The problem: You sold five cash-secured puts last month and the premium looked great.

Then one stock dropped 20% and you got assigned.

Another dropped 15%.

That is not a strategy problem or a wrong stock pick, it’s just a position sizing problem.

Solution:

A simple yet boring one: risk about 1–5% of your account per underlying, with no more than ~50% of your total buying power tied up in open wheel trades at once.

This goes by saying that you don’t solely gamble by buying options and that you hold some long term investments in your account, run some wheels (sell options) and have a few occasional directional bets.

Author: David Romic – retail options trader and active member in the options trading communities on Reddit (u/thedavidromic).

I share wheel strategy setups, trade management, and lessons learned from real positions.

Position Sizing in Options Trading: What You Need to Know (TLDR)

Here is everything you need to know about position sizing in options trading, explained simply.

Position sizing means deciding how much money to put into each trade. Think of your trading account like a pizza. You cut it into slices, and each slice is one trade. If you make the slices too big, one bad trade eats most of your pizza. If you cut them into reasonable pieces, losing one slice does not ruin dinner.

The simple rule: Never put more than 5% of your total account into a single options trade.

Example: You have $50,000 in your account. Five percent of $50,000 is $2,500. That means you should not risk more than $2,500 on any one position.

For a cash-secured put, you need enough cash to buy 100 shares if assigned. If a stock trades at $45 and you sell a put at the $45 strike, you need $4,500 in cash secured. That is 9% of your $50,000 account — which is too large under the 5% rule for max risk. So you might choose a $25 stock instead, where the $2,500 capital requirement fits perfectly within your limit.

How many positions should you have? Aim for 8 to 20 wheel positions depending on your account size. This gives you diversification without making management impossible.

The one thing that matters most: No single trade should have the power to seriously damage your account. If you follow this principle, you will survive the bad trades and profit from the good ones over time.

What Is Position Sizing and Why It Matters More Than Stock Picking

Position sizing in options trading refers to determining how much of your total capital to allocate to each individual trade.

It is not about which stock to pick or what strike price to choose — it is about how much money you are putting on the line with each decision.

Why this matters:

A study from Van Tharp, one of the most respected trading psychologists, found that position sizing accounts for more of a trader’s long-term success than stock selection or market timing combined.

Conclussion:

You could have a strategy that wins only 50% of the time and still be extremely profitable if your position sizing keeps your winners large enough and your losers small enough.

What not to do:

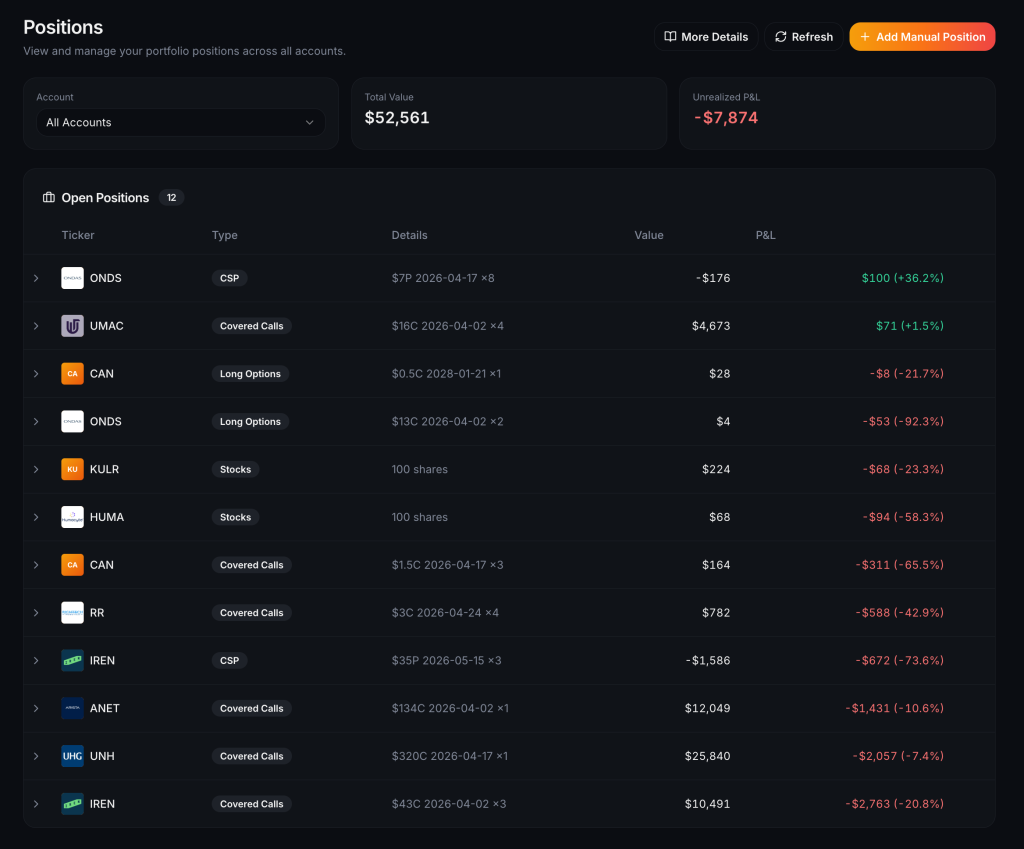

Here you can see that some open positions are 50-70% drawdown which is unacceptable.

Losers need to be cut earlier because the market (S&P500) is down just 3%.

What to do:

Diversify accordingly, pick different sectors, when entering a new stock don’t go all in at once, enter at prices that are reasonable and don’t chase the hype.

These positions might be in drawdown currently but there’s still $200,000 to be allocated out of $52,561 used currently.

The Core Position Sizing Rules for Options Traders

1. Start from account‑level risk

-

Define a max drawdown you can stomach (e.g., 20–30% on the whole account).

-

From that, cap risk per ticker (e.g., 2–5% of net liq if everything goes wrong on that name).

2. Limit allocation per underlying

-

For wheel / CSPs, keep per‑underlying allocation roughly in this range:

-

Conservative: 1–2% of account per short put.

-

Moderate: 3–5% per ticker, scaling only after real track record.

-

-

Hard rule: no single stock should be able to blow up more than your pre‑defined per‑ticker risk if it gaps down badly.

3. Control total “short premium” exposure

-

Set a portfolio cap on premium‑selling strategies:

-

Many experienced traders keep 30–50% of buying power in short options during “normal” volatility.

-

Only push higher in exceptional conditions you fully understand (e.g., post‑event IV crush setups).

-

-

Make sure you can survive a correlated volatility spike (multiple positions moving against you simultaneously).

4. Size by worst‑case, not by premium

-

For CSPs, size as if you’ll absolutely be assigned at the strike and must hold shares through a major drawdown.

-

Ask before entering: “If this stock drops 30–50%, am I okay with that dollar loss and capital tie‑up on this size?”

-

If the honest answer is “no,” reduce contracts or skip the trade.

5. Adjust size to volatility

-

In high IV, keep position size smaller per ticker because gap risk and path risk are larger, even though premium looks juicy.

-

In low IV, you can size slightly larger per ticker (because moves tend to be smaller), but total account risk should still respect your overall rules.

6. Use tiered scaling rules

-

Start new tickers small then scale only after:

-

Surviving a full cycle (several rolls, an assignment, or one earnings event).

-

PnL and behavior match your thesis.

-

-

Example scheme:

-

Tier 1: 1 contract.

-

Tier 2: 2–3 contracts after 2–4 successful cycles.

-

Tier 3: 4–5+ contracts only on your A‑tier, fundamentally strong names.

-

7. Respect correlation and “theme” risk

-

Do not treat 5 semis, 4 SaaS, or 6 fintech names as “diversified.” Correlation means those positions can blow up together.

-

Limit sector or theme exposure (e.g., no more than 15–20% of account in one industry or macro theme).

8. Have explicit “stop adding” rules

-

Define in advance when you stop scaling into losers:

-

After X% drop in the underlying.

-

After N rolls that extend duration without improving break‑even.

-

-

This prevents “rescue sizing” that turns a manageable loss into an account‑threatening one.

9. Align size with time horizon and style

-

Short‑term, high‑frequency options traders usually risk less per trade (e.g., 0.25–1% per position), relying on many small edges.

-

Slower wheel / CSP traders can risk more per name (e.g., 1–5%), but with fewer, higher‑conviction positions and strong fundamental filters.

10. Make it mechanical, not emotional

-

Write your rules as if–then statements, for example:

-

“If account drawdown reaches 10%, then cut new position size by 50% until back above prior equity high.”

-

“If IV rank > 50 and stock passes my fundamentals checklist, then max 3% allocation; if IV rank < 20, then max 1% allocation.”

-

-

The goal is consistency: same inputs ⇒ same size, regardless of how you “feel” about the trade today.

Position Sizing for the Wheel Strategy: A Specific Framework

The wheel strategy has unique position sizing considerations that general options education does not cover. When you run the wheel, your capital flows through different stages — from cash-secured puts to potential assignment to covered calls and back again. Your position sizing must account for this full cycle.

Sizing Cash-Secured Puts

When you sell a cash-secured put, you need enough capital in your account to buy 100 shares at the strike price. This is your capital commitment. Your position size is determined by the strike price you choose.

Here is how to think about it with a $50,000 account and a 5% maximum position size:

- Maximum capital per position: $2,500

- This means you can sell cash-secured puts on stocks trading up to approximately $25 per share (since 100 shares × $25 = $2,500)

But wait — many popular wheel stocks trade well above $25. Stocks like AMD, PLTR, and SOFI might trade between $20 and $180. How do you handle this?

Option 1: Strict adherence. Only wheel stocks that fit within your per-position limit. With a $50,000 account at 5%, that is stocks under $25. This is the most conservative approach.

Option 2: Risk-based sizing. Instead of capping the total capital committed, cap the maximum loss you are willing to take. If you sell a $50 put and collect $2.00 premium, your breakeven is $48. If you set a mental stop at a 20% decline from breakeven ($48 × 0.20 = $9.60), your maximum expected loss is $960. That is under 2% of your $50,000 account. This allows larger nominal positions while keeping risk controlled.

Option 3: Gradual scaling. Start with smaller positions and increase sizing as your account grows. This is the approach many successful wheel traders take over time.

Sizing Covered Calls After Assignment

The key insight here is that your position size does not change just because you moved from cash-secured put to covered call.

You still have the same capital at risk.

What changes is your cost basis.

If you sell a $50 covered call and collect another $1.50 in premium, your adjusted cost basis is now $46.50.

Your actual risk on this position has decreased, which changes the risk calculation for your overall portfolio.

Here is where most traders struggle: calculating your actual cost basis after assignment while selling options.

Your broker shows one number, but your real basis includes all the premium collected through the full wheel cycle.

You need to track this manually across every position.

![]()

Avoid mistakes like this by creating a system to track your portfolio positions →

How Many Wheel Positions Should You Run?

The number of simultaneous positions depends on your account size, your per-position allocation, and how much time you have for management. Here is a general framework based on experience from thousands of wheel traders:

$10,000–$25,000 account: 3–6 positions. You are limited by capital and should focus on lower-priced stocks. Diversification is harder at this level, so be extra conservative with position sizing (closer to 3% per position).

$25,000–$50,000 account: 6–12 positions. This is the range where the wheel strategy starts to work well. You have enough capital for meaningful diversification across sectors. Aim for 4–5% per position.

$50,000–$100,000 account: 10–18 positions. You can now wheel some higher-priced stocks while maintaining diversification. Consider a tiered approach with core positions at 5% and satellite positions at 3%.

$100,000–$500,000 account: 15–25 positions. At this level, you have flexibility to run a well-diversified wheel portfolio. Management becomes the main challenge — tracking 20+ positions in spreadsheets gets difficult fast.

$500,000+ account: 20–30+ positions. Full portfolio diversification is achievable. Professional tracking tools become essential. Many traders at this level also start working with margin for additional positions.

The 5% Rule: Why Most Wheel Traders Swear By It

The 5% rule is the single most referenced position sizing guideline in the wheel strategy community, especially in places like r/thetagang. It is simple: no single position should represent more than 5% of your total portfolio value.

Here is why it works so well for the wheel strategy specifically:

It survives the worst-case scenario. If a stock you are wheeling drops 50% and you have 5% of your portfolio in it, your total portfolio takes a 2.5% hit. Painful, but survivable. If you had 20% in that same position, you would lose 10% of your entire portfolio on one trade.

It forces diversification. At 5% per position, you need at least 20 positions to be fully invested. This naturally spreads your risk across stocks and sectors.

It leaves room for opportunity. When the market sells off and IV spikes — exactly when you want to be selling premium — you still have dry powder if your positions are properly sized.

It accounts for assignment risk. In the wheel strategy, assignment is not a disaster, it is part of the plan. But it does lock up capital. If each position is only 5% of your account, getting assigned on one or two positions does not cripple your ability to continue trading.

It aligns with the wheel philosophy. The wheel strategy is about consistent, boring, profitable income generation. Not home runs. The 5% rule reinforces this conservative approach — it is the position sizing equivalent of the wheel’s core identity.

Some experienced traders adjust the 5% rule based on stock quality. They might allocate up to 7–8% on a blue-chip like Apple or Microsoft while keeping speculative positions at 2–3%. This tiered approach makes mathematical sense, but the key principle remains: no single position should be large enough to cause serious portfolio damage.

Position Sizing by Account Size: Real Examples With Numbers

Abstract rules are helpful, but nothing beats seeing position sizing in options trading applied with real numbers. Here are detailed examples for three common account sizes.

Example 1: The $25,000 Account

Sarah has $25,000 in her brokerage account and wants to start wheeling. She decides on a 5% maximum position size, which gives her $1,250 per position. This limits her to stocks trading around $12.50 or lower for cash-secured puts.

At this price range, Sarah’s available stocks include names like Ford (F), SoFi (SOFI), and Palantir (PLTR) when they trade in the low double digits. She can comfortably run 8–10 positions.

Sarah’s Portfolio Allocation:

- 8 positions × $1,250 = $10,000 committed

- $15,000 in cash reserve (60% cash position)

This 60% cash reserve might seem high, but it gives Sarah room to add positions when IV spikes and keeps her safe if she gets assigned on multiple positions simultaneously.

Monthly Income Target: If Sarah collects an average of 1.5% monthly premium on her committed capital ($10,000), she generates approximately $150 per month. That is 0.6% return on her total account — not glamorous, but conservative and sustainable.

Example 2: The $75,000 Account

Marcus has $75,000 and has been trading the wheel for six months. He uses a tiered position sizing approach:

- Core positions (blue-chips, large-caps): 5% each = $3,750

- Standard positions (mid-caps, good fundamentals): 4% each = $3,000

- Satellite positions (higher IV, slightly riskier): 2.5% each = $1,875

Marcus’s Portfolio Allocation:

- 4 core positions × $3,750 = $15,000

- 6 standard positions × $3,000 = $18,000

- 4 satellite positions × $1,875 = $7,500

- Total committed: $40,500 (54% of account)

- Cash reserve: $34,500 (46% of account)

Marcus can wheel stocks up to $37.50 per share in his core positions, giving him access to many popular wheel stocks. His satellite positions can target higher-IV names for enhanced premium.

Example 3: The $200,000 Account

Priya has $200,000 and runs a full-scale wheel portfolio. She uses the 5% rule strictly, giving her $10,000 per position. This allows her to wheel stocks up to $100 per share.

Priya’s Portfolio Allocation:

- 20 positions × $10,000 = $200,000 maximum committed

- In practice, she keeps 15–18 positions active (75–90% invested)

- Cash reserve: $20,000–$50,000 (10–25%)

Priya’s challenge is not capital — it is management. Tracking 15–18 wheel positions through their full cycles, monitoring cost basis adjustments, tracking premium collected, and watching for roll opportunities across this many positions requires serious organizational tools.

After managing 15+ wheel positions, your spreadsheet becomes a nightmare. Which puts are still open? What is your total premium collected? What is your adjusted cost basis on assigned positions? This is exactly why platforms like QuantWheel exist — built specifically for wheel traders who need to track this without losing their minds.

Sector Diversification: The Position Sizing Rule Everyone Forgets

Position sizing is not just about individual trade size — it is about portfolio-level risk management. One of the most dangerous mistakes in options trading is having proper individual position sizing but terrible sector diversification.

Here is what that looks like: a trader follows the 5% rule perfectly, running 20 positions. But 8 of those positions are in technology stocks, 5 are in semiconductors, and 3 are in software. When the tech sector sells off 15%, over three-quarters of their positions are underwater simultaneously. The individual position sizing was correct, but the concentration risk was catastrophic.

The sector rule: No more than 20–25% of your total capital should be in any single sector.

For a 20-position portfolio, this means no more than 4–5 positions in the same sector. Here is a diversified wheel portfolio framework:

- Technology: 4–5 positions (20–25%)

- Financials: 3–4 positions (15–20%)

- Healthcare: 2–3 positions (10–15%)

- Consumer: 2–3 positions (10–15%)

- Energy: 2–3 positions (10–15%)

- Industrials: 2–3 positions (10–15%)

- Other sectors: 1–2 positions (5–10%)

This ensures that a sector-wide selloff affects only a portion of your portfolio. Even if every technology stock in your portfolio drops 20%, you lose a maximum of 5% of your total account value (25% allocation × 20% decline = 5% total impact).

When building a diversified wheel portfolio at this scale, a portfolio dashboard that shows aggregate metrics across all your positions — sector allocation, total exposure, premium collected — becomes extremely valuable. Many traders at this level find that spreadsheets simply cannot handle the complexity of tracking sector concentration alongside individual position metrics.

How to Adjust Position Sizing for Volatility

Not all market environments are created equal. Position sizing in options trading should adapt to market conditions, particularly implied volatility levels.

High Volatility Environments (VIX Above 25)

When the VIX is elevated and implied volatility is high across the market, premiums are rich. This is when selling puts and calls is most profitable per trade. But it is also when stocks move the most violently.

The adjustment: Reduce individual position sizes by 20–30% and increase your number of positions. Instead of 5% per position, drop to 3–3.5%. Instead of 15 positions, run 20–25.

Why? Because high IV means higher probability of large moves. Your premium collected is higher, but so is your risk of assignment at unfavorable prices. Smaller positions and broader diversification protect you during the volatile moves while still capturing enhanced premium.

Low Volatility Environments (VIX Below 15)

When the VIX is low, premiums are thin. Each individual trade generates less income. Some traders respond by increasing position size to compensate — this is a mistake.

The correct adjustment: Keep position sizes the same or reduce them slightly. Accept that low-volatility periods will generate less income. The alternative — increasing position sizes to maintain income targets — is how accounts blow up when volatility inevitably returns.

What you can do in low-volatility environments is adjust your strategy rather than your position sizing. Consider shorter expirations (weekly instead of monthly), slightly higher deltas (to compensate for lower premiums), or simply sitting on more cash and waiting for better opportunities. Never compromise your position sizing rules to chase income.

Earnings Season Adjustments

Earnings announcements create stock-specific volatility events. Many wheel traders avoid selling puts just before earnings, while others specifically target the elevated IV around earnings season.

If you choose to trade around earnings, reduce your position size for those specific trades. A standard 5% position might drop to 2–3% for a pre-earnings put sale. The IV crush after earnings can generate excellent returns, but the binary nature of earnings events means the position deserves less capital allocation.

The Margin Trap: Position Sizing Mistakes That Blow Up Accounts

The most dangerous position sizing error in options trading is not about being too conservative — it is about using margin without adjusting your mental model.

Many brokers allow you to sell cash-secured puts using margin. This means your $50,000 account might have $100,000 in buying power. Some traders see this doubled buying power and immediately double their position count or size. This is how accounts get destroyed.

Here is why margin changes the position sizing equation:

Without margin: You sell a $50 put with $5,000 cash in your account. If the stock goes to zero, you lose $5,000 (minus premium). Your account goes to zero.

With margin: You sell a $50 put using only $2,500 of margin. If the stock drops significantly, your broker issues a margin call. You must either add cash or liquidate positions at the worst possible time — when the market is down. This forced selling locks in losses and can cascade across your entire portfolio.

The position sizing rule for margin: Size your positions based on the full capital commitment (as if cash-secured), NOT based on the reduced margin requirement. If you would need $5,000 to be fully cash-secured, allocate $5,000 of your mental capital budget even if your broker only requires $2,500 in margin.

Some experienced traders use margin selectively and carefully, but this should only happen after years of experience and with strict rules in place. For most wheel strategy traders, treating every position as fully cash-secured is the safest approach to position sizing.

Position Sizing and the Psychology of Trading

Position sizing in options trading is as much about psychology as it is about math. When your positions are too large, every tick of the market feels like a life-or-death event. When they are properly sized, you can watch a 10% drawdown in one position and calmly evaluate whether to roll, hold, or take assignment.

The Sleep Test

Here is a simple psychological position sizing test: can you go to sleep at night without checking your positions? If you are waking up at 2 AM to check futures because you are worried about a single put you sold, your position is too large. Proper position sizing means you can genuinely not think about your positions until the next trading day.

The Drawdown Exercise

Before you commit to a position size, do this mental exercise: imagine the stock drops 30% overnight on a catastrophic earnings miss. Calculate your loss. Now multiply that by the number of positions you have. Can your account survive that hit if it happened to your two worst positions simultaneously?

If the answer is no, your position sizes are too large.

Overconfidence Bias

After a string of winning trades, many traders increase their position sizes. “I have found the formula,” they think. “I should bet bigger.” This is overconfidence bias, and it is the most common psychological position sizing error.

Your position sizing rules should be set in advance and followed mechanically, regardless of recent performance. A winning streak does not change the probability of the next trade. Keep your sizing consistent and let the compounding do the work over time.

Loss Aversion After a Loss

The opposite of overconfidence: after a painful loss, some traders dramatically reduce their position sizes or stop trading entirely. While it is healthy to review what went wrong, cutting your sizing by half because of one bad trade means you are letting emotions override your system.

If your position sizing was correct before the loss, it is still correct after. The loss was not a position sizing failure — it was the expected cost of doing business in options trading. Some trades lose. That is why you size them conservatively in the first place.

Scaling Your Position Sizing as Your Account Grows

One of the most rewarding aspects of the wheel strategy is watching your account compound over time. As your account grows, your position sizing should grow proportionally.

The Rebalancing Schedule

Review and adjust your position sizing every quarter based on your current account value. If your account started at $50,000 with 5% position sizes ($2,500 each) and has grown to $60,000 after six months of premium collection, your new position size should be $3,000.

This quarterly rebalancing ensures your positions scale with your account and you do not become unconsciously over-conservative as your capital grows.

When to Increase Position Count vs. Position Size

As your account grows, you have two choices: increase the number of positions (more diversification) or increase the size of each position (more capital per trade). The answer depends on where you are in your journey.

Account under $50,000: Focus on increasing position count. You need more diversification. Go from 6 positions to 10 before making any single position larger.

Account $50,000–$150,000: Balance both. Increase position sizes on your best performers while also adding new positions in sectors where you are underweight.

Account over $150,000: Position count should plateau around 20–25 positions. Beyond that, management becomes difficult. Focus on increasing position size with the excess capital, but maintain the 5% maximum rule on a per-position basis.

The Compounding Effect of Proper Sizing

Here is where conservative position sizing creates extraordinary long-term results. Consider a $50,000 account that generates 1.5% monthly return through disciplined wheel trading with proper position sizing:

- After 1 year: $59,693 (19.4% annual return)

- After 3 years: $85,012 (compounded)

- After 5 years: $121,124 (compounded)

Now consider the same trader who uses aggressive 15% position sizes, achieves higher monthly returns of 3% for the first 18 months, but then gets wiped out by a 35% drawdown because two over-sized positions got assigned during a market correction:

- After 18 months: $85,000 (impressive run)

- After drawdown: $55,250 (lost 35% of peak value)

- Net after 2 years: $55,250 (barely ahead of starting capital)

The conservative trader reaches a higher account value with far less stress and far lower probability of catastrophic loss. Boring, but profitable. That is the wheel strategy philosophy applied to position sizing.

Common Position Sizing Mistakes Options Traders Make

Understanding what NOT to do is as valuable as knowing what to do. Here are the most common position sizing errors that wheel traders make.

Mistake 1: Sizing Based on Conviction

“I am really confident in this trade, so I am going bigger.” This is the number one account killer. Your conviction has almost no predictive value for the outcome of an individual trade. The market does not care how confident you are. Size every trade within your rules regardless of how you feel about it.

Mistake 2: Ignoring Total Portfolio Exposure

A trader sells five $50 puts, five $40 covered calls, and three $30 puts. Each individual position fits within their 5% rule. But their total capital committed is $31,000 in a $50,000 account — 62% of their capital. If the market drops 20% broadly, all positions lose simultaneously and the portfolio takes a devastating hit.

Your total committed capital should not exceed 70–80% of your account. Keep 20–30% in cash reserves for margin safety and opportunity capital.

Mistake 3: Not Accounting for Correlation

Having 5% in AMD, 5% in NVDA, 5% in INTC, and 5% in QCOM looks diversified — four different stocks. But they are all semiconductor companies. When the sector drops, all four positions move together. Effective position sizing considers correlation between positions.

Mistake 4: Averaging Down Without a Plan

Your put gets challenged and the stock drops. You think: “Great opportunity to sell another put at this lower price!” Without a predetermined averaging plan, you are effectively doubling your position size in a losing trade. If you are going to scale into positions, plan the sizing before the trade starts and include the potential second entry in your original allocation.

Mistake 5: Ignoring Assignment Probability Changes

When you sell a 30-delta put, there is roughly a 30% probability of assignment. If the stock drops and your put goes to 70-delta, the probability of assignment has more than doubled. Your effective risk has increased, but your position size has not changed. Some traders address this by rolling early, others by accepting assignment — but the key is having a plan for how increased assignment probability affects your portfolio-level risk.

How to Track Position Sizing Across Your Entire Portfolio

Once you move beyond 5–6 positions, tracking your portfolio-level position sizing becomes a challenge. You need to know at any moment: how much capital is committed, how much is at risk, what is your sector exposure, and how close are you to your maximum allocation limits.

The Spreadsheet Approach

Many traders start with a spreadsheet that tracks each position’s capital commitment, current value, premium collected, and sector. This works for small portfolios but breaks down as you scale. Common issues include manual update errors, forgetting to adjust cost basis after assignment, and inability to calculate real-time portfolio metrics.

The Professional Tool Approach

As your portfolio grows beyond 10–15 positions, professional tracking tools become worth the investment. The key features to look for in a position sizing and portfolio management tool are automatic cost basis adjustment after assignment, real-time portfolio allocation visualization, sector concentration alerts, premium collection tracking across full wheel cycles, and margin usage monitoring.

Most options screeners and brokerages were built for day traders or complex multi-leg strategies. But the wheel has unique needs: premium tracking through full cycles, assignment management, cost basis adjustments across puts and calls. A platform that understands the wheel cycle specifically can save hours of manual tracking and prevent costly errors.

For example, if you are managing 20 wheel positions across different stages — some in the cash-secured put phase, some assigned and running covered calls, some approaching expiration — your tracking tool needs to understand these transitions and adjust your portfolio metrics automatically.

Position Sizing for Beginners: Where to Start

If you are new to the wheel strategy and position sizing feels overwhelming, here is a simple starting framework you can implement today.

Step 1: Determine your total trading capital. This is the money you have specifically allocated for options trading. Not your emergency fund. Not your retirement savings. Your trading capital.

Step 2: Set your maximum per-position allocation at 5%. Multiply your total capital by 0.05. That is your maximum capital commitment per trade.

Step 3: Choose stocks that fit your position size. Divide your per-position maximum by 100 (since each options contract represents 100 shares). That gives you the maximum stock price you can wheel.

For a $30,000 account: $30,000 × 0.05 = $1,500 per position. $1,500 ÷ 100 = $15 maximum stock price.

Step 4: Start with 4–6 positions maximum. Even though your capital might support more, start small. Learn the mechanics, build your tracking system, and develop your management routine. You can always add positions later.

Step 5: Keep 40–50% in cash. As a beginner, being heavily invested increases stress and reduces your margin of safety. As you gain experience over 3–6 months, you can gradually increase your committed capital to 60–70% of your account.

Step 6: Review monthly. At the end of each month, review your position sizes relative to your current account value. Adjust up or down as needed.

Advanced Position Sizing Techniques

For experienced wheel traders who have mastered the basics, there are several advanced position sizing techniques worth exploring.

Volatility-Weighted Position Sizing

Instead of equal position sizes, weight each position inversely to its volatility. High-volatility stocks get smaller allocations, low-volatility stocks get larger ones. This equalizes the expected dollar move across all positions.

The formula: Position Size = (Target Risk ÷ Stock Volatility) × Normalizing Factor

For example, if Stock A has 40% implied volatility and Stock B has 20% implied volatility, Stock B gets twice the allocation because it is expected to move half as much. This means each position contributes roughly equal risk to your portfolio regardless of the underlying stock’s volatility profile.

Dynamic Sizing Based on Portfolio Heat

“Portfolio heat” is a concept from trend-following traders that applies well to the wheel strategy. It measures your total portfolio risk at any given moment — the sum of all position risks.

Maximum portfolio heat: Most conservative traders keep total portfolio heat below 15–20%. This means the sum of all individual position risks (each position’s maximum expected loss as a percentage of total capital) stays under 20%.

As positions expire or are closed, heat decreases and you can add new positions. When multiple positions are challenged simultaneously, heat increases and you should not add new trades until some positions resolve.

Conditional Position Sizing

Adjust your base position size based on specific market or stock conditions:

- VIX below 15: Reduce base position size by 20% (lower premiums do not compensate for risk)

- VIX above 30: Reduce base position size by 30% (higher risk of large moves)

- VIX 15–25: Standard position sizing (the sweet spot for the wheel)

- After earnings: Reduce position size by 40% for 5 trading days (event risk)

- Stock downtrend: Reduce position size by 25% (catching a falling knife risk)

These conditional adjustments add nuance to your base position sizing rules and can improve risk-adjusted returns over time.

The Barbell Approach

Allocate 80% of your capital to conservative, large-cap wheel positions with standard sizing. Allocate 20% to higher-IV, higher-risk positions with aggressive sizing (but each individual position stays small — 1–2% of total capital).

The conservative positions generate steady, reliable income. The aggressive positions generate outsized returns when they work and are small enough to absorb when they do not. This approach captures both safety and opportunity.

Position Sizing Tools and Calculators

While the math of position sizing is straightforward, having the right tools makes execution consistent and error-free. Here are the tools wheel traders commonly use.

A Position Sizing Calculator

A basic position sizing calculator takes three inputs — total account value, maximum percentage per position, and stock price — and tells you whether a trade fits your rules. You can build this in a simple spreadsheet:

Total Account Value: $50,000 Maximum Position Percentage: 5% Maximum Per Position: $2,500 Stock Price: $45.00 Capital Required (100 shares): $4,500 Fits Rule? No — exceeds maximum by $2,000

Portfolio Allocation Tracker

Beyond individual position sizing, you need a way to view your entire portfolio’s allocation. This should show committed capital versus available capital, sector allocation percentages, number of positions versus maximum target, portfolio heat or risk level, and cash reserve percentage.

Automated Portfolio Management

The next level beyond spreadsheets and calculators is an automated platform that tracks your position sizes in real time, alerts you when you approach allocation limits, and adjusts your risk metrics as positions move through the wheel cycle.

This is particularly valuable during the assignment phase. When a cash-secured put becomes an assigned stock position, your capital dynamics change. The put’s capital requirement becomes actual share ownership. Your portfolio tracker needs to understand this transition and adjust your available capital and sector exposure accordingly.

Start your free trial of QuantWheel →

Risk Disclosure: Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.