If you want to learn more, keep reading. I go through every possible scenario there is on how and when to roll covered call positions.

Author: David Romic – retail options trader and active member in the options trading communities on Reddit (u/thedavidromic).

I share wheel strategy setups, trade management, and lessons learned from real positions.

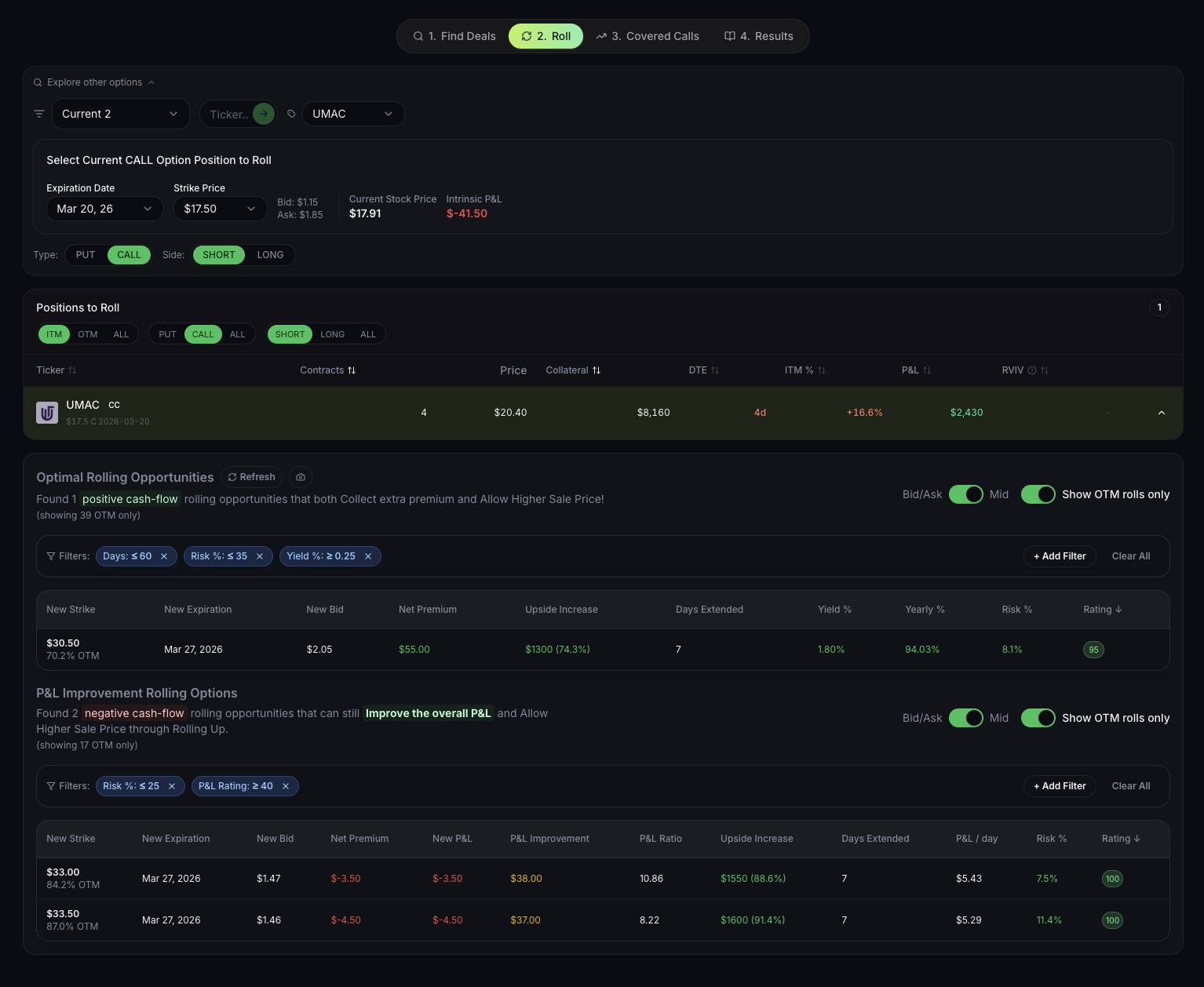

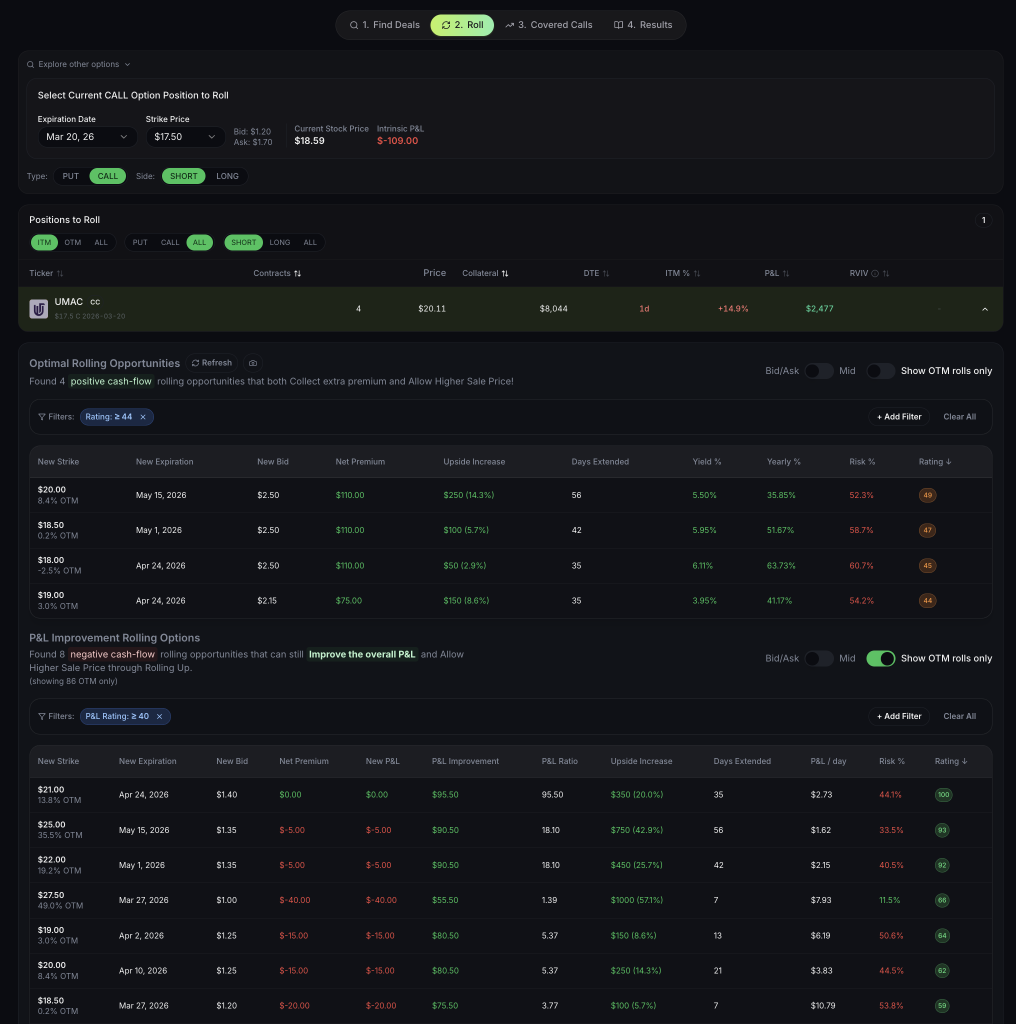

Let’s kick it off immediately with an example..

Example trade:

$UMAC $17.5 CC with 1 days left until expiration, was 20% ITM 2 days ago and now it’s at 10% ITM.

Now that you have a clean slate to make a decision, which one would you pick?

Answer: The first one, either from table 1 or table 2. (I went with the first one from table 2, this depends on what’s happening out there in the real world)

Why? It gives you an amazing value – upside (from $17.50 -> $21) which means you improve your PnL significantly and it also doesn’t cost you anything at the end.

This example shows how streamlined the whole process of rolling covered calls can be. Below you can find some practical situations and frameworks which can also help you understand how to roll covered calls.

TLDR: Everything You Need to Know About Rolling Covered Calls

Rolling a covered call means buying back your current call option and simultaneously selling a new one with different parameters – typically a later expiration date, higher strike price, or both. This technique allows you to continue collecting premium on stock you own while managing your exit strategy.

When to Roll Covered Calls:

- Your call reaches 50% of max profit with 21+ days remaining (optimize time decay)

- Stock price exceeds your strike by 3-5% and you want to avoid assignment (roll up and out)

- Approaching expiration with stock near strike price and new premium available (roll out for time)

- You want to continue generating income instead of closing the full wheel position

When NOT to Roll:

- Net credit from rolling is minimal (<0.5% of strike price)

- You’re comfortable taking profits and accepting assignment

- Stock fundamentals deteriorated and you want to exit anyway

- Better opportunities exist elsewhere for your capital

Rolling covered calls is a core wheel strategy skill that bridges premium collection and position management. Master when to roll (and when to accept assignment), and you’ll extract significantly more value from your wheel positions over time.

What is Rolling a Covered Call?

Rolling a covered call is the process of closing your existing covered call position and simultaneously opening a new covered call with different parameters. You “buy to close” the current call and “sell to open” a new call in a single transaction.

The three ways to roll:

Rolling Out (Same strike, later expiration):

- Keep the same strike price

- Extend to a later expiration date

- Collect additional time premium

- Use when: Stock is stable near strike, want more income

Rolling Up (Higher strike, same expiration):

- Move to a higher strike price

- Keep the same expiration date

- Gives stock more appreciation room

- Use when: Stock has rallied significantly

Rolling Up and Out (Higher strike, later expiration):

- Move to higher strike AND later expiration

- Most common rolling strategy for wheel traders

- Maximizes both premium and appreciation potential

- Use when: Stock rallies above strike and you want to continue the position

How Rolling Works Mechanically

Let’s use a real example to understand the transaction:

Current Position:

- Own 100 shares of NVDA at $880 (cost basis after assignment)

- Sold $900 covered call, collected $5.00 premium

- Current NVDA price: $920

- Call now worth: $22.00

- Days to expiration: 7

Rolling Decision: Your shares will likely get called away at $900 (you’d make $20/share on the stock + $5 premium = $25/share total). But NVDA has momentum and you want to stay in the position.

Rolling Up and Out:

- Buy to close: $900 call for $22.00 (debit)

- Sell to open: $930 call, 30 DTE for $18.50 (credit)

- Net debit: $3.50 per share ($350 total)

Result After Rolling:

- You paid $350 to roll

- But now you can capture $30 more stock appreciation ($930 strike vs $900)

- Plus you collected $18.50 in new premium for the next 30 days

- Total potential: $30 stock gain + $18.50 premium – $3.50 roll cost = $45 potential

This is where most wheel traders get stuck – calculating whether the roll is worth it requires comparing multiple scenarios, factoring in probability of success, and considering opportunity cost. Professional traders use tools like QuantWheel’s Roll Assistant to analyze all possible roll combinations and identify the optimal choice based on your criteria (max return, min time, or balanced risk-reward).

When to Roll Covered Calls: The Decision Framework

The decision to roll a covered call isn’t arbitrary – it follows a systematic framework based on your position’s current status, the premium available, and your strategy goals.

Scenario 1: Roll for Profit Taking (50% Rule)

When: Your covered call has reached 50% of its maximum profit with 21+ days until expiration.

Why: Options decay accelerates in the final 30 days. By closing at 50% profit with significant time remaining, you free up risk capital while capturing most of the time decay. You can then sell a new call to start collecting fresh premium.

Example:

- Sold $150 call for $4.00 (max profit $400)

- Call now worth $2.00 (50% profit achieved)

- 28 days until expiration

Action: Close the $150 call for $2.00 (keep $200 profit), sell a new $150 or $155 call for the next expiration cycle and collect new premium.

Math: You booked $200 profit in ~14-16 days. Selling a new 30-45 DTE call might collect another $3.50-4.50, restarting your premium collection with fresh time value.

This is the “rinse and repeat” approach many successful wheel traders use – close early at 50% profit, redeploy into new positions. Over 12 months, this approach often outperforms holding each position to expiration because you’re constantly harvesting time decay at its optimal rate.

Scenario 2: Rolling Up and Out to Avoid Assignment

When: Stock price has moved 3-5% above your strike price and you want to avoid having shares called away.

Why: Your shares are in-the-money and will likely get assigned at expiration. If you believe the stock has further upside, rolling to a higher strike lets you participate in more appreciation while collecting additional premium.

Example:

- Current position: Short $100 call on stock trading at $108

- Your shares will get called away at $100 (missing the $8 gain above strike)

- Roll to $110 call, 30-45 days out

Calculation:

- Buy to close $100 call: $9.00 debit (intrinsic value + remaining time)

- Sell to open $110 call, 45 DTE: $7.50 credit

- Net debit: $1.50 per share

Analysis: You paid $150 to roll, but now you can capture $10 more in stock appreciation ($110 strike vs $100). If the stock reaches $110, your additional gain is $10/share – $1.50 roll cost = $8.50 net benefit.

Critical consideration: You’re making a directional bet that the stock continues higher. If the stock reverses and falls back to $100, you paid $150 for nothing. Only roll up when you have conviction in continued upside.

Scenario 3: Rolling Out for More Time Premium

When: Approaching expiration (7-14 days), stock is near your strike price, and meaningful premium exists in the next expiration cycle.

Why: If your call is barely in-the-money or at-the-money, you can close it cheaply and sell a new call at the same strike for the next cycle, collecting net credit while maintaining your position.

Example:

- Short $200 call, stock trading at $198

- 7 days to expiration

- Call worth: $1.20 (mostly intrinsic, little time value)

- Next month’s $200 call: $5.50

Rolling Transaction:

- Buy to close current $200 call: $1.20 debit

- Sell to open next month $200 call: $5.50 credit

- Net credit: $4.30 per share ($430 collected)

Result: You collected $430 to extend your position 30 days. If the stock stays below $200, you keep the new premium. This is the safest type of roll – you’re collecting significant net credit and not changing your strike price.

Scenario 4: When NOT to Roll (Accept Assignment)

Rolling isn’t always optimal. Sometimes accepting assignment and taking your profit is the right move.

Don’t roll when:

1. Minimal net credit available (<0.5% of strike price): If rolling only nets you $0.50-0.75 per share, the time commitment and opportunity cost often aren’t worth it. Accept assignment and redeploy capital elsewhere.

2. Stock has appreciated significantly and you want to take profits: If your stock is up 15-20% from your original cost basis and you’re comfortable exiting, let the shares get called away. You’ve achieved solid gains – don’t get greedy.

3. Stock fundamentals deteriorated: If the company reports bad earnings, loses market share, or faces headwinds, accept assignment gladly. You’re getting out at a good price with premium collected.

4. Better opportunities exist elsewhere: Capital has opportunity cost. If you can deploy your capital into a higher-premium, better risk-reward position, accept assignment and move on.

Example of accepting assignment:

- You own shares with $85 cost basis (after put premium)

- Current stock price: $102

- Your $100 covered call will be assigned

- Total gain: $15/share (stock gain) + put premium collected + call premium = excellent return

Action: Let assignment happen. You’ve successfully completed a wheel cycle with strong returns. Start a new cycle by selling cash-secured puts on a different stock or the same stock if you want to re-enter.

This is the mentality shift that separates good wheel traders from those who get stuck: assignment is success, not failure. You collected premium on the way down (put), collected premium on the way up (call), and captured stock appreciation. Mission accomplished.

How to Calculate the Optimal Roll (Step-by-Step)

Deciding WHETHER to roll is one thing – determining the BEST roll is another. Here’s the systematic process:

Step 1: Identify Your Rolling Options

For any covered call, you have multiple rolling choices:

Expiration options:

- Next weekly expiration (+7 days)

- Next monthly expiration (+30 days)

- Quarterly expiration (+45-60 days)

Strike options:

- Same strike (rolling out only)

- One strike higher (typically $5 or $10 higher)

- Two strikes higher (aggressive appreciation capture)

Combinations: 3 expirations × 3 strikes = 9 possible rolls to analyze

This is where manual analysis breaks down. Checking 9 different roll options with real-time pricing, calculating net credit/debit for each, comparing return profiles – it takes 20-30 minutes per position. With 10+ positions, this becomes unmanageable.

Step 2: Calculate Net Credit/Debit for Each Option

For each possible roll:

Net Credit/Debit = New premium received – Cost to close current position

Example: Rolling a $150 call (currently $3.50) to $155 call expiring in 30 days ($4.80):

Net Credit = $4.80 – $3.50 = $1.30 credit

You receive $130 per contract for rolling.

Rule of thumb: Aim for at least $0.50-1.00 net credit when rolling out, or accept paying up to 1-2% of strike price when rolling up for significant additional appreciation potential.

Step 3: Compare Return Potential

For each roll option, calculate the maximum return if stock reaches the new strike:

Max Return = (New Strike – Current Stock Price) + Net Credit from Roll

Example Comparison (Stock at $152, current call worth $4.00):

Option A: Roll to $155, 30 DTE, collect $5.20

- Net credit: $5.20 – $4.00 = $1.20

- Max return: ($155 – $152) + $1.20 = $4.20 per share

- Days: 30

- Return per day: $0.14

Option B: Roll to $160, 45 DTE, collect $4.80

- Net credit: $4.80 – $4.00 = $0.80

- Max return: ($160 – $152) + $0.80 = $8.80 per share

- Days: 45

- Return per day: $0.20

Option C: Roll to $155, 45 DTE, collect $6.50

- Net credit: $6.50 – $4.00 = $2.50

- Max return: ($155 – $152) + $2.50 = $5.50 per share

- Days: 45

- Return per day: $0.12

Analysis: Option B offers highest return per day IF stock reaches $160. Option C offers best risk-adjusted return with moderate strike increase and strong premium collection.

Step 4: Factor in Probability of Success

Use delta as a proxy for probability that the stock finishes above your new strike:

- 30-delta call: ~70% chance of expiring worthless (you keep premium)

- 40-delta call: ~60% chance of expiring worthless

- 50-delta call: ~50% chance of expiring worthless

Conservative wheel traders target 20-30 delta calls (high probability of keeping shares or getting called away at profitable strikes).

Aggressive wheel traders target 35-45 delta calls (higher premium, accept more frequent assignment).

Multiply your max return by probability of success to get expected value:

Option B: $8.80 max return × 65% success probability = $5.72 expected value

Option C: $5.50 max return × 72% success probability = $3.96 expected value

Even though Option B has higher absolute return, Option C might be preferable for conservative traders who want higher probability outcomes.

Step 5: Make the Decision

Choose the roll that best aligns with your goals:

Maximize income: Choose highest net credit received Maximize stock appreciation: Choose highest strike with acceptable premium Balance both: Choose highest expected value (return × probability) Minimize time: Choose shortest expiration that still collects meaningful premium

Here’s the problem: This analysis takes 20-30 minutes per position. If you’re managing 10 wheel positions, that’s 3-5 hours every time you need to make rolling decisions.

This is exactly where QuantWheel’s Roll Assistant eliminates the tedious math. It analyzes every possible roll combination in real-time, ranks them by your preferred criteria (max return, best probability, or balanced), and shows you the before/after comparison instantly. What takes 30 minutes manually happens in 15 seconds.

Start your free trial of QuantWheel →

Common Rolling Mistakes (And How to Avoid Them)

Mistake 1: Rolling for Emotional Reasons

The mistake: You’re emotionally attached to the stock and keep rolling up to avoid assignment, even when the math doesn’t support it.

Example: Stock rallied 25% from your cost basis. You keep rolling to higher strikes, paying net debits each time, because you “don’t want to miss more upside.”

Why it’s costly: You’re turning a winning position into a losing one by paying to maintain exposure. You’ve already won – take the profit.

Fix: Set a rule: “I’ll accept assignment if my total return exceeds 15%” or “I’ll only roll if I collect net credit.” Remove emotion from the decision.

Mistake 2: Rolling Too Early

The mistake: Rolling when your call still has 30-40 days to expiration and significant extrinsic value.

Example: Sold a $140 call for $4.50. Stock jumps to $145 on day 5. You panic and immediately roll up, paying $6.50 to close and collecting $5.00 for the new call. Net debit: $1.50.

Why it’s costly: You closed a position with tons of remaining time value. If the stock had pulled back to $140 by expiration, you would have kept the full $4.50. Instead, you locked in a $1.50 loss.

Fix: Wait until your call has less than 21 days until expiration OR the stock moves significantly (>5% beyond strike) before considering rolling. Let time decay work in your favor first.

Mistake 3: Rolling for Tiny Net Credits

The mistake: Rolling out for $0.25-0.50 net credit just to “stay active” in the position.

Example: Roll from current month to next month, collecting $0.40 net credit for 30 more days of exposure.

Why it’s costly: You’re tying up capital for minimal return. That $0.40 per share ($40 per contract) for 30 days is 0.3% monthly return – terrible risk-adjusted performance. Your time and capital are worth more.

Fix: Only roll if you’re collecting at least 1-2% of strike price as net credit. Otherwise, accept assignment or let the position expire.

Mistake 4: Not Comparing to Alternatives

The mistake: Focusing only on “can I roll?” without asking “should I roll versus other options?”

Example: Your $100 call can be rolled to $105 for $1.00 net credit. Meanwhile, you could accept assignment, take your profit, and redeploy into a new stock offering 8% premium for the same timeframe.

Why it’s costly: Opportunity cost. Your capital would generate better returns elsewhere.

Fix: Always compare rolling to the best alternative use of your capital. If accepting assignment and starting a fresh wheel cycle on a high-IV stock offers better returns, do that instead.

Mistake 5: Ignoring Earnings Dates

The mistake: Rolling into an expiration that spans an earnings announcement without adjusting your strike.

Example: Roll to 30 days out, not realizing earnings is in 20 days. The IV crush after earnings collapses your call’s value, but the stock also moves unpredictably.

Why it’s costly: Earnings introduce binary risk. You might get lucky or get crushed – it’s a coin flip.

Fix: Check earnings calendar before rolling. Either:

- Roll to expiration BEFORE earnings (collect premium, avoid risk)

- Roll to higher strike to give cushion for earnings volatility

- Accept assignment before earnings and reassess after

QuantWheel shows earnings dates directly on your position dashboard and warns you when a roll would span earnings, helping you avoid this mistake automatically.

Advanced Rolling Strategies

Once you master basic rolling, these advanced techniques can optimize your returns further:

Strategy 1: The “Rolling Down” Repair

When to use: Stock declined significantly from your cost basis, your covered call is far out-of-the-money, and you want to lower your breakeven.

How it works: Your call is worthless, so you let it expire and immediately sell a new call at a LOWER strike than before, collecting more premium.

Example:

- Cost basis: $150 (after assignment)

- Sold $155 call for $3.00, collected premium

- Stock drops to $140

- $155 call expires worthless (you keep $3 premium)

- Sell new $145 call for $4.50

Result: You’re lowering your strike to collect more premium while reducing your breakeven. Your new effective breakeven is $150 – $3 – $4.50 = $142.50.

Risk: If stock recovers to $145, shares get called away. You’d miss gains from $145-$150. Only use when you’re willing to exit at the lower strike.

Strategy 2: The “Aggressive Roll Up” for Momentum Stocks

When to use: High-conviction on continued stock upside, willing to pay debit to capture more appreciation.

How it works: Pay a net debit to roll to a significantly higher strike, giving yourself much more upside exposure.

Example:

- Stock at $180, short $175 call worth $7.50

- Pay $7.50 to close, sell $195 call (45 DTE) for $5.00

- Net debit: $2.50 per share ($250)

Calculation: You paid $250 to extend, but gained $20 of additional appreciation potential ($195 vs $175 strike). Breakeven is stock reaching $182.50. If stock reaches $195, you’ve captured $15/share extra vs original $175 strike.

Risk: You’re making a leveraged bet. If stock reverses, you paid $250 and gained nothing. Only use with high conviction and strong technicals.

Strategy 3: The “Defensive Roll Out” for Challenged Positions

When to use: Stock is declining, you’re underwater, but believe in long-term recovery.

How it works: Keep rolling out at same or lower strikes, collecting premium to reduce cost basis while waiting for recovery.

Example:

- Cost basis after assignment: $200

- Stock currently: $185

- Short $190 call expiring in 14 days, worth $0.50

- Roll to $190 call, 45 DTE for $4.80

- Net credit: $4.30 per share

Result: You collected $4.30, lowering your cost basis to $195.70. If stock recovers to $190, you’re only down $5.70/share instead of $10. Keep repeating monthly.

Risk: You’re “averaging down” with time. If stock never recovers, you’re collecting small premium while holding a losing position. Set a stop-loss threshold (e.g., “If stock hits $170, I exit regardless”).

Strategy 4: The “Earnings Straddle Roll”

When to use: Earnings coming up, high IV, want to capture both sides.

How it works: Before earnings, close your covered call. After earnings (IV crush), sell a new call at attractive strikes with deflated IV.

Example:

- 7 days before earnings, buy back $150 call for $5.00

- After earnings, IV drops 40%, stock settles at $152

- Sell new $155 call for $4.00 (post-IV crush pricing)

- Net cost: $1.00 for timing arbitrage

Result: You avoided being locked into a position during binary event, then re-established after IV normalized. The $1.00 cost might be worth it if earnings moved stock unpredictably.

Risk: If stock gaps up significantly on earnings, you’ll miss that move. Only use when uncertainty is high and you want optionality.

Rolling and Cost Basis: The Accounting Nobody Talks About

Here’s the complexity that trips up 90% of wheel traders: tracking your real cost basis through multiple rolls.

The Problem

When you roll a covered call:

- You’re paying to close the old call (reduces your overall premium collected)

- You’re collecting premium for the new call (increases premium collected)

- Your NET cost basis changes with each roll

- Brokers don’t track this across rolls – you have to do it manually

Example of Cost Basis Confusion

Starting position:

- Bought 100 shares at $100 via assignment on cash-secured put

- Collected $3 put premium

- Real cost basis: $97 per share

First covered call:

- Sold $105 call for $4.00

- New cost basis: $97 – $4 = $93 per share

First roll (stock at $107):

- Paid $5.50 to close $105 call

- Collected $6.00 for $110 call, 30 DTE

- Net credit from roll: $0.50

- New cost basis: $93 – $0.50 = $92.50 per share

Second roll (stock at $112):

- Paid $7.20 to close $110 call

- Collected $7.00 for $115 call, 45 DTE

- Net debit from roll: $0.20

- New cost basis: $92.50 + $0.20 = $92.70 per share

Finally assigned at $115:

- Sold shares at $115

- Real cost basis: $92.70

- Profit: $22.30 per share

- Your broker shows: ~$15-17 (because they don’t track premium properly)

Why This Matters

Tax reporting: You need accurate cost basis for Schedule D. If you don’t track every roll, you’ll either:

- Overpay taxes (reporting higher cost basis than reality)

- Underpay taxes and face penalties (reporting lower cost basis)

Performance measurement: You can’t know if your wheel strategy is actually profitable without tracking true cost basis across complete cycles.

Position management: Without knowing your real breakeven, you can’t make good rolling decisions.

The Manual Tracking Nightmare

To track this correctly, you need:

- Spreadsheet tracking every roll transaction

- Premium received/paid for each roll

- Running cost basis calculation

- Multiplication across 10-15 positions

- Updates twice per week as you manage positions

Reality: 95% of wheel traders don’t track this properly. They estimate, guess, or use broker figures that are incomplete.

This is specifically why QuantWheel exists – it automatically calculates and adjusts your cost basis through every roll, assignment, and position adjustment. When you make a rolling transaction, QuantWheel updates your real cost basis instantly. At tax time, you export accurate Schedule D data without manual reconciliation.

[QUANTWHEEL SCREENSHOT] Feature: Cost Basis Tracking Through Rolls Show: Position showing original cost, premium adjustments from multiple rolls, current real cost basis Caption: “QuantWheel automatically tracks your cost basis through every roll – no spreadsheet needed” CTA: “See Cost Basis Tracking →” links to /features/cost-basis

Rolling in the Complete Wheel Strategy Context

Rolling covered calls is one piece of the wheel strategy puzzle. Here’s how it fits into the complete cycle:

Complete Wheel Cycle with Rolling

Phase 1: Sell Cash-Secured Put

- Collect premium while waiting for assignment

- If not assigned: Roll put or let expire, sell new put

- If assigned: Move to Phase 2

Phase 2: Assigned Stock + Sell Covered Call

- Now own 100 shares (cost basis = strike – put premium)

- Sell covered call to collect premium

- This is where rolling decisions happen

Phase 3A: Roll Covered Call (Continue Position)

- Stock moves up but you want to stay in position

- Roll up and out to collect more premium + capture appreciation

- Repeat until ready to exit or get assigned

Phase 3B: Accept Assignment (Exit Position)

- Stock reaches your strike at expiration

- Shares called away

- Calculate total return: put premium + call premium + stock gains

- Start new cycle with different stock or same stock

When Rolling Fits Your Strategy

Roll covered calls when:

- You have high conviction on continued upside

- Premium collection opportunities remain attractive

- You’re in efficient tax position (avoiding short-term gains)

- Position management is worth your time investment

Accept assignment when:

- You’ve achieved target returns (15-25% total wheel cycle)

- Better opportunities exist elsewhere

- Stock fundamentals changed negatively

- Time commitment isn’t worth marginal additional premium

The Wheel Trader’s Rolling Rules

Based on analysis of successful wheel strategy traders, these rules optimize long-term returns:

Rule 1: Close at 50% profit with 21+ DTE, roll to new cycle Rule 2: Roll up only if collecting net credit OR stock up 5%+ with conviction Rule 3: Never pay more than 1% of strike price to roll Rule 4: Accept assignment at 15%+ total cycle return Rule 5: Check earnings calendar before every roll Rule 6: Track real cost basis through all rolls (manually or with QuantWheel)

Following these rules systematically prevents emotional rolling decisions and optimizes your returns per unit of time and capital deployed.

Tools and Platforms for Rolling Covered Calls

Broker Platforms

Most brokers allow rolling in one transaction:

Fidelity: Use “Roll” option in position management TD Ameritrade: “Create Rolling Order” in thinkorswim Interactive Brokers: “Roll Option Position” from account management Tastyworks: “Roll” button on position page Robinhood: No built-in roll feature, must close and open separately

Pros: Integrated with your trading account, execute rolls quickly Cons: Minimal decision support, no comparison of roll options, no cost basis tracking through rolls

Professional Wheel Strategy Platforms

QuantWheel (wheel strategy specialist):

- Roll Assistant analyzes all possible rolls, ranks by criteria

- Automatic cost basis adjustment through rolls

- Shows earnings calendar conflicts

- Alerts for optimal rolling opportunities

- Full wheel cycle tracking

Pros: Built specifically for wheel traders, automates tedious calculations Cons: Separate platform from broker (though broker integration available)

Generic Options Platforms (OptionStrat, OptionAlpha, etc.):

- Focus on options education and generic strategies

- Some have rolling calculators

- Not wheel-strategy specific

Pros: Good for learning options mechanics Cons: Manual tracking required, no wheel-specific features, no cost basis management

Spreadsheet Tracking

Many traders start with Excel/Google Sheets:

Pros: Free, customizable, you control data Cons: Manual data entry, calculation errors, no real-time updates, breaks at scale, no automatic cost basis tracking

Reality: Spreadsheets work for 1-3 positions. Past that, the time investment and error rate make professional tools worthwhile.

The economics are simple: If QuantWheel’s Roll Assistant saves you 30 minutes per week on rolling decisions and prevents one $200 rolling mistake per month, the $49/month subscription pays for itself 5x over. Most wheel traders managing 10+ positions save 3-5 hours per week on tracking and analysis.

Start your free trial of QuantWheel →

Real-World Rolling Examples

Example 1: Successful Roll Up and Out (Tech Stock Rally)

Starting Position:

- Own 100 shares PLTR at $64 (cost basis after put assignment)

- Sold $68 covered call, collected $3.20

- 14 days later: PLTR rallies to $72 on AI news

- Current call value: $5.40

Decision: Roll up and out to capture more upside

Rolling Transaction:

- Buy to close $68 call: $5.40 debit

- Sell to open $75 call, 45 DTE: $6.80 credit

- Net credit: $1.40 per share ($140 collected)

Outcome (45 days later):

- PLTR reaches $77, shares assigned at $75

- Stock gain: $75 – $64 = $11 per share

- Premium collected: $3.20 (original) + $1.40 (roll) = $4.60

- Total profit: $15.60 per share = 24.4% return in ~60 days

Analysis: Rolling up allowed capture of additional $7/share appreciation ($75 strike vs $68) while collecting $1.40 extra premium. If had accepted assignment at $68, would have made only $7.20 total. Rolling added $8.40/share (116% more profit).

Example 2: Defensive Rolling on Declining Stock

Starting Position:

- Own 100 shares BABA at $88 (cost basis after assignment)

- Sold $92 covered call for $2.80

- Stock declines to $84 on China regulatory concerns

- Current call value: $0.40

Decision: Roll out at lower strike to collect premium and reduce cost basis

Rolling Transaction:

- Buy to close $92 call: $0.40 debit

- Sell to open $87 call, 45 DTE: $3.20 credit

- Net credit: $2.80 per share

Result:

- New cost basis: $88 – $2.80 – $2.80 (roll) = $82.40

- New breakeven: $82.40

- If assigned at $87, profit would be $4.60/share despite stock decline

What happened next: BABA continued declining to $78. Rolled again to $82 call for $2.60 net credit. Final cost basis: $79.80. Eventually assigned at $82 when stock recovered, final profit: $2.20/share despite buying at $88 originally.

Analysis: Rolling defensively turned a losing position into slight profit by systematically lowering cost basis. Required patience and 3 rolling transactions over 4 months, but preserved capital.

Example 3: Mistake – Rolling Without Net Credit

Starting Position:

- Own 100 shares TSLA at $245 (cost basis after assignment)

- Sold $255 covered call for $8.50

- TSLA gaps to $268 on delivery numbers

- Current call value: $16.20

Bad Decision: Emotional roll to avoid assignment

Rolling Transaction:

- Buy to close $255 call: $16.20 debit

- Sell to open $275 call, 30 DTE: $12.40 credit

- Net debit: $3.80 per share ($380 paid to roll)

Outcome: TSLA drops back to $258 over next 2 weeks. New $275 call expires worthless.

Total result:

- Stock gain: $258 – $245 = $13/share

- Premium: $8.50 (original) – $3.80 (roll cost) = $4.70 net

- Total: $17.70/share

What should have happened: Accept assignment at $255

- Stock gain: $255 – $245 = $10/share

- Premium: $8.50

- Total: $18.50/share

Lesson: The emotional roll COST $0.80/share ($80) versus accepting assignment. The $20 extra stock appreciation potential ($275 vs $255 strike) wasn’t worth the $380 debit paid.

Conclusion: Master Rolling to Master the Wheel

Rolling covered calls transforms from guesswork to systematic process once you understand the frameworks:

- Know when to roll: 50% profit rule, stock movement thresholds, expiration timing

- Calculate optimal rolls: Compare all options by net credit, return potential, and probability

- Avoid common mistakes: No emotional rolling, avoid tiny credits, compare to alternatives

- Track cost basis properly: Manual spreadsheet or use QuantWheel for automation

- Integrate into wheel strategy: Rolling is position management within broader wheel cycle

The most successful wheel traders treat rolling as a repeatable process, not a reaction to fear or greed. They have clear rules, calculate expected value for each decision, and track results to continuously improve.

The difference between amateur and professional wheel traders isn’t intelligence – it’s systematic process and efficient execution. Amateurs spend 30 minutes analyzing each roll and still miss opportunities. Professionals use tools like QuantWheel to analyze in seconds and execute confidently.

If you’re managing 5+ wheel positions and spending hours each week on rolling decisions, cost basis tracking, and position management, QuantWheel eliminates 80% of that work while improving your decision quality.

Start your free trial of QuantWheel →

Start with your next rolling decision. Instead of manually checking strikes and calculating net credits, see how QuantWheel’s Roll Assistant analyzes every option and identifies the optimal roll in 15 seconds. Your time is worth more than spreadsheet maintenance.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.