The options Greeks sound intimidating, but they answer four simple questions:

– How much will my option move if the stock moves? Delta

– How much value am I losing each day? Theta

– How fast is everything changing? Gamma

– And how does volatility affect my premium? Vega

If you sell options – especially cash-secured puts and covered calls in the wheel strategy – the Greeks are your most practical tools for selecting strike prices, timing entries, and understanding exactly how your trades make money.

This guide breaks down all four main Greeks in plain English with real-world examples.

Author: David Romic – retail options trader and active member in the options trading communities on Reddit (u/thedavidromic).

I share wheel strategy setups, trade management, and lessons learned from real positions.

What Are the Options Greeks?

The options Greeks are measurements that describe how sensitive an option’s price is to different factors. Each Greek tells you one thing about your option trade outcome.

In plain english: Delta is your speedometer, theta is your fuel gauge (burning down daily), gamma is your acceleration, and vega is your weather forecast.

Together, they tell you everything about how your position behaves.

Delta: How Much Your Option Moves With the Stock

Delta measures how much an option’s price changes for every $1 move in the underlying stock.

How Delta Works

If you think a stock will move, you get more for buying an option vs buying the stock.

Why? Because you can spend less by buying a few options rather than buying the stock and then get more value for your money.

You gain more percentage-wise on the option than owning the stock for the same $1 move, due to leverage on your smaller investment (the premium).

Stock example ($100/share, 100 shares): $1 up = +$100 total (+1% return).

Call (Δ=0.50, premium ~$2/share): +$50 total (+25% return on $200 premium)

| Delta Value | Option Type | What It Means | Example |

|---|---|---|---|

| 0.80 – 1.00 | Deep ITM Call | Moves nearly $1 for $1 | Stock up $1 → option up ~$0.85 |

| 0.50 | ATM Call | 50/50 chance of finishing ITM | Stock up $1 → option up ~$0.50 |

| 0.10 – 0.30 | OTM Call | Low probability of finishing ITM | Stock up $1 → option up ~$0.20 |

| -0.20 to -0.30 | OTM Put | Sweet spot for CSP sellers | Stock down $1 → put up ~$0.25 |

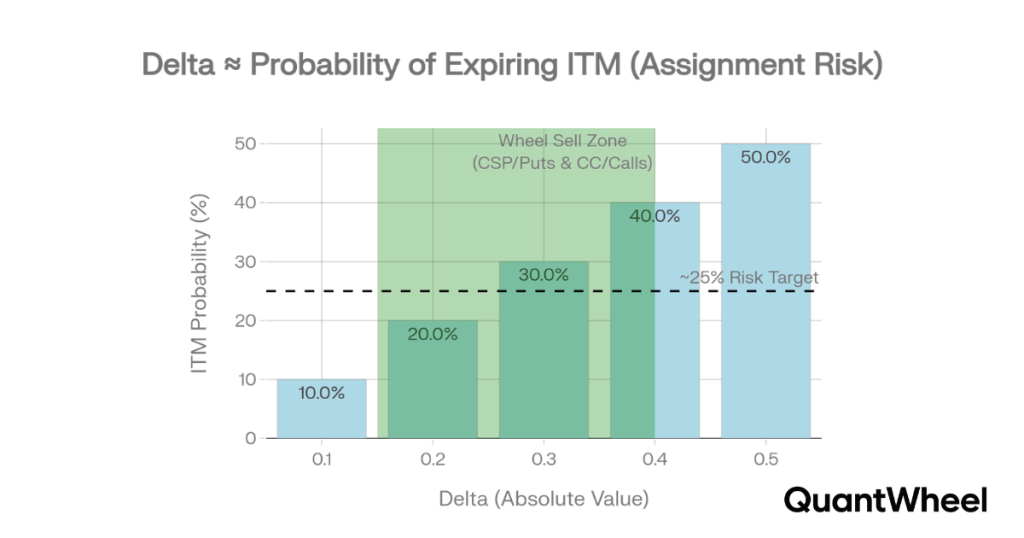

Delta as Assignment Probability

Here’s the most practical use of delta for wheel strategy traders: delta roughly approximates the probability of an option expiring in the money.

This is why most wheel traders sell cash-secured puts at the 0.20 to 0.30 delta range.

What happens is that you’re accepting a 20-30% probability of assignment in exchange for premium.

For covered calls, most wheel traders sell at the 0.25 to 0.35 delta range.

This balances keeping your shares against collecting reasonable premium.

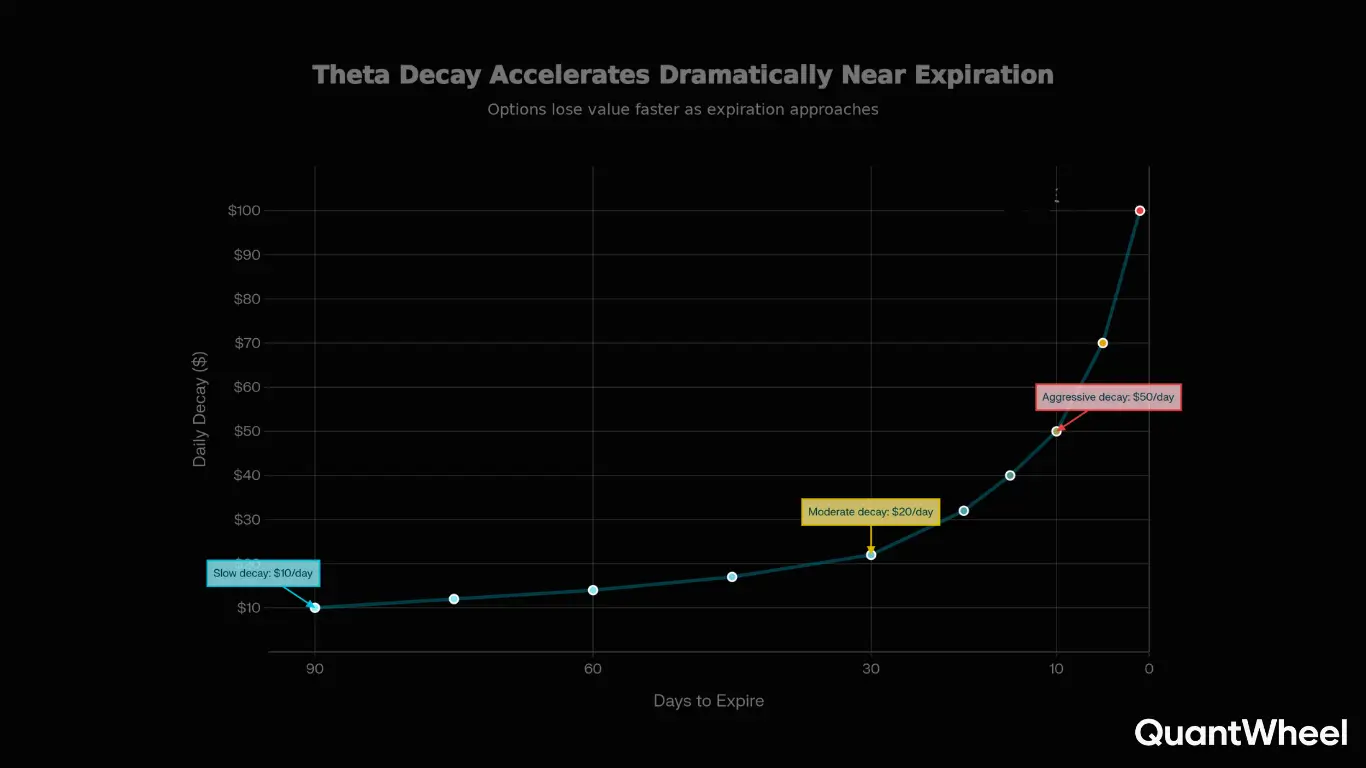

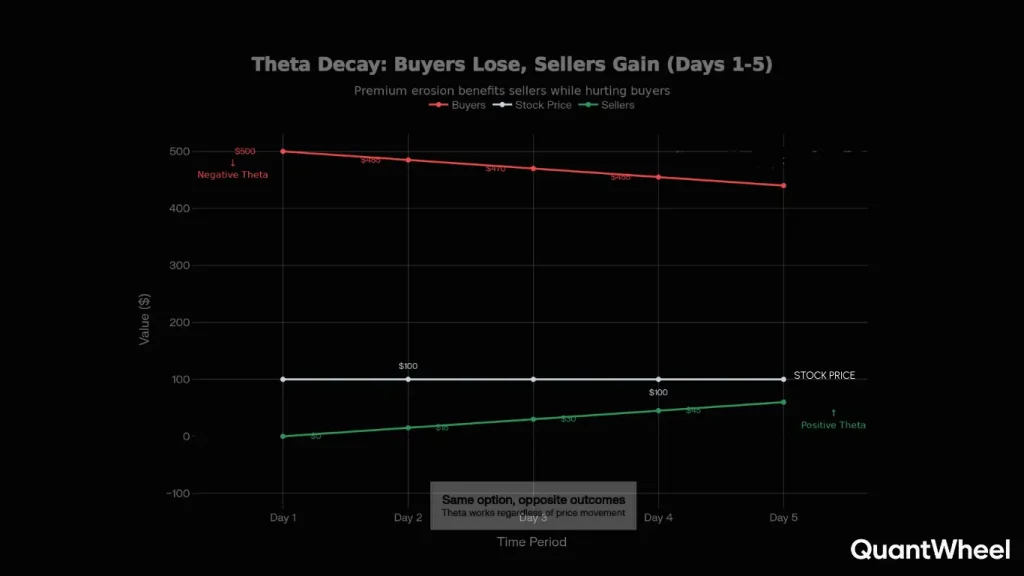

Theta: Your Daily Income as an Options Seller

Theta measures how much value an option loses per day from time decay alone. For options sellers, theta is your best friend – it represents the money flowing from the buyer to you every single day.

How Theta Works

If an option has a theta of -0.05, it loses $0.05 per share ($5 per contract) in value every day, assuming nothing else changes. As a seller, that’s $5 per day going into your pocket.

Theta accelerates as expiration approaches. An option with 45 days to expiration might lose $3/day, while the same option with 7 days left might lose $12/day. This acceleration is why many wheel traders sell options with 30-45 days to expiration – you capture the most theta decay in the optimal time window.

Theta Decay Curve: When Time Decay Accelerates

| Days to Expiration (DTE) | Daily Theta Decay | Decay Speed | Strategy Implication |

|---|---|---|---|

| 90 DTE | ~$1-2/day | Slow | Too early – capital tied up for little decay |

| 45 DTE | ~$3-5/day | Moderate | ✓ Ideal entry point for selling |

| 30 DTE | ~$5-8/day | Accelerating | ✓ Strong decay, still good premium |

| 14 DTE | ~$8-12/day | Fast | Consider closing at 50% profit |

| 7 DTE | ~$12-18/day | Very Fast | Gamma risk increases – close or roll |

| 1-3 DTE | ~$15-25/day | Maximum | High risk – gamma spikes can erase gains |

The sweet spot for most wheel traders is selling at 30-45 DTE and closing or rolling at 14-21 DTE. You capture the steepest part of the decay curve while avoiding the high gamma risk in the final week.

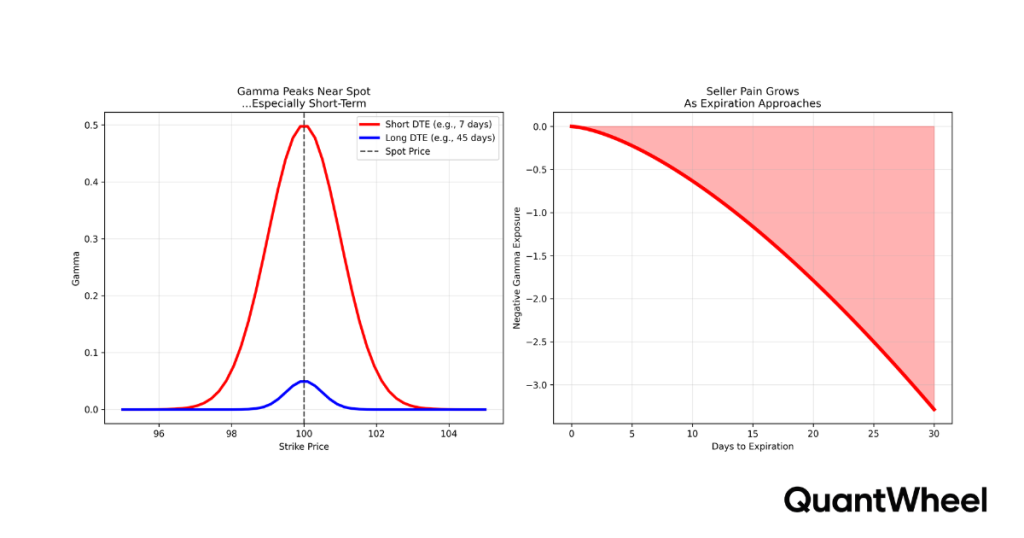

Gamma: Why Options Get Unpredictable Near Expiration

Gamma measures how much delta changes when the stock moves $1. If delta is your speed, gamma is your acceleration.

High gamma means your position’s risk profile can change rapidly with small stock movements.

How Gamma Works

Say you sold a put with a delta of -0.25 and a gamma of 0.03. If the stock drops $1, your new delta becomes approximately -0.28 (delta changed by gamma). If the stock drops another $1, delta moves to about -0.31. Each dollar of stock movement makes your position more sensitive to the next dollar.

Gamma is highest for at-the-money options near expiration. This is called “gamma risk” and it’s the main reason wheel traders should be cautious about holding options into the final week before expiration.

Gamma Risk by Days to Expiration

| DTE | ATM Gamma | Risk Level | What Can Happen |

|---|---|---|---|

| 45 DTE | Low (0.01-0.02) | Low Risk | Delta changes slowly, position is stable |

| 14 DTE | Medium (0.03-0.05) | Moderate Risk | Delta shifts faster, monitor closely |

| 3-5 DTE | High (0.08-0.15) | High Risk | Small stock move can flip OTM to ITM rapidly |

| 0-1 DTE | Extreme (0.15+) | Extreme Risk | Delta can swing from 0.10 to 0.90 in hours |

For wheel strategy traders, gamma is the reason you should consider closing positions at 50% profit or rolling them when they reach 14-21 DTE. The remaining premium often isn’t worth the gamma risk of holding into the final days.

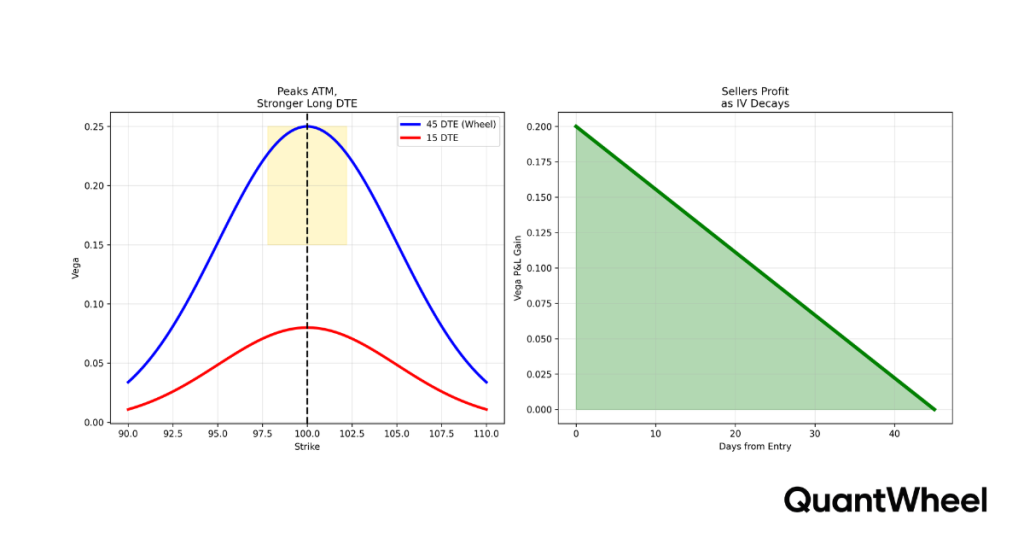

Vega: How Volatility Changes Your Premium

Vega measures how much an option’s price changes when implied volatility (IV) moves by 1 percentage point.

Vega peaks at-the-money (ATM) and is strongest in 45 DTE wheel trades. Sellers grab high vega premium near spot upfront, gaining as IV decays over time.

How Vega Works

If an option has a vega of 0.10 and implied volatility increases from 30% to 31%, the option’s price increases by approximately $0.10 per share ($10 per contract). If IV drops from 30% to 29%, the option loses $10.

As an options seller, you want to sell when IV is high (rich premiums, high vega) and buy back when IV drops (cheaper to close). This is the core mechanics behind the popular strategy of selling options before earnings and closing after the “IV crush.”

Vega and the Wheel Strategy

Understanding vega helps wheel traders time their entries. Selling a cash-secured put when IV is elevated means you collect more premium for the same strike price and same expiration. When IV eventually contracts back to normal levels, the option loses value faster than theta alone would predict – and you can close for a quicker profit.

| IV Environment | Premium Level | Vega Impact | Strategy for Sellers |

|---|---|---|---|

| Low IV (below IV Rank 20) | Thin premiums | Low – small IV changes, small price impact | Consider waiting or going closer to ATM |

| Normal IV (IV Rank 20-50) | Fair premiums | Moderate – standard conditions | Standard wheel entries at 0.20-0.30 delta |

| High IV (IV Rank 50+) | Rich premiums | High – IV contraction = fast profit | ✓ Ideal selling conditions |

| Extreme IV (IV Rank 80+) | Very rich premiums | Very high – big swings possible | Sell further OTM, reduce position size |

A common mistake is chasing high IV without adjusting your strike selection. When IV is elevated, you should sell further out of the money than usual. The elevated premium compensates for the wider strike, and you get a bigger margin of safety if the stock moves against you.

How the Greeks Work Together: A Real Example

The Greeks don’t exist in isolation. Here’s how they interact on a typical wheel strategy trade.

Scenario: You sell a cash-secured put on a stock trading at $175. You sell the $165 strike put with 35 DTE for $2.50 premium.

| Greek | Value | What It Tells You |

|---|---|---|

| Delta: -0.25 | ~25% chance of assignment | If stock drops $1, option gains ~$0.25 in value against you |

| Theta: -0.04 | $4/day decay in your favor | You earn ~$4/day just from time passing |

| Gamma: 0.02 | Delta changes 0.02 per $1 | Low gamma – position is stable at 35 DTE |

| Vega: 0.12 | $12 per 1% IV change | If IV drops 2%, option loses $24 – good for you as a seller |

Day 1-14: Stock stays around $173-177. Delta stays near -0.25, gamma is low and stable. Theta eats away $4/day = ~$56 of decay in your favor. IV drops slightly, adding another $10-15 of profit from vega.

Day 15 (21 DTE): Option is now worth $1.20 (you sold for $2.50). That’s 52% profit. Many wheel traders would close here and redeploy capital rather than holding into the high-gamma zone.

Result: $130 profit in 14 days on a $16,500 capital commitment = 0.79% return in 2 weeks, or roughly 20% annualized. That’s the Greeks working together for a premium seller.

Options Greeks Cheat Sheet for Wheel Traders

| Greek | Seller Wants | Ideal Range (CSP) | Ideal Range (CC) | Watch Out For |

|---|---|---|---|---|

| Delta | Low absolute value | -0.20 to -0.30 | 0.25 to 0.35 | Delta creeping above 0.50 (likely assignment) |

| Theta | High daily decay | Sell at 30-45 DTE for best decay curve | Theta alone doesn’t compensate for gamma risk under 7 DTE | |

| Gamma | Low gamma | Under 0.05 (stay above 14 DTE) | Gamma spikes in last 7 days can erase weeks of theta gains | |

| Vega | Sell high, buy low | Sell when IV Rank > 30, ideally > 50 | Selling in low IV = thin premiums, potential IV expansion loss | |

5 Common Greeks Mistakes That Cost Traders Money

1. Ignoring gamma near expiration. Holding a short option into the last 3-5 days to squeeze out the remaining $20-30 of theta, only to have a sudden stock move cause $200+ in losses. The theta-to-gamma ratio becomes unfavorable inside 7 DTE.

2. Selling options in low IV environments. When IV Rank is below 15-20, premiums are thin and you’re getting paid very little for your risk. Worse, if IV expands after you sell, vega works against you and your position moves into a loss even if the stock doesn’t move.

3. Using delta for exact probabilities. Delta is an approximation of assignment probability, not a guarantee. Market conditions, skew, and model assumptions all affect the actual probability. Use delta as a guide, not a precise prediction.

4. Forgetting Greeks change constantly. The Greeks you see when you open a trade are a snapshot. They shift every day as time passes, as the stock moves, and as volatility changes. A position that started at 0.20 delta can drift to 0.50 delta after a stock move. Check your Greeks regularly.

5. Overcomplicating the analysis. You don’t need to calculate Greeks by hand or monitor them every hour. For most wheel strategy trades, checking delta and theta at entry, monitoring delta weekly, and being aware of gamma risk near expiration covers 90% of what you need.

Practical Workflow: Using Greeks in Your Wheel Strategy

Here’s a simple step-by-step process for incorporating the Greeks into your wheel trades:

Step 1 – Check IV environment (Vega). Before opening any new position, look at the stock’s IV Rank or IV Percentile. If it’s above 30, conditions are favorable for selling. If it’s below 20, consider waiting or choosing a different stock with better premiums.

Step 2 – Select your strike using delta. For cash-secured puts, find the strike with a delta between -0.20 and -0.30. For covered calls, look for 0.25 to 0.35 delta. This gives you a balance of premium and probability.

Step 3 – Confirm theta is working for you. Check the daily theta. Multiply it by the number of days you plan to hold. Is the potential theta income worth the capital requirement? If theta seems low relative to the premium, the trade might not be efficient.

Step 4 – Set a management plan based on gamma. Decide before entering: “I’ll close at 50% profit or roll at 21 DTE, whichever comes first.” This keeps you out of the high-gamma danger zone in the final week.

Step 5 – Monitor weekly. Check your delta once a week. If it has drifted significantly from where you opened (e.g., from -0.25 to -0.45), consider adjusting, rolling, or closing the position.

Start your free trial of QuantWheel →

Related Articles

- Introduction to Options Greeks

- Delta Explained: The Most Useful Greek for Options Traders

- Theta and Time Decay: How Options Sellers Make Money

- Gamma Explained: Why Options Get Risky Near Expiration

- Vega Explained: How Volatility Affects Your Options

- Implied Volatility Explained for Options Traders

- IV Crush: What It Is and How to Profit From It

- How to Select the Right Strike for Cash-Secured Puts

Risk Disclosure: Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions. The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security.