Last Updated: Tuesday, February 12, 2026 · Word Count: ~2,400 words · Reading Time: 5-9 minutes

What Is Options Premium?

Options premium is the price of an option contract. It's quoted per share, but since each contract controls 100 shares, you multiply by 100 to get the actual cost. Example:

- Option premium: $3.50 per share

- Actual cost per contract: $3.50 × 100 = $350

Premium for Buyers vs Sellers

Buyers pay premium to purchase the right (but not obligation) to buy or sell stock. Sellers receive premium for taking on the obligation to fulfill the contract if exercised. Premium is paid/received immediately when the trade executes.

Components of Premium

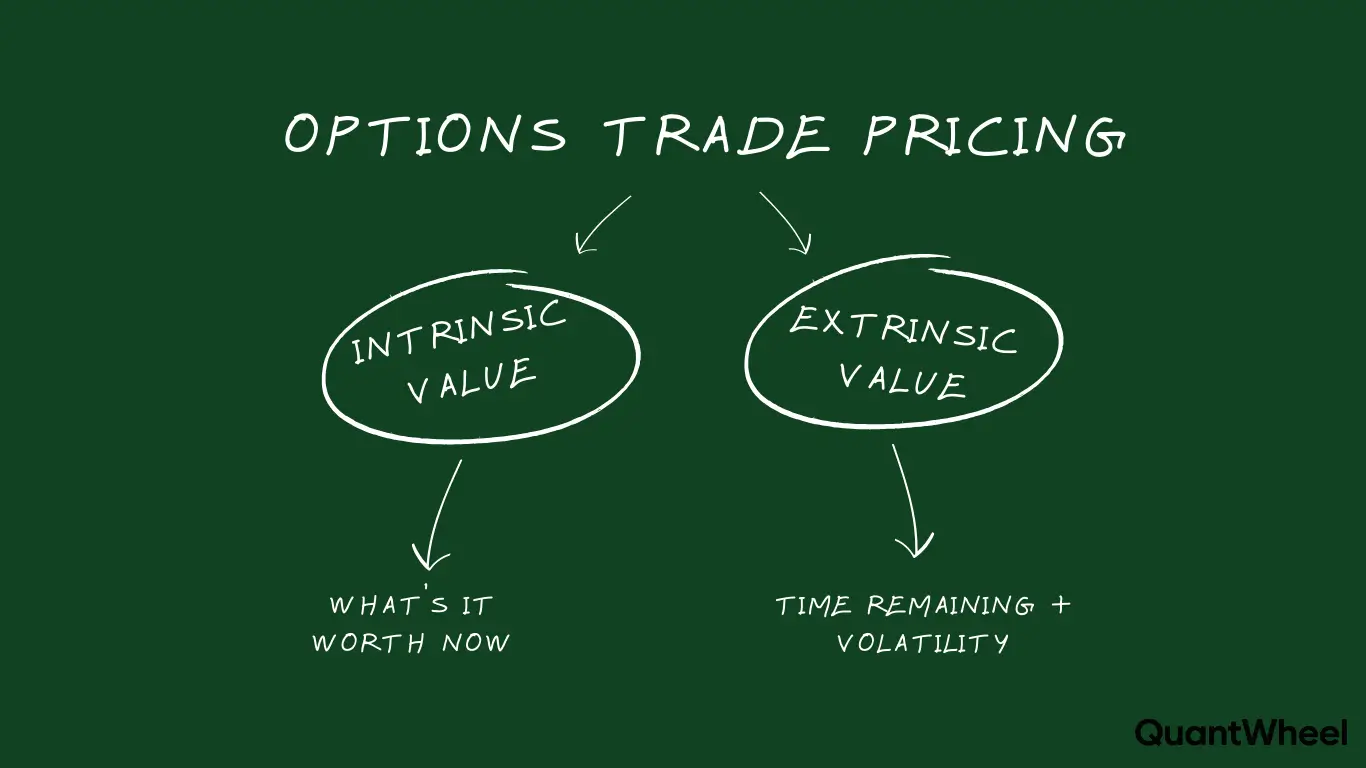

Every option premium consists of two parts: Premium = Intrinsic Value + Extrinsic Value

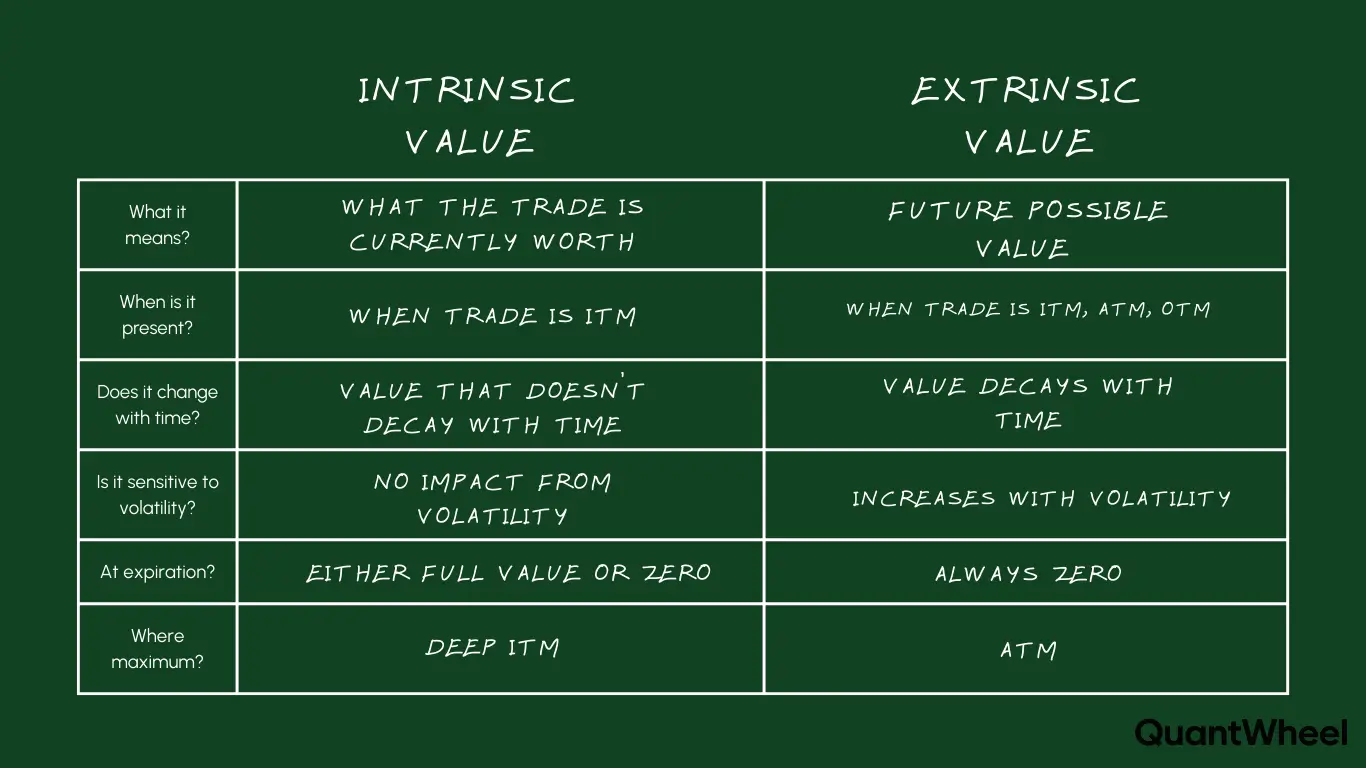

Intrinsic Value

Intrinsic value is the real, tangible value of an option—how much it would be worth if exercised right now.

For calls: Intrinsic Value = Stock Price - Strike Price (if positive)

For puts: Intrinsic Value = Strike Price - Stock Price (if positive)

Example:

- AAPL at $180

- $170 call intrinsic value = $180 - $170 = $10

- $175 put intrinsic value = $0 (stock above strike)

OTM options have zero intrinsic value—their entire premium is extrinsic.

Extrinsic Value (Time Value)

Extrinsic value is everything else—the "hope value" that the option might become more valuable before expiration. Extrinsic value includes:

- Time value: More time = more opportunity = more value

- Volatility value: More uncertainty = more potential = more value

Extrinsic Value = Premium - Intrinsic Value

Example:

- AAPL $170 call trading at $12

- Intrinsic value: $10 ($180 - $170)

- Extrinsic value: $2 ($12 - $10)

As expiration approaches, extrinsic value decays to zero. This is how options sellers make money.

What Affects Premium?

Five main factors drive option premiums:

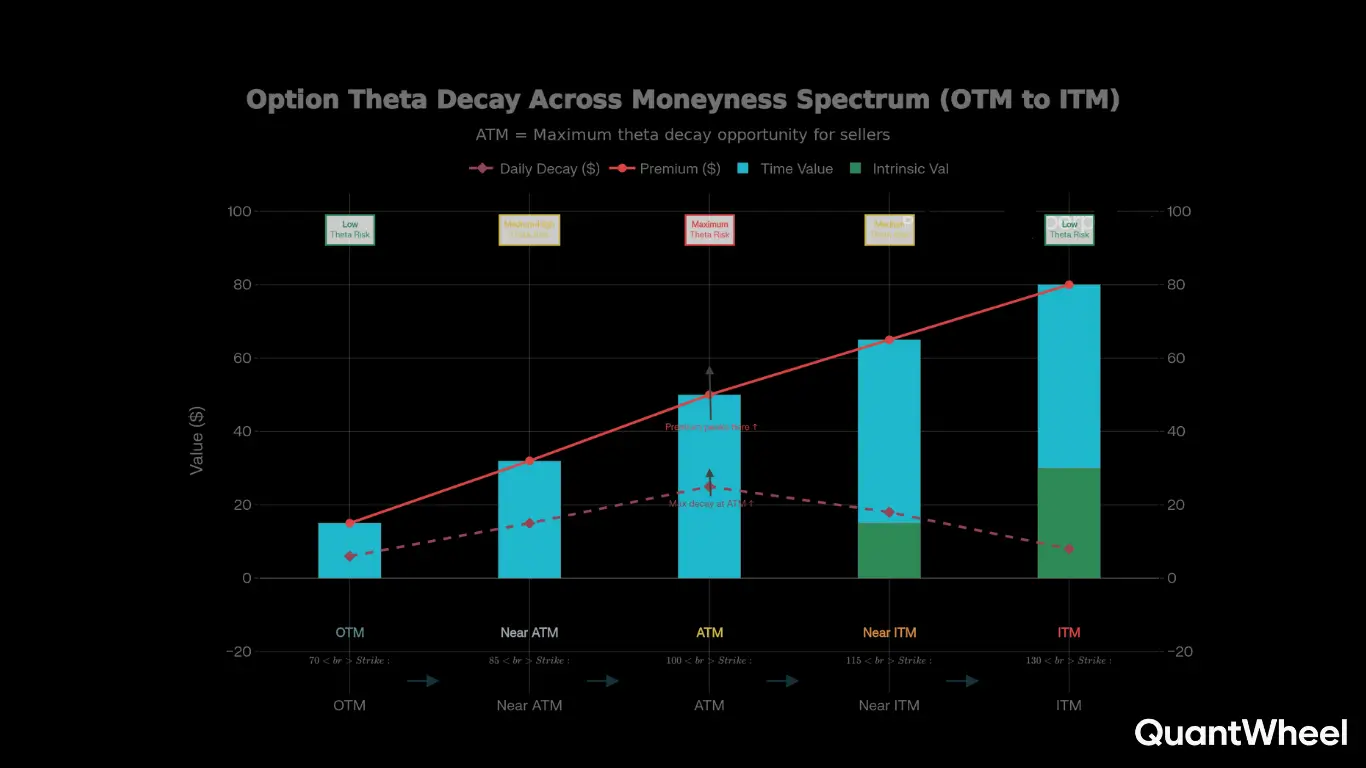

1. Stock Price vs Strike Price (Intrinsic Value)

The closer to (or further into) the money, the higher the premium. More ITM = Higher premium (more intrinsic value) More OTM = Lower premium (no intrinsic value)

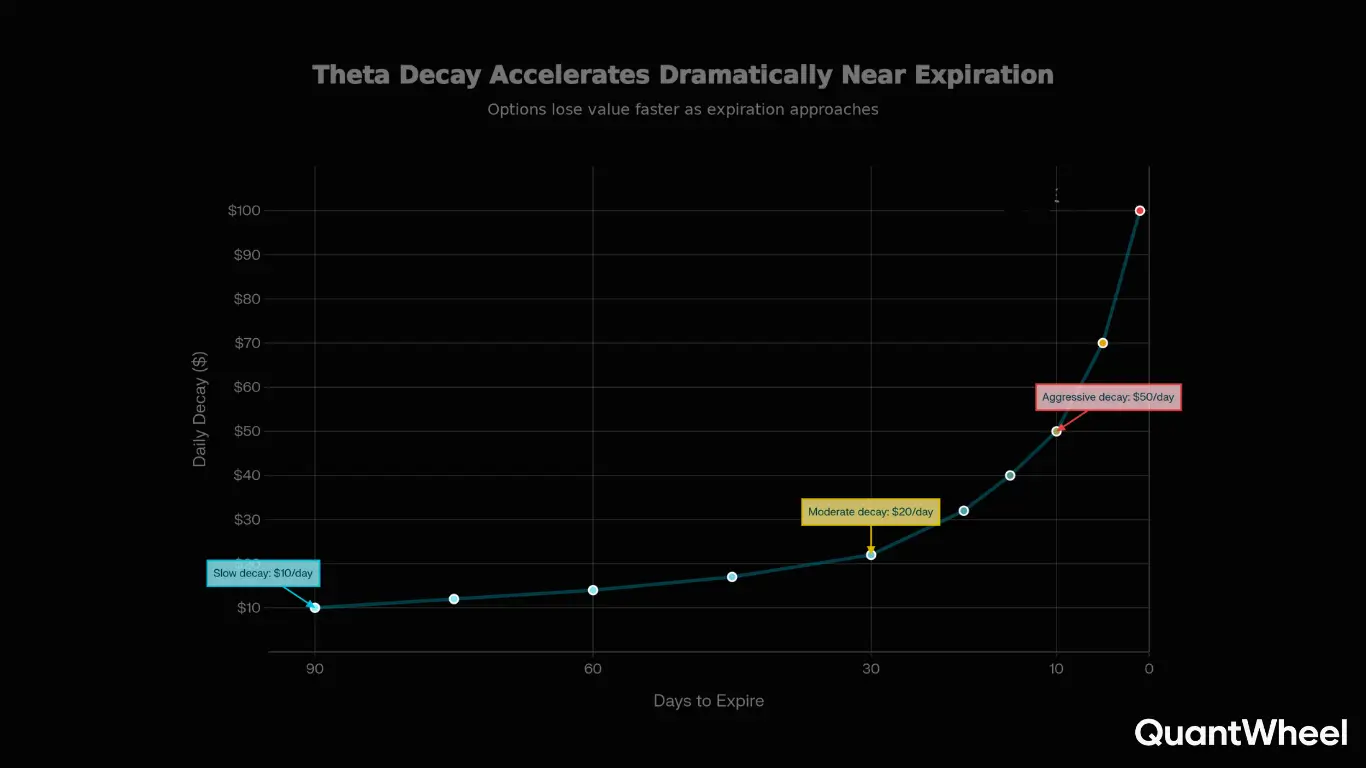

2. Time to Expiration

More time = more extrinsic value = higher premium. 45 DTE option: Higher premium 7 DTE option: Lower premium (same strike) Time decay (theta) erodes this value daily.

3. Implied Volatility (IV)

Higher IV = higher premiums. IV reflects expected future movement. High IV (earnings, news): Expensive options Low IV (calm markets): Cheap options This is the most controllable factor for traders:

- Sellers: Sell when IV is high to collect more premium

- Buyers: Buy when IV is low to pay less

4. Interest Rates

Higher interest rates slightly increase call premiums and decrease put premiums. Minor factor—usually ignored by retail traders.

5. Dividends

Expected dividends reduce call premiums and increase put premiums slightly. Important for: Covered call sellers near ex-dividend dates (early assignment risk).

Premium and the Greeks

The Greeks measure how premium changes with different factors:

| Greek | Measures | Effect on Premium |

|---|---|---|

| Delta | Price change per $1 stock move | Higher delta = premium changes more |

| Theta | Time decay per day | Premium decreases daily |

| Vega | IV sensitivity | Higher IV = higher premium |

| Gamma | Delta acceleration | Premium more sensitive near expiration |

Theta: The Premium Killer (or Profit Engine)

Theta represents daily time decay: For buyers: Theta is negative—you lose value every day For sellers: Theta is positive—you gain value every day

Example: Option with theta of -0.05

- Loses $5 per day (per contract) just from time passing

- If stock doesn't move, buyer loses $5/day

- Seller gains $5/day

This is why options sellers have a mathematical edge.

Premium for Different Strategies

Buying Calls (Pay Premium)

You pay premium hoping stock rises significantly. Considerations:

- ATM calls: Higher premium, higher delta

- OTM calls: Lower premium, lower probability

- Long-dated: More expensive but more time

Goal: Stock rises enough that option gains exceed premium paid.

Buying Puts (Pay Premium)

You pay premium hoping stock falls or to hedge. For hedging: Premium is like insurance cost For speculation: Need stock to fall enough to profit

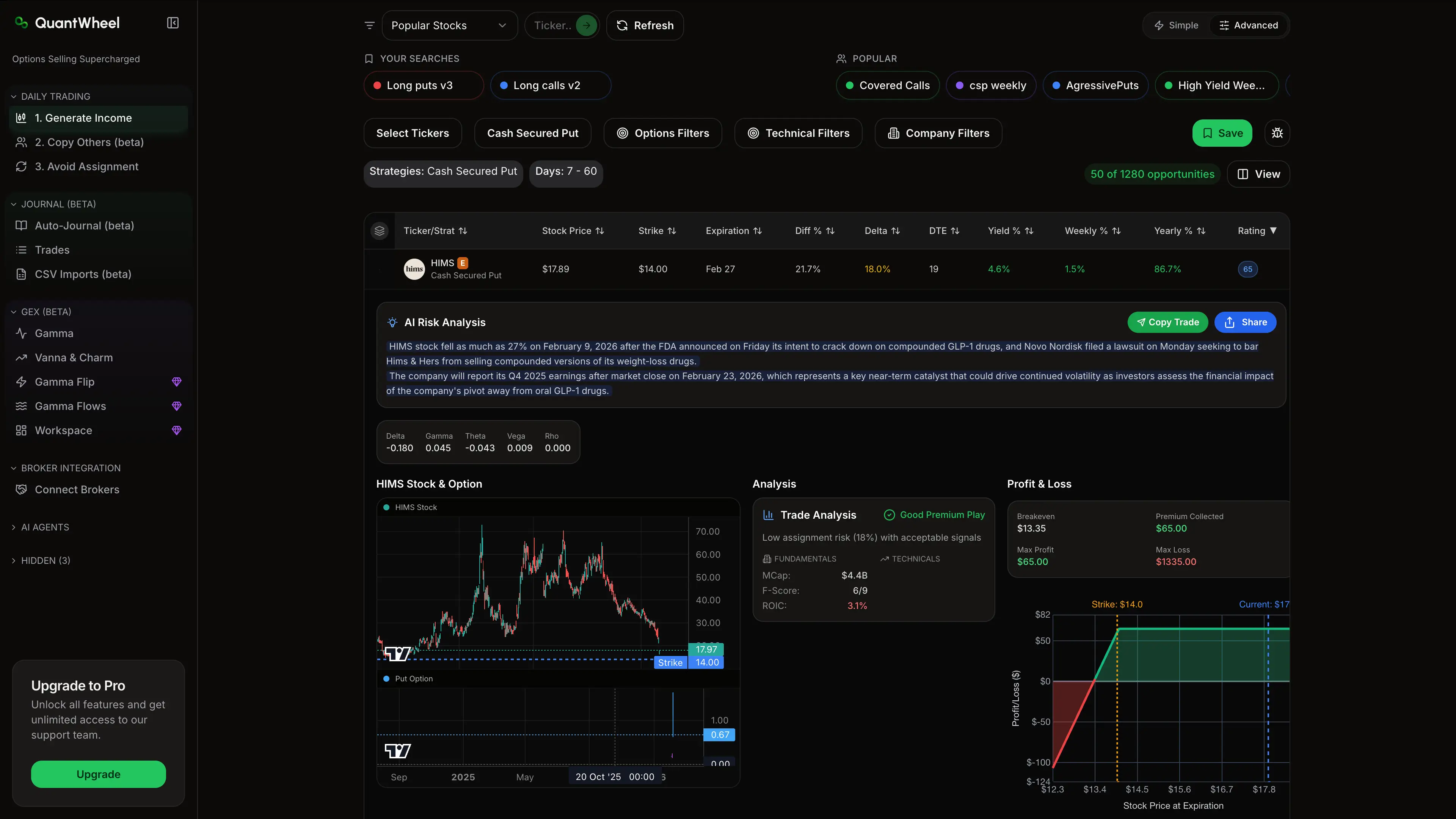

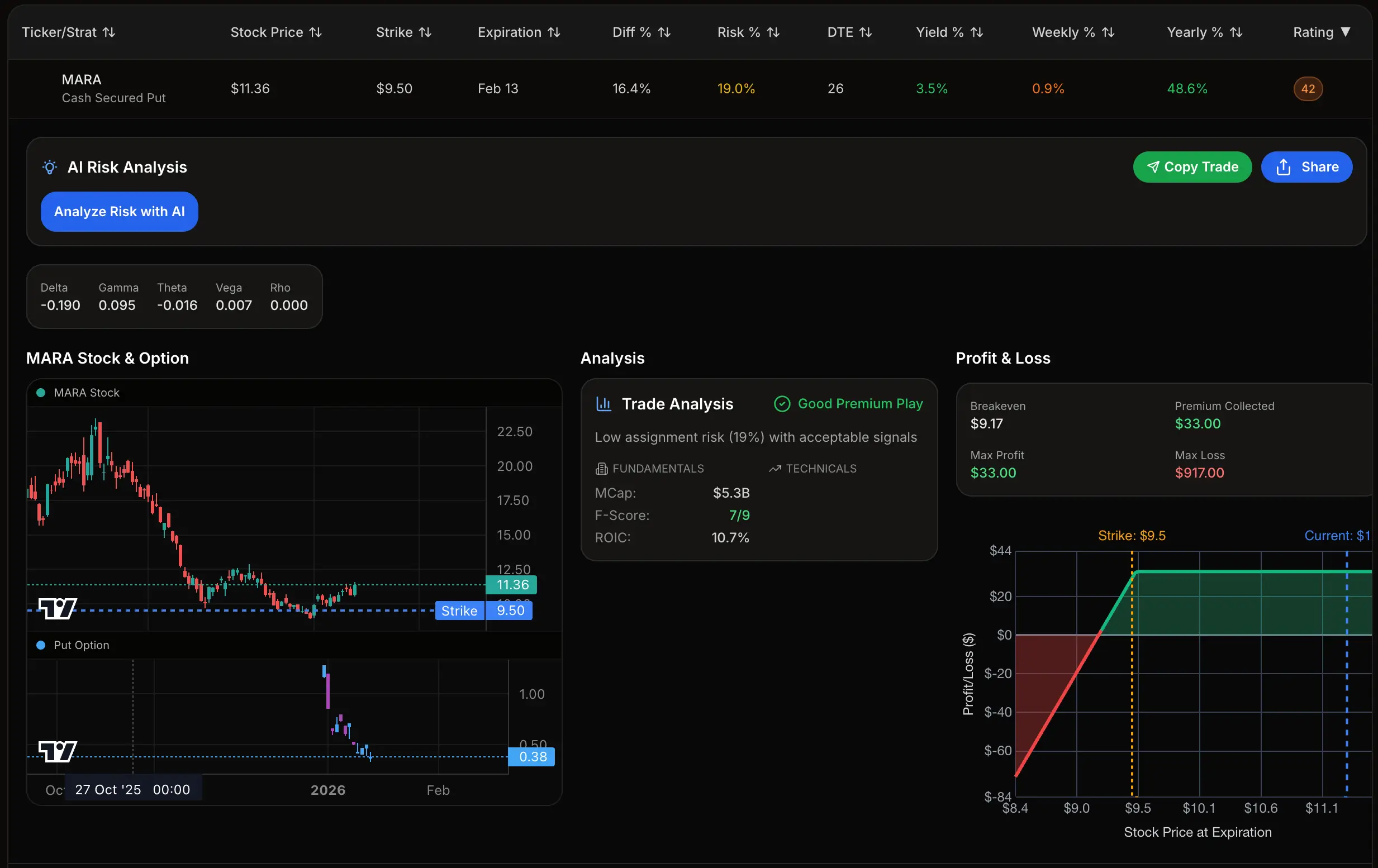

Selling Cash-Secured Puts (Receive Premium)

You receive premium for agreeing to potentially buy stock. Premium collected = Maximum profit

Ideal conditions:

- High IV (inflated premiums)

- Stock you want to own

- Strike below current price (OTM)

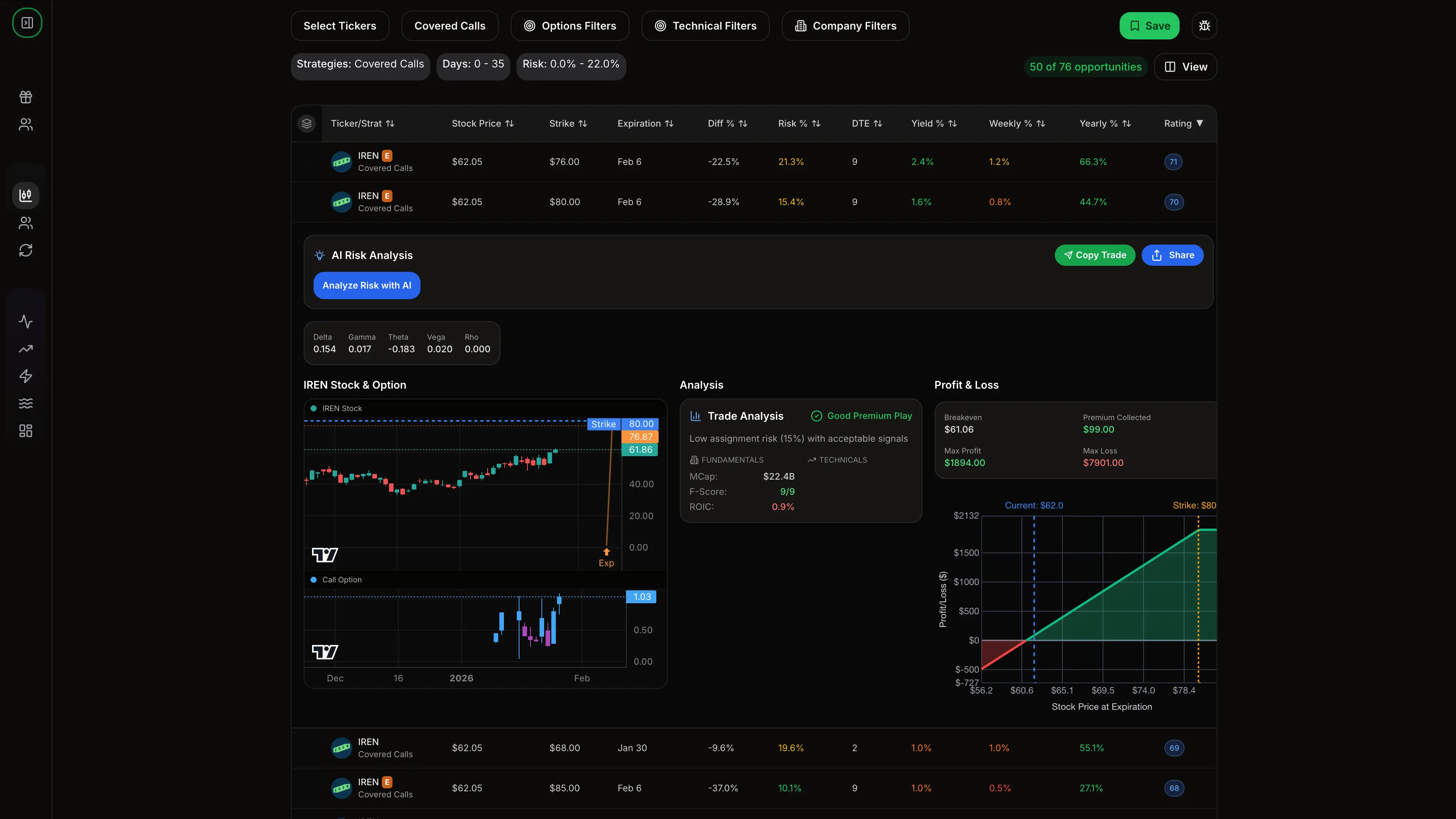

Selling Covered Calls (Receive Premium)

You receive premium for agreeing to potentially sell stock you own. Premium collected = Extra income on holdings

Ideal conditions:

- High IV

- Willing to sell at strike

- Strike above current price (OTM)

How to Evaluate Premium

Premium Yield Calculation

- For selling strategies, calculate the yield to compare opportunities:

Premium Yield = (Premium / Collateral) × (365 / DTE)

Example: Sell $170 put for $3 (30 DTE)

- Collateral: $17,000

- Premium Yield: ($300 / $17,000) × (365 / 30) = 21.5% annualized

QuantWheel does this for you:

Find more trades like these inside QuantWheel →

What's a Good Premium?

For cash-secured puts:

- Target: 1-2% per month (12-24% annualized)

- Minimum: 0.75% per month to be worthwhile

- Consider risk vs reward for each trade

For covered calls:

- Target: 1-2% per month

- Balance premium vs upside cap

Premium Red Flags

Very high premium usually means:

- Earnings announcement coming

- High uncertainty/risk

- Stock is very volatile

Very low premium usually means:

- Low IV environment

- Far OTM strike

- May not be worth the risk

Premium Strategies for Income

Maximizing Premium Income

- Sell when IV is elevated (IV Rank > 50)

- Use 30-45 DTE for optimal theta decay

- Target 0.20-0.30 delta for balance of premium and probability

- Close at 50% profit to capture quick wins

Premium Decay Timeline

- For a 45 DTE option sold for $3:

| DTE | Approx Value | Your Profit |

|---|---|---|

| 45 | $3.00 | $0 |

| 35 | $2.40 | $60 (20%) |

| 25 | $1.80 | $120 (40%) |

| 21 | $1.50 | $150 (50%) ← Close here |

| 14 | $1.00 | $200 (67%) |

| 7 | $0.50 | $250 (83%) |

| 0 | $0.00 | $300 (100%) |

Notice how the 50% profit comes in less than half the time. This is the power of the 45-21 rule.