Author: David Romic – retail options trader and active member in the options trading communities on Reddit (u/thedavidromic).

I share wheel strategy setups, trade management, and lessons learned from real positions.

TL;DR: Rolling Cash Secured Puts

-

If you’d do “panic rolling”, your position was wrong from the start — rolling panic means you were never truly fine with owning the stock at that strike; fix that before the next entry, not during.

-

Deep ITM rolls are mostly moving losses around, not earning premium — once your put is deep ITM and vol drops, any “credit” you collect is near-zero extrinsic; you’re not actually generating new income.

-

Rolling doesn’t have to be on the same stock — it’s just redeploying collateral, so ask if this is still the best use of that capital before defaulting back to the same ticker.

-

Always run the CC math before rolling — check what a covered call at a good strike would pay if you just took assignment of a CSP; it often beats the roll credit by a wide margin.

-

Never roll for a net debit — if a credit roll isn’t possible, rolling is no longer a tool you have available; the position needs to be closed or assigned, not extended at a cost.

-

Your breakeven didn’t reset when you rolled — the new put’s strike is not your real cost basis; subtract all prior booked losses from the new position’s “win” before declaring success.

-

Check if your theta goes up or down after the roll — rolling deeper ITM or far out in time can actually slow your daily decay rate, meaning the new contract earns premium more slowly than waiting would have.

-

Rolling down locks in more short-vol exposure during drops — each downward roll feels safer but compounds your vulnerability to continued decline; only do it if your thesis on the stock is unchanged.

When to roll: Roll when you’re down 20-25% on your position, can collect a net credit, and still want the stock at your adjusted cost basis. (these are

How to roll: Simultaneously buy-to-close your current put and sell-to-open a new put. Most traders roll out 2-4 weeks (same strike) rather than changing the strike.

Cost basis calculation: New effective strike = (Original Strike – Original Premium – Roll Credits + Roll Debits). Each roll credit lowers your breakeven point.

When NOT to roll: If fundamentals have deteriorated, if you can’t roll for a credit, or if you’ve rolled 3+ times and the stock keeps declining. Sometimes taking the loss is smarter than throwing good money after bad.

Understanding Cash-Secured Put Rolls

Rolling is not a magic fix for losing trades. It’s a tactical decision to extend time on a position when you still believe in the underlying stock and can do so profitably.

Rolling for a Credit vs Rolling for a Debit

Rolling for a credit (the goal):

- Premium received from new put > Cost to close old put

- Net credit reduces your effective strike price

- Example: Pay $300 to close, receive $450 for new put = $150 credit

- Your breakeven just improved by $1.50 per share

Rolling for a debit (generally avoid):

- Premium received from new put < Cost to close old put

- Net debit increases your effective strike price

- Example: Pay $300 to close, receive $250 for new put = $50 debit

- Your breakeven just worsened by $0.50 per share

Most experienced wheel traders follow this rule: Only roll if you can collect a net credit.

Rolling for a debit means you’re paying extra to delay a losing decision, which rarely works out well.

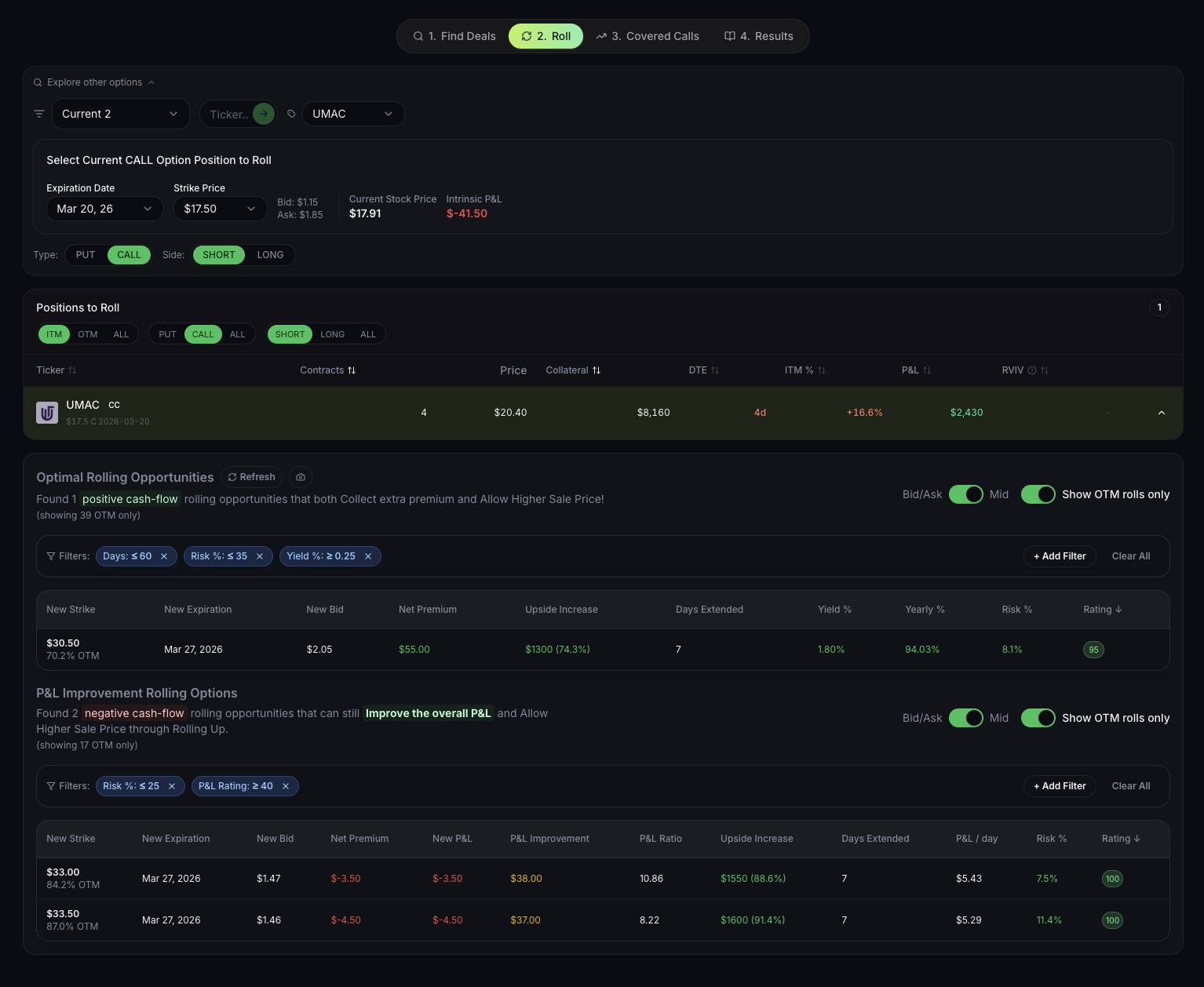

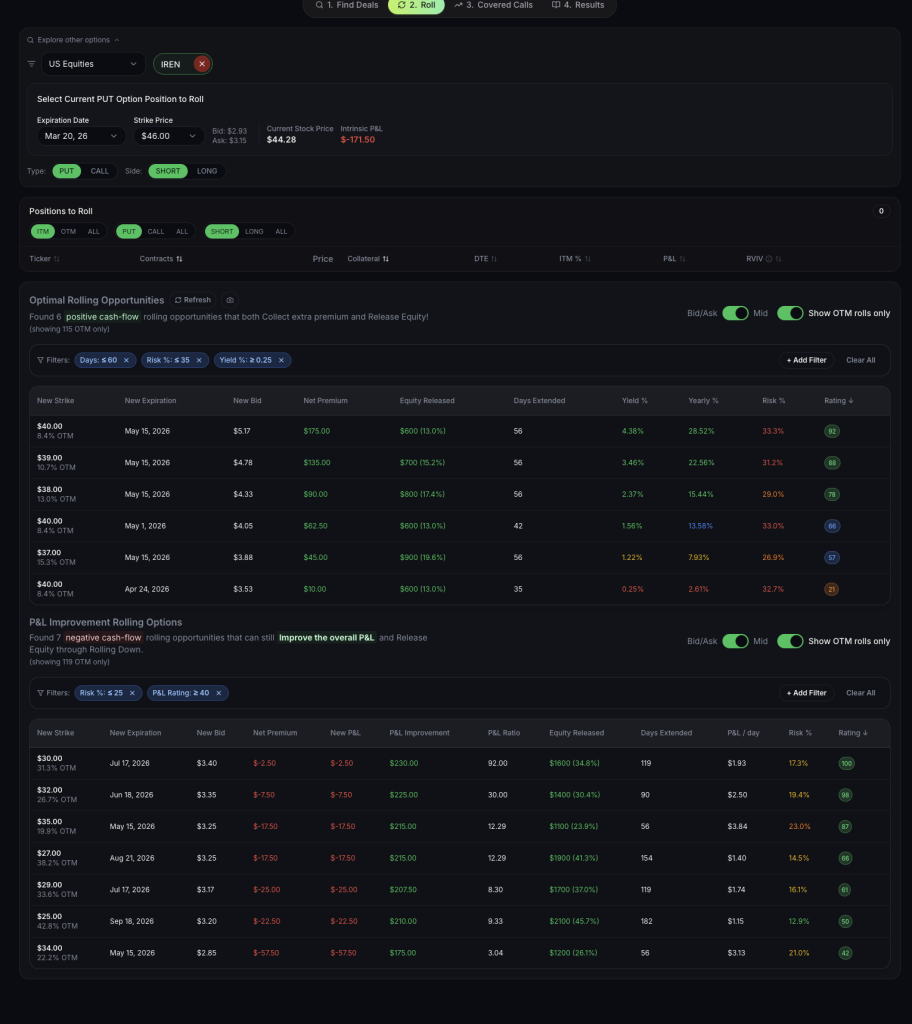

Example trade: IREN $46 CSP with 3 days left until expiration.

Current stock price: $44.28

You can see the available rolling opportunities below:

The solution: First ranked opportunity under “optimal rolling opportunities” or under “P&L Improvement rolling options” – depends on what suits your liking and situation the best.

Find rolls like this for your positions →

The Three Types of Rolls

- Roll out (time roll): Same strike, later expiration

- Most common roll for wheel traders

- Maximizes premium collection

- Gives stock time to recover

- Example: $50 put expiring this Friday → $50 put expiring next month

- Roll down (strike roll): Lower strike, same expiration

— Defensive move that lowers your obligation price.

— Almost always done for a net debit (you pay to roll).

— Only worth it if you’re genuinely convinced the stock will recover to the new, lower strike. - Roll out and down: Lower strike AND later expiration

- Combination strategy

- Reduces risk while adding time

- Usually collects solid credit

- Example: $50 put expiring Friday → $49 put expiring next month

Each type serves different goals.

When to Roll Cash-Secured Puts

The decision to roll isn’t arbitrary. It should follow a systematic framework based on your position’s profit/loss, time to expiration, and your conviction about the underlying stock.

Rule 1: Roll When Down 20-25%

Most wheel traders set a threshold for when to consider rolling: typically when a position is down 20-25% of the premium collected.

Example calculation:

- You sold a put for $2.00 ($200 premium)

- Position is now worth $2.50 (down $50, or 25%)

- This triggers your “consider rolling” threshold

Why 20-25%? Because this is the point where:

- The position is clearly losing but not catastrophic

- Time decay hasn’t completely evaporated

- Rolling for a credit is still usually possible

- The stock hasn’t moved so far that fundamentals are likely broken

If you wait until you’re down 50% or more, rolling for a credit becomes much harder because you’re paying significantly more to close while receiving less premium for the new put (since the stock has fallen further).

Rule 2: Roll When You Can Collect a Credit

This is non-negotiable for most profitable wheel traders. The roll must generate a net credit—meaning you receive more premium from the new put than you pay to close the old one.

How to check before rolling:

- Look at the cost to buy-to-close your current put

- Look at the premium available for your target new put

- Calculate: New premium – Close cost = Net credit/debit

- Only roll if the result is a credit

Example:

- Current put (expiring in 7 days): $2.80 to close

- New put (expiring in 35 days): $4.20 to open

- Net credit: $4.20 – $2.80 = $1.40 credit ✓ Good roll

If you can’t roll for a credit, you have three options:

- Wait a few more days (time decay might improve the math)

- Accept assignment (if you want the stock)

- Close for a loss (if you no longer want the stock)

Rule 3: Roll When You Still Want the Stock

This is the most important rule. Rolling extends your commitment to potentially owning the stock. Ask yourself:

- Do I still want to own this stock at my adjusted cost basis?

- Have the fundamentals changed since I opened this position?

- Would I enter this trade today at the current price?

If you answered “no” to any of these questions, rolling is probably the wrong decision. You’re just delaying the inevitable loss and tying up capital that could be used elsewhere.

Red flags that suggest you should NOT roll:

- Company reported terrible earnings

- Sector rotation away from this industry

- Technical breakdown below major support

- You need the capital for a better opportunity

- You’ve already rolled this position 2-3 times

Rule 4: Roll Before Expiration (Not On Expiration Day)

Many beginners make the mistake of waiting until expiration day to decide whether to roll. This is a tactical error because:

- Time value has evaporated: Options on expiration day are mostly intrinsic value, giving you less premium to work with

- Bid-ask spreads widen: Liquidity decreases as market makers prepare for expiration

- Assignment risk is immediate: You could get assigned before you execute the roll

Best practice: Evaluate rolling opportunities 5-10 days before expiration. This is when:

- Time value is still present in both puts

- You can roll out 3-4 weeks and collect meaningful premium

- Bid-ask spreads are tighter

- You have time to think, not panic

When Rolling Makes Perfect Sense

Let’s walk through a scenario where rolling is clearly the right decision:

Situation:

- You sold a $100 put on a quality stock, collected $3 premium

- Stock is now at $98 (slightly ITM)

- 7 days to expiration

- Put is now worth $2.50 (down 0.50, or 17%)

- You still believe in the stock long-term

- Earnings are not for another 45 days

Rolling analysis:

- Close current put: Pay $2.50

- Open new put (30 DTE, same $100 strike): Receive $4.00

- Net credit: $4.00 – $2.50 = $1.50 ✓

New effective cost basis:

- Original: $100 – $3 = $97

- After roll: $97 – $1.50 = $95.50

Decision: Roll. You improved your breakeven by $1.50, gave the stock 30 days to recover, and you’re still confident in the underlying. This is a textbook good roll.

How to Execute a Cash-Secured Put Roll

Now that you know when to roll, let’s cover the mechanics of actually executing the roll on your broker platform.

Step 1: Analyze Your Current Position

Before doing anything, gather this information:

- Current strike price

- Current expiration date

- Original premium collected

- Current value of the put (mark price)

- Current profit/loss (original premium – current value)

- Days to expiration

Most of this is visible in your broker’s position screen. Write it down or screenshot it—you’ll need these numbers to evaluate rolling options.

Step 2: Identify Rolling Candidates

Now scan for potential rolls. You’re looking for puts that meet these criteria:

- Expiration: 2-4 weeks later than your current put

- Strike: Same as your current (most common) or slightly higher

- Premium: Enough to cover your close cost plus generate a credit

Pro tip: Most brokers have a “roll” function that automatically shows you roll options. On ThinkorSwim, right-click your position and select “Create Rolling Order.” On Tastyworks, click “Roll” next to the position.

Step 3: Calculate the Net Credit/Debit

For each roll candidate, calculate:

Net Credit = (New Put Premium) – (Cost to Close Current Put)

Make this calculation for several options:

Option A: Roll out 2 weeks (same strike)

- Close current: $2.50

- Open new: $3.80

- Net: $1.30 credit

Option B: Roll out 4 weeks (same strike)

- Close current: $2.50

- Open new: $4.50

- Net: $2.00 credit

Option C: Roll out 2 weeks (+$5 higher strike)

- Close current: $2.50

- Open new: $3.00

- Net: $0.50 credit

In this example, Option B (roll out 4 weeks) gives you the best net credit. But is it worth tying up your capital for 4 weeks versus 2 weeks? This is where annualized return calculations help.

Step 4: Compare Annualized Returns

To compare rolls with different time frames fairly, calculate the annualized return:

Annualized Return = (Net Credit / Capital at Risk) × (365 / Days Added)

Example:

- Capital at risk: $10,000 (for a $100 strike)

- Option B net credit: $200

- Days added: 28

Calculation:

- ($200 / $10,000) × (365 / 28)

- = 0.02 × 13.04

- = 26% annualized return

Compare this to the annualized return of other options. Sometimes a 2-week roll with a smaller credit actually generates a better annualized return than a 4-week roll with a larger credit.

This is exactly the kind of tedious math that wheel traders hate doing manually. Platforms like QuantWheel automatically calculate the annualized return for every possible roll, showing you which option optimizes for your goals—whether that’s maximum premium, shortest time, or best risk-adjusted return.

Step 5: Execute the Roll

Once you’ve chosen your roll, enter it as a single spread order (not two separate orders). Here’s how on major platforms:

ThinkorSwim:

- Right-click your put position

- Select “Create Rolling Order”

- Choose your new strike and expiration

- Adjust the credit to your target (between the bid and ask)

- Submit as a limit order

Tastyworks:

- Click “Roll” next to your position

- Select new expiration and strike

- Set your minimum credit

- Submit order

Robinhood:

- Robinhood doesn’t have a native “roll” function

- You must close the old position and open the new one separately

- This can result in worse fills—consider using a limit order for each leg

Pro tip: Don’t take the mid-price automatically. Start your roll order at a slightly better credit (closer to the ask for the new put, closer to the bid for closing the old put). You can often get filled at a better price than the mid-price, especially on liquid stocks.

Step 6: Track Your New Cost Basis

Here’s where most traders make a critical mistake: they don’t track their adjusted cost basis after rolling. Your broker won’t do this for you. After rolling, your effective strike price has changed.

Cost basis formula after rolling:

New Cost Basis = Original Strike – Original Premium – Sum of All Roll Credits

Example:

- Original: Sold $100 put for $3 (basis: $97)

- Roll 1: Collected $1.50 credit (basis: $95.50)

- Roll 2: Collected $1.00 credit (basis: $94.50)

If you get assigned on this put, you’ll pay $100 per share, but your real cost basis is $94.50 per share after accounting for all premiums collected. This is critical for:

- Tax reporting (cost basis affects capital gains)

- Position management (knowing your real breakeven)

- Profitability tracking (calculating actual returns)

Most wheel traders track this in a spreadsheet. Every roll means updating the spreadsheet. After three or four rolls, the accounting becomes a nightmare. This is exactly why tools like QuantWheel exist—it automatically adjusts your cost basis when you roll, giving you accurate breakeven calculations at all times without manual spreadsheet updates.

Strike Selection When Rolling Puts

When rolling, you need to decide: same strike, or different strike? This decision affects your risk, reward, and probability of assignment.

Rolling to the Same Strike (Most Common)

Why wheel traders prefer this:

- Maximizes premium collection (lower strikes = more premium)

- Maintains your original target entry price

- Simplest to track cost basis

- Best when you still believe in the stock at this price

When to use:

- Stock fundamentals haven’t changed

- You’re happy to own at the original strike

- You want maximum premium per roll

- Stock is only slightly ITM or still OTM

Example:

- Original: $50 put, collected $2

- Stock now: $49

- Roll: Close $50, open new $50 put 30 days out for $4

- Net credit: $2

- New basis: $46

Rolling to a Higher Strike (More Conservative)

Why some traders do this:

- Reduces assignment risk

- Works when confidence in the stock has decreased slightly

- Gives more upside buffer

- Useful after a gap down

Trade-off:

- Collects less premium

- May result in a smaller net credit

- Can still be assigned if stock continues falling

When to use:

- Stock fundamentals slightly weakened but aren’t broken

- You want to own at a better price

- Recent volatility makes you nervous

- Stock gapped down significantly

Example:

- Original: $50 put, collected $2

- Stock now: $47 (ouch)

- Roll: Close $50, open new $52 put 30 days out for $5

- Net credit: $3

- New basis: $47 ($52 strike – $5 total premium)

Rolling up reduces your assignment risk but also reduces the premium advantage you get from rolling.

Rolling to a Lower Strike (Rare, Aggressive)

This is uncommon and risky. You would only roll to a lower strike if:

- You’re extremely bullish on the stock

- The stock has fallen significantly but you believe it will recover

- You want to maximize the roll credit

- You’re willing to get assigned at an even lower price

Most wheel traders avoid rolling down. It increases your risk and commits you to buying at a lower price, which may no longer align with your original thesis.

Strike Selection Framework

Use this simple decision tree:

- Stock fundamentals unchanged? → Roll to same strike

- Slightly less confident but still want the stock? → Roll up $2-5

- Fundamentals deteriorated significantly? → Don’t roll, close or accept assignment

- Extremely bullish and stock oversold? → Roll to same strike or (rarely) roll down

Most rolls (80%+) in the wheel strategy are to the same strike, extended in time.

Expiration Selection: How Far Out to Roll

Once you’ve chosen your strike, you need to decide how much time to add. This is a critical decision that affects your premium, flexibility, and capital efficiency.

The 2-4 Week Sweet Spot

Most wheel traders roll out 2-4 weeks (14-28 days) for these reasons:

Why 2-4 weeks works:

- Balances premium collection with flexibility

- Gives the stock reasonable time to recover

- Doesn’t tie up capital for too long

- Allows re-evaluation monthly

- Time decay (theta) is still strong in this range

Premium example (stock at $100, $100 strike put):

- 1 week out: $1.50

- 2 weeks out: $2.20

- 4 weeks out: $3.50

- 8 weeks out: $5.00

Notice that doubling the time doesn’t double the premium (due to square root rule of options pricing). The 2-4 week range offers the best premium-per-day ratio.

When to Roll 1 Week (Short-Term Roll)

Use case:

- Stock is very close to being OTM again

- You think short-term catalyst will help (earnings, news)

- You want to preserve flexibility

- You’re less confident in long-term outlook

Trade-off:

- Less premium collected

- More frequent management required

- Higher transaction costs (more rolls = more commissions)

When to Roll 4-8 Weeks (Long-Term Roll)

Use case:

- High conviction on the stock long-term

- Stock needs significant time to recover

- Want to minimize management frequency

- Comfortable locking up capital longer

Trade-off:

- Capital tied up longer

- Less flexibility to exit if fundamentals change

- Opportunity cost (capital can’t be deployed elsewhere)

The Math: Comparing Roll Options

Let’s compare three rolling options with real numbers:

Scenario: $100 put, currently worth $3.50, 5 days to expiration

Option A: Roll 1 week

- Premium: $4.00

- Net credit: $0.50

- Annualized return: ~26%

- Management frequency: Weekly

Option B: Roll 4 weeks

- Premium: $5.50

- Net credit: $2.00

- Annualized return: ~18%

- Management frequency: Monthly

Option C: Roll 8 weeks

- Premium: $7.00

- Net credit: $3.50

- Annualized return: ~16%

- Management frequency: Bi-monthly

Option A has the highest annualized return but requires weekly management. Option B balances return with reasonable management. Option C maximizes total credit but has lower annualized return and ties up capital longest.

Most wheel traders choose Option B (the 4-week roll). It’s the Goldilocks zone: not too short, not too long, just right.

Cost Basis Tracking After Multiple Rolls

This is where the wheel strategy gets complex and where most traders lose track of their real profitability. Let’s walk through a realistic example with multiple rolls.

Example: Three Rolls on the Same Position

Week 1: Initial trade

- Sell $50 put, collect $2.00

- Effective cost basis: $48.00

Week 4: First roll

- Stock at $48.50

- Close original put: Pay $2.50

- Open new $50 put (30 DTE): Receive $4.00

- Net credit: $1.50

- New effective cost basis: $46.50 ($50 – $2 – $1.50)

Week 8: Second roll

- Stock at $47.00

- Close previous put: Pay $3.20

- Open new $50 put (30 DTE): Receive $4.50

- Net credit: $1.30

- New effective cost basis: $45.20 ($50 – $2 – $1.50 – $1.30)

Week 12: Third roll

- Stock at $46.50

- Close previous put: Pay $3.60

- Open new $50 put (30 DTE): Receive $4.80

- Net credit: $1.20

- New effective cost basis: $44.00 ($50 – $2 – $1.50 – $1.30 – $1.20)

Week 16: Assignment

- Stock at $49.00 at expiration

- Put expires ITM, you’re assigned

- You buy stock at $50 (strike price)

- But your real cost basis is $44.00

- Stock is trading at $49.00

- Immediate unrealized gain: $5.00 per share ($500 per contract)

The Tracking Problem

Notice what happened: You were “assigned” at $50, which looks like you bought at the current market price of $49 and immediately lost money. But because you collected $6.00 in total premiums across the original trade and three rolls, your real cost basis is $44.00—a $5 per share profit even though you got assigned ITM.

Your broker shows:

- Stock purchase price: $50.00

- Current stock price: $49.00

- P&L: -$1.00 per share ❌ WRONG

Your real position:

- Effective cost basis: $44.00

- Current stock price: $49.00

- P&L: +$5.00 per share ✓ CORRECT

If you don’t track your real cost basis through multiple rolls, you’ll have no idea whether you’re actually profitable. This is especially critical for:

- Tax reporting: Your cost basis affects capital gains/losses

- Covered call strikes: Selling calls above your effective basis captures all profits

- Exit decisions: Knowing your real breakeven helps you decide when to exit

Here’s where most wheel traders struggle: calculating this manually through multiple rolls becomes tedious and error-prone. You need to track:

- Original premium

- Each roll credit/debit

- Days in each position

- Actual strike prices

Miss one roll credit in your spreadsheet, and your cost basis is wrong for the rest of the position’s life. This is exactly the problem QuantWheel solves—it automatically adjusts your cost basis on every roll, showing your true breakeven at all times without any manual calculations or spreadsheet updates.

When NOT to Roll Cash-Secured Puts

Rolling isn’t always the right answer. Sometimes the best decision is to take the loss, accept assignment, or do nothing. Let’s cover when rolling is a mistake.

Red Flag 1: You’ve Rolled 3+ Times

If you’ve already rolled a position three or more times, the stock is telling you something: it wants to go lower. At some point, you’re not “managing a position”—you’re refusing to accept a bad trade.

Ask yourself:

- Is this stock in a long-term downtrend?

- Have I been rolling for 2-3 months?

- Am I rolling because I believe in recovery or because I’m avoiding a loss?

Reality check: If you’ve rolled three times and the stock keeps declining, your thesis was probably wrong. Accepting the loss or assignment and moving on is often better than rolling a fourth time.

Exception: If the overall market crashed (like March 2020 or October 2022) and your fundamentally strong stock got dragged down with everything else, continuing to roll may make sense. But be honest about whether it’s a market issue or a stock-specific issue.

Red Flag 2: Fundamentals Have Deteriorated

Rolling makes sense when the stock is temporarily down but fundamentals remain intact. But if the underlying business has weakened significantly, rolling is just delaying a bad decision.

Signs fundamentals have deteriorated:

- Earnings miss with lowered guidance

- Major product failure or recall

- Loss of key customers or contracts

- Management changes or scandal

- Sector rotation away from the industry

- Credit rating downgrade

Example: You’re wheeling a tech stock that just reported terrible earnings, missed revenue by 20%, and guided down for the next two quarters. The stock drops 30%. Should you roll your ITM put?

No. The market is repricing the stock based on new information. Rolling means you’re committing to owning it at a price that no longer reflects its value. Take the assignment, immediately sell the stock, and move on—or close the put for a loss if you really don’t want it.

Red Flag 3: You Can’t Roll for a Credit

If you can’t collect a net credit when rolling, you’re essentially paying extra to extend a losing position. This rarely works out well.

Why rolling for a debit is bad:

- You’re increasing your cost basis

- You’re paying for time, not collecting premium

- The math only works if the stock bounces back significantly

- You’re violating the core principle of premium collection

What to do instead:

- Wait a few more days to see if time decay improves the credit

- Accept assignment if you want the stock

- Close the position for a loss if you don’t want the stock

Exception: If you’re 1-2 days from expiration and rolling for a small debit (less than $0.10 per share) saves you from immediate assignment you definitely don’t want, the small debit may be worth it. But this should be rare.

Red Flag 4: Better Opportunities Exist

Every dollar tied up in a rolled position is a dollar that can’t be deployed elsewhere. If you see significantly better opportunities in other stocks, closing your position and moving capital may be smarter.

Opportunity cost example:

- Current position: Rolled 2x, down 15%, marginal roll credit available

- New opportunity: High IV stock with 20%+ annual return potential

Staying in the old position out of stubbornness costs you the better opportunity. Take the loss, free up the capital, and redeploy it where the returns are better.

Red Flag 5: You Need the Capital

If you need the capital for an emergency, better opportunity, or simply to reduce exposure, don’t roll just to avoid a loss. Accept the assignment or close the position. Your psychological need to “not lose” on a trade shouldn’t override rational capital management.

When Accepting Assignment Is Better Than Rolling

Sometimes assignment is actually the better outcome:

Assignment makes sense when:

- Stock is fundamentally strong and temporarily down

- You have capital available to hold the stock

- Your effective cost basis is good after rolling credits

- You can sell covered calls immediately to continue collecting premium

- The stock pays dividends (you’ll collect while holding)

Example: You’ve been wheeling a quality dividend stock. After one roll, your effective cost basis is $45. Stock is at $47, but your put strike is $50. You get assigned.

Result:

- You buy at $50 but real basis is $45

- Stock is at $47 (unrealized $2 gain)

- Stock pays 3% dividend ($1.50/year)

- You immediately sell a $50 covered call for $3

- If called away at $50, you profit $5 + $3 call premium = $8 per share profit

- If not called away, you keep collecting premium and dividends

This is the wheel strategy working exactly as intended. Assignment isn’t a failure—it’s part of the plan.

Advanced Rolling Strategies

Once you’ve mastered basic rolling, these advanced techniques can optimize your results.

The Defensive Roll: Rolling Up and Out

When you’re less confident in a stock but don’t want to close it entirely, roll both to a higher strike AND later expiration.

Advantages:

- Reduces assignment risk (higher strike)

- Adds time for recovery (later expiration)

- Can still generate a credit

- Gives you flexibility to re-evaluate

Example:

- Original: $100 put, stock now at $96

- Roll: Close $100 put, open $102 put (4 weeks out)

- Why: You still like the stock but want less downside risk

- Result: Higher strike = less likely to be assigned, more time to recover

The Aggressive Roll: Rolling Down

Very rare, but occasionally used by extremely bullish traders when a quality stock has been oversold.

When to consider:

- Stock dropped on temporary news, fundamentals intact

- You’re very confident in short-term recovery

- Rolling down still generates a solid credit

- You want even more exposure at lower prices

Example:

- Original: $50 put, stock now at $45

- Roll: Close $50 put, open $48 put (4 weeks out)

- Why: You think $45 is a temporary bottom, want to own more at $48

- Risk: If wrong, you’ve committed to buying at a lower price

Warning: This is advanced and risky. Most wheel traders should avoid rolling down unless they’re very experienced and very bullish.

The “Rescue” Roll: Multiple Rolls to Eventual Profit

Sometimes a well-executed series of rolls can rescue a badly losing position. This only works if the stock eventually recovers and you have patience.

Real example:

- Week 1: Sell $60 put, collect $3 (basis: $57)

- Week 4: Stock at $55, roll for $2 credit (basis: $55)

- Week 8: Stock at $53, roll for $1.50 credit (basis: $53.50)

- Week 12: Stock at $52, roll for $1.50 credit (basis: $52)

- Week 16: Stock at $55, close put for $5 profit

- Total profit: $8 per share across 4 months

The key: the stock eventually recovered. If it hadn’t, you’d have been assigned at $60 with an effective cost basis of $52—still a reasonable outcome if the stock is fundamentally sound.

The Calendar Roll: Mixing Expirations

Some traders get creative with expiration timing, mixing weekly and monthly options depending on market conditions.

Weekly rolls:

- Use when very close to being OTM again

- Provides flexibility

- Lower premium but more frequent management

Monthly rolls:

- Use when stock needs significant time to recover

- Maximizes premium per roll

- Less management but less flexibility

Strategy:

- Start with weekly rolls if close to breakeven

- If stock isn’t recovering, extend to monthly rolls

- Mix based on market conditions and stock price action

Tools and Calculators for Rolling

The math for rolling—especially comparing multiple options—gets tedious quickly. Here are approaches traders use.

Manual Spreadsheet Tracking

Pros:

- Complete control

- Customizable to your needs

- Free

Cons:

- Time-consuming to maintain

- Easy to make errors

- Doesn’t sync with broker

- No real-time data

Typical spreadsheet columns:

- Date

- Action (BTC/STO)

- Strike

- Expiration

- Premium

- Net credit/debit

- Running cost basis

After three or four rolls, your spreadsheet has 10-15 rows for a single position. Multiply this by 10-15 positions, and you’re spending hours per week on spreadsheet accounting.

Broker Built-In Tools

Most brokers show you roll options, but they don’t:

- Calculate your cumulative cost basis

- Compare multiple roll scenarios side-by-side

- Track roll history across multiple transactions

- Show annualized returns for different rolls

ThinkorSwim has the best broker tools (roll suggestions, projected P&L), but it’s still not designed specifically for wheel traders managing multiple positions through rolling cycles.

Professional Wheel Strategy Platforms

This is where dedicated platforms shine. A tool like QuantWheel is built specifically for wheel traders and handles:

Automatic cost basis tracking:

- Updates your effective strike after every roll

- Tracks cumulative premiums collected

- Shows your real breakeven at all times

Roll comparison:

- Analyzes all possible rolls (different strikes and expirations)

- Calculates net credit, annualized return, and probability of profit

- Recommends optimal roll based on your goals

Position history:

- Tracks every roll in your position’s lifecycle

- Shows total premiums collected

- Displays time in trade and overall performance

Alerts:

- Notifies you when positions hit your roll threshold (e.g., down 20%)

- Reminds you when expirations are approaching

- Flags when good rolling opportunities appear

The value proposition: Stop spending hours in spreadsheets calculating cost basis and comparing roll options. Automated platforms do it instantly, letting you focus on the actual trading decisions rather than the accounting.

For traders managing 10+ positions with regular rolls, the time savings alone justifies the cost of a professional tool. The improved accuracy in cost basis tracking prevents costly tax mistakes and ensures you know your real profitability.

Real Example: Rolling Through a Market Downturn

Let’s walk through a realistic scenario showing how rolling can work (and when it doesn’t).

The Setup

March 1: You sell a $150 put on a high-quality tech stock, collecting $6 premium. Your effective cost basis is $144. The stock is trading at $155, and you’re confident in the fundamentals.

March 15: Stock drops to $148 on market-wide tech selloff. Your put is now worth $8 (you’re down $2, or 33%). You decide to roll.

First roll:

- Close $150 put: Pay $8

- Open new $150 put (30 DTE): Receive $11

- Net credit: $3

- New cost basis: $141 ($150 – $6 – $3)

The Test: Multiple Rolls

April 15: Stock drops further to $142 on continued selling. Your put is now worth $9.50. You’re still confident in the company, so you roll again.

Second roll:

- Close $150 put: Pay $9.50

- Open new $150 put (30 DTE): Receive $12

- Net credit: $2.50

- New cost basis: $138.50 ($150 – $6 – $3 – $2.50)

May 15: Stock stabilizes at $145. Your put is worth $5.50. You roll one more time.

Third roll:

- Close $150 put: Pay $5.50

- Open new $150 put (30 DTE): Receive $7

- Net credit: $1.50

- New cost basis: $137 ($150 – $6 – $3 – $2.50 – $1.50)

The Outcome: Two Scenarios

Scenario A: Recovery (Happy Ending)

- June 15: Stock recovers to $152

- Your put expires worthless

- You never get assigned

- Total profit: $13 per share (all premiums collected)

- Time in trade: 3.5 months

- Annualized return: ~35%

Scenario B: Assignment (Still Good)

- June 15: Stock drops to $148, you get assigned

- You buy stock at $150 (strike)

- Your real cost basis is $137

- Stock trading at $148

- Immediate unrealized gain: $11 per share

- You immediately sell covered calls at $150 for $5

- If called away: $13 strike profit + $5 call premium = $18 total profit

Scenario C: Disaster (Bad Ending)

- Fundamentals deteriorate significantly

- Stock drops to $125 and stays there

- You’re assigned at $150, effective basis $137

- Stock at $125 = $12 unrealized loss

- Lesson: Should have stopped rolling after 2nd roll and accepted the loss

The key learning: Rolling works when the stock eventually recovers or stabilizes. It fails when fundamentals have truly broken and the stock enters a long-term downtrend.

Tax Implications of Rolling

Rolling has specific tax implications you need to understand for accurate reporting.

How Rolls Are Taxed

Each roll is two separate transactions for tax purposes:

- Closing the old put = Closes that option position (gain or loss realized)

- Opening the new put = Opens a new option position

Example:

- Original: Sold put for $500 premium

- Roll: Paid $700 to close (realized $200 loss), received $900 for new put

- Tax impact: You realized a $200 loss when you closed the first put

- New position: $900 premium, will be realized when this put closes

Short-Term vs Long-Term

Options are almost always short-term capital gains/losses because they’re rarely held longer than one year. This means:

- Profits are taxed at ordinary income rates (not lower capital gains rates)

- Losses offset other short-term gains or up to $3,000 of ordinary income

Wash Sale Rules

This is where rolling gets complex. The wash sale rule prevents you from claiming a loss if you rebuy a “substantially identical” security within 30 days.

Does rolling trigger wash sale?

Yes, if you close a put at a loss and immediately open a new put on the same stock at the same or similar strike within 30 days, it’s likely a wash sale. This means:

- You can’t immediately deduct the loss

- The loss gets added to the cost basis of the new put

- You can eventually claim it when the new position closes

Example:

- Close $50 put at $200 loss

- Immediately roll to new $50 put

- Loss is disallowed as wash sale

- Loss gets added to new put’s cost basis

Impact: Your taxes get more complicated, but you’ll eventually get the loss deduction. Track this carefully or use software to handle wash sale adjustments.

Cost Basis Reporting

Your broker reports options transactions to the IRS, but they do not track your cumulative adjusted cost basis through rolls. You need to track:

- All premiums collected

- All closing costs paid

- Net credits/debits for each roll

- Final effective cost basis if assigned

When you get assigned and your broker shows a purchase price of $50, but your real cost basis is $45 after three rolls, you are responsible for correctly reporting the $45 basis to the IRS—not the $50 your broker shows.

Recommendation: Keep detailed records or use a platform that exports tax-ready reports showing your true cost basis through all rolls. Getting this wrong can result in overpaying taxes (if you don’t adjust basis correctly) or underpaying (audit risk).

Common Rolling Mistakes to Avoid

After analyzing thousands of rolled positions, here are the most common mistakes wheel traders make.

Mistake 1: Rolling on Expiration Day

Why it’s bad:

- Time value has evaporated

- Bid-ask spreads are wider

- Less premium available

- Rushed decision-making

Fix: Evaluate rolling 7-10 days before expiration. Give yourself time to think and get better pricing.

Mistake 2: Rolling for a Debit

Why it’s bad:

- You’re paying to extend a losing trade

- Increases your effective cost basis

- Violates the principle of premium collection

Fix: Only roll if you can collect a net credit. If you can’t, either accept assignment or close for a loss.

Mistake 3: Rolling Indefinitely on Bad Stocks

Why it’s bad:

- Refusing to accept reality

- Tying up capital in a loser

- Missing better opportunities

Fix: Set a rule: Maximum 3 rolls on any single position. After that, accept assignment or close it out.

Mistake 4: Not Tracking Adjusted Cost Basis

Why it’s bad:

- You don’t know your real breakeven

- Can’t make informed decisions about covered calls

- Tax reporting errors

Fix: Use a spreadsheet or automated platform to track cumulative premiums and your effective strike price through all rolls.

Mistake 5: Rolling Too Early

Why it’s bad:

- Panicking on small losses

- Not giving positions time to work

- Creating unnecessary transaction costs

Fix: Set a threshold (like down 20-25%) before considering a roll. Don’t roll just because a position is slightly losing.

Mistake 6: Ignoring Fundamentals

Why it’s bad:

- Rolling on a stock with deteriorating fundamentals

- Committing to ownership of a bad company

- Losses compound

Fix: Before every roll, ask: “Would I enter this trade today?” If no, don’t roll.

Mistake 7: Rolling Too Far Out in Time

Why it’s bad:

- Ties up capital for months

- Reduces flexibility

- Opportunity cost

Fix: Stick to 2-4 week rolls most of the time. Only roll 6-8 weeks if you have very high conviction and want to minimize management frequency.

QuantWheel’s Rolling Assistant

We built QuantWheel because we got tired of the manual calculations and spreadsheet chaos that comes with rolling multiple positions. Here’s what the platform handles automatically:

Automatic Cost Basis Tracking

Every time you roll a position, QuantWheel:

- Detects the roll automatically via broker sync

- Calculates the net credit/debit

- Updates your effective cost basis

- Shows your new breakeven price

No manual spreadsheet entries. No forgetting to update. Your real cost basis is always visible, accurate, and current.

Roll Comparison Analysis

When considering a roll, QuantWheel shows you:

- All possible roll options (different strikes and expirations)

- Net credit/debit for each option

- Annualized return for each option

- Probability of profit for each option

- Recommended optimal roll based on your goals

Example output:

- Roll to $50 (2 weeks): $150 credit, 28% annualized

- Roll to $50 (4 weeks): $280 credit, 22% annualized

- Roll to $52 (2 weeks): $200 credit, 30% annualized (Recommended)

The platform does all the math instantly, letting you focus on the decision rather than the arithmetic.

Position History & Performance

For every position that’s been rolled, you can see:

- Complete roll history (dates, strikes, expirations, credits)

- Total premiums collected

- Effective cost basis after each roll

- Time in trade

- Overall profitability

This makes it easy to review whether your rolling strategy is actually working or whether you’ve been rolling too much on bad stocks.

Roll Alerts

Set custom alerts to notify you when:

- Position is down X% (your roll threshold)

- Expiration is Y days away (your evaluation window)

- A good rolling opportunity appears based on your criteria

No more constantly checking positions or missing optimal roll timing. The platform watches for you and alerts when action might be needed.

Summary: The Rolling Decision Framework

Here’s your step-by-step framework for deciding whether to roll a cash-secured put:

Step 1: Check Your Roll Threshold

- Is the position down 20-25% or more?

- If yes, proceed to Step 2

- If no, let it run (or use your custom threshold)

Step 2: Verify You Can Roll for a Credit

- Calculate: New premium – Closing cost = Net credit?

- If yes, proceed to Step 3

- If no, don’t roll (unless extraordinary circumstances)

Step 3: Confirm You Still Want the Stock

- Would you enter this trade today at the current price?

- Have fundamentals changed?

- If you still believe in the stock, proceed to Step 4

- If fundamentals have deteriorated, close or accept assignment

Step 4: Compare Rolling Options

- Analyze 2-4 week rolls (same strike)

- Consider 2-4 week rolls (higher strike) if less confident

- Calculate annualized returns for each

- Choose the option that best fits your goals

Step 5: Execute the Roll

- Enter as a single spread order

- Set limit order for desired credit (don’t take mid automatically)

- Confirm fill

- Update your cost basis tracking

Step 6: Monitor and Re-Evaluate

- Set alerts for your next roll threshold

- Review 7-10 days before new expiration

- Limit to 3 rolls maximum per position

- Be ready to accept assignment if fundamentals change

Final Thoughts

Rolling cash-secured puts is one of the most powerful tools in the wheel trader’s arsenal. When used correctly—on fundamentally sound stocks, for net credits, with clear thresholds—it allows you to manage losing positions, improve your cost basis, and often turn what looked like a bad trade into a profitable one.

But rolling is not a magic fix. It doesn’t work on stocks with broken fundamentals. It fails when you roll indefinitely hoping for a miracle recovery. And it becomes a nightmare to track if you’re managing 10-15 positions through multiple rolls without the right tools.

The keys to successful rolling:

- Roll when down 20-25%, not sooner

- Always roll for a credit, never a debit

- Confirm you still want the stock before rolling

- Roll 2-4 weeks out for optimal premium-to-time ratio

- Track your adjusted cost basis after every roll

- Limit to 3 rolls before accepting reality

- Use the right tools to make comparisons and tracking easier

If you’re manually tracking all of this in spreadsheets, you know how tedious it becomes. Professional platforms like QuantWheel automate the cost basis calculations, compare rolling options instantly, and track your complete position history—letting you focus on the actual trading decisions rather than the accounting.

Whether you track manually or use a platform, the important thing is having a systematic approach to rolling. Follow your rules, trust your framework, and accept that some positions will end up assigned no matter how well you roll. That’s part of the wheel strategy, and it’s often where the real profits begin.

Start your free trial of QuantWheel →

Disclaimers

Risk Disclosure: Options trading involves substantial risk and is not suitable for all investors. Rolling cash-secured puts can extend losses if the underlying stock continues to decline. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

Tax Disclaimer: The tax information provided in this article is general in nature and may not apply to your specific situation. Options taxation is complex, especially with wash sale rules and cost basis adjustments. Consult with a qualified tax professional for advice specific to your circumstances.

Not Financial Advice: The strategies, examples, and recommendations in this article are for educational purposes only. The author and QuantWheel are not providing personalized financial advice or recommendations to buy or sell any security. All investment decisions should be based on your own analysis, risk tolerance, and financial situation.