolling and fully closing.

Technique 3: Calendar Roll to Higher IV. When implied volatility has spiked (such as before an earnings report two cycles out or during a market selloff), rolling to that high-IV expiration generates outsized credits. The elevated volatility inflates the premium you receive on the new option, making the roll more profitable. Just be mindful of what is causing the spike.

Technique 4: The Strategic Width Change. For credit spread traders, you can change the width of your spread when rolling. For example, rolling a 5-wide spread to a 3-wide spread reduces your maximum risk even if the credit is similar. This is a sophisticated adjustment that effectively repositions your risk-reward.

Real-World Rolling Scenario: A Full Wheel Cycle with Rolls

Let us walk through a complete wheel cycle that includes multiple rolling adjustments. This example uses hypothetical prices for educational purposes.

Setup: You identify Stock ABC trading at $55. You are comfortable owning it at $50 or below. You sell a $50 cash-secured put expiring in 30 days for $1.50. Cash requirement: $5,000. Premium collected: $150.

Week 3: Stock drops to $49. Your put is in the money. You check the next monthly expiration and see you can roll the $50 put for a $0.80 net credit. You roll. Total premium: $2.30. Effective breakeven: $47.70.

Week 7: Stock is at $48. Still below your strike. You roll again to the next month for a $0.60 net credit. Total premium: $2.90. Effective breakeven: $47.10.

Week 11: Stock is at $47. The credit available for rolling has shrunk to $0.20. You decide the opportunity cost is too high and accept assignment. You now own 100 shares of Stock ABC at $50 strike, but your effective cost basis is $50 minus $2.90 equals $47.10.

Week 12: Stock is at $47. You sell a $49 covered call for $1.20. If called away, your profit would be ($49 minus $47.10) plus $1.20 equals $3.10 per share.

Week 16: Stock rallies to $49.50. Your call is tested. You roll the call up and out to a $51 call for a $0.40 net credit. Total call premium: $1.60.

Week 20: Stock is at $52. Call expires in the money. Shares are called away at $51. Final math: Stock sold at $51.00, effective cost $47.10, total call premium $1.60. Total profit: $51.00 minus $47.10 plus $1.60 equals $5.50 per share ($550 per contract).

Without rolling, the original trade would have either resulted in assignment at $48.50 breakeven (only the original put premium) or a loss if the stock stayed below $50. Rolling added $2.90 in premium on the put side and $0.40 on the call side, turning a challenging trade into a $550 winner.

This is the power of rolling options for credit within the wheel strategy. And tracking all of these adjustments, premiums, and cost basis changes across a real portfolio with 10-15 positions? That is where automated tracking becomes essential.

Tracking Your Rolls: Why Accuracy Matters More Than You Think

After two or three rolls, keeping track of your actual numbers gets complicated fast. Your broker will show you the strike price as your cost basis, but that number does not include any of the premium you collected through puts, rolls, or covered calls. Your real cost basis is different from what your broker reports.

Tracking inaccuracies compound over time. If you miscalculate your breakeven by even $0.50, you might hold a position longer than you should or exit too early. Multiply that error across 10-15 positions and the impact on your annual returns becomes significant.

Many wheel traders start with spreadsheets and they work fine for 1-3 positions. But once you scale to 10+ positions with multiple rolls each, the spreadsheets break. Formulas get complicated, manual entry errors creep in, and one missed roll credit throws off everything downstream.

This is exactly why QuantWheel’s Wheel Native Journal exists. It tracks your full wheel cycle, including every single roll, from CSP to assignment to covered call to exit. Each roll credit is automatically captured and your cost basis updates in real time. You always know your true breakeven, total premium collected, and return on every position, without maintaining a single spreadsheet.

Key Takeaways for Rolling Options for Credit

Rolling options for credit is one of the most valuable skills in a premium seller’s toolkit. It allows you to manage losing positions, extend profitable setups, and compound your returns through additional premium collection. But it is not a magic fix.

The most important principles to remember are: always roll for a credit, never for a debit. Have a clear decision framework for when to roll, when to close, and when to accept assignment. Track every roll credit meticulously because your real cost basis depends on it. Recognize when the rolling opportunity has passed and it is time to move on to the next trade.

Whether you are running the wheel strategy, selling cash-secured puts, or writing covered calls, rolling for credit should be a core part of your position management system. It will not win every trade, but it will give you the best mathematical chance of turning challenging positions into profitable ones over time.

Start your free trial of QuantWheel →

Risk Disclosure: Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.