For most wheel traders, the sweet spot for DTE is 30-45 days. This range balances optimal theta decay with enough time to manage positions if the trade moves against you. You can read more about how to adjust this based on your strategy and risk tolerance - and also based on how's the market behaving.

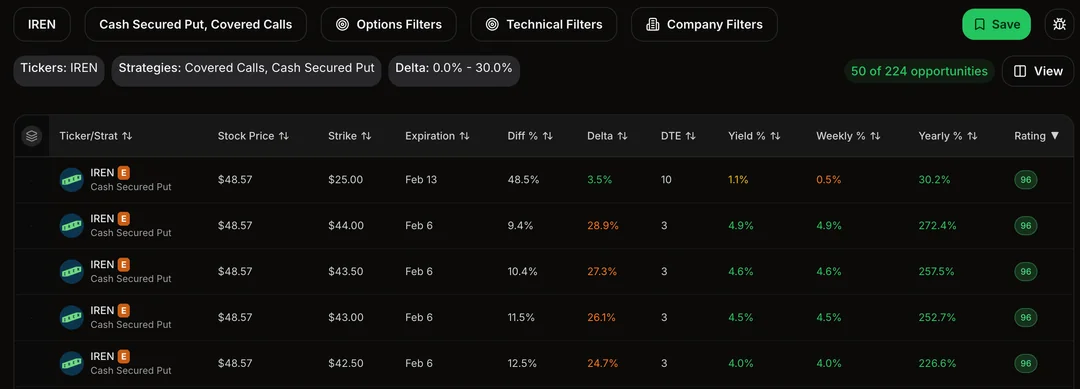

Choosing DTE comes down to four factors: your capital size, the stock's volatility, your assignment willingness, and current market conditions. Getting even one of these wrong can turn a profitable setup into a forced assignment. Once you understand how to pick the DTE from the article below, you can make your process of picking DTE faster and better inside QuantWheel. It can help you decide on a single glance what's better, rather than taking a guess. Here's a small screenshot from it:

We recommend you to keep on reading to understand how to pick DTE the best, then create a system inside QuantWheel to make the process of picking DTE faster and more precise.

Understanding Options Expiration Selection

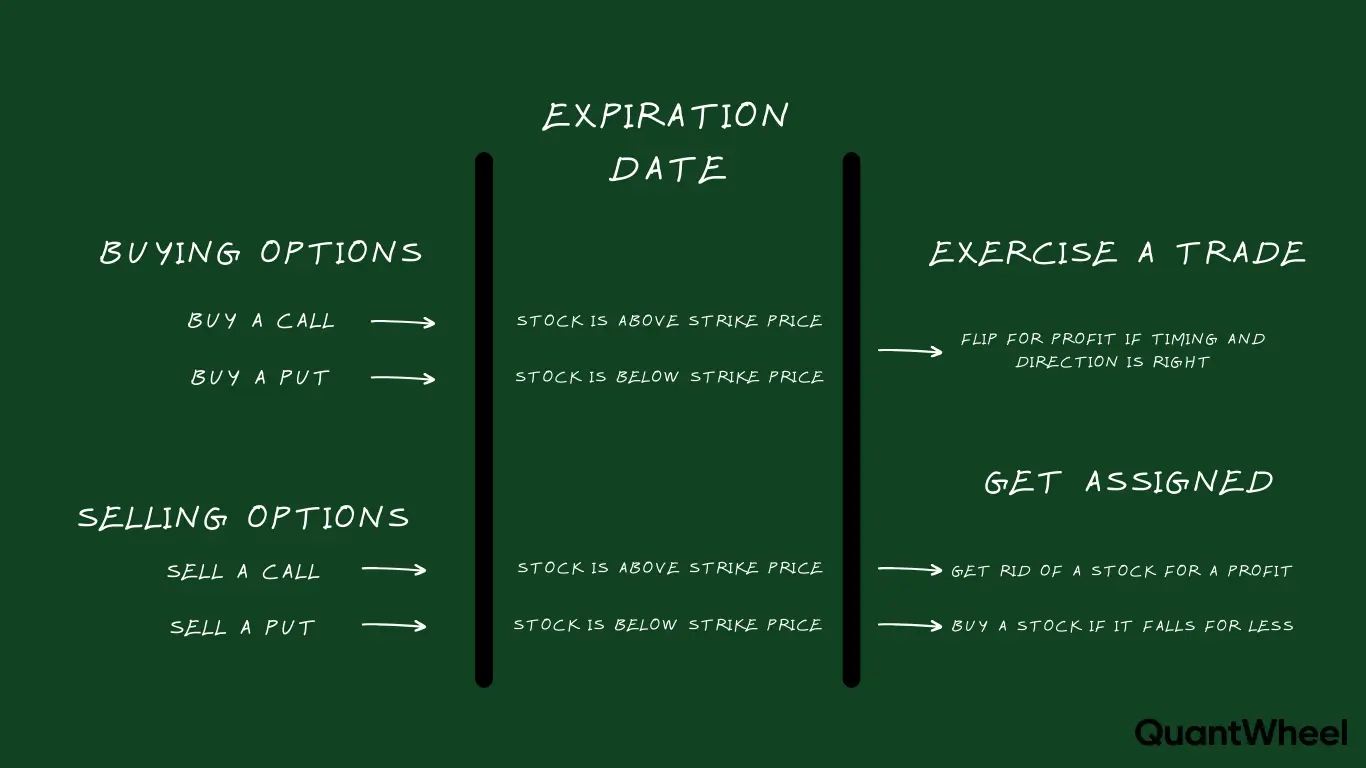

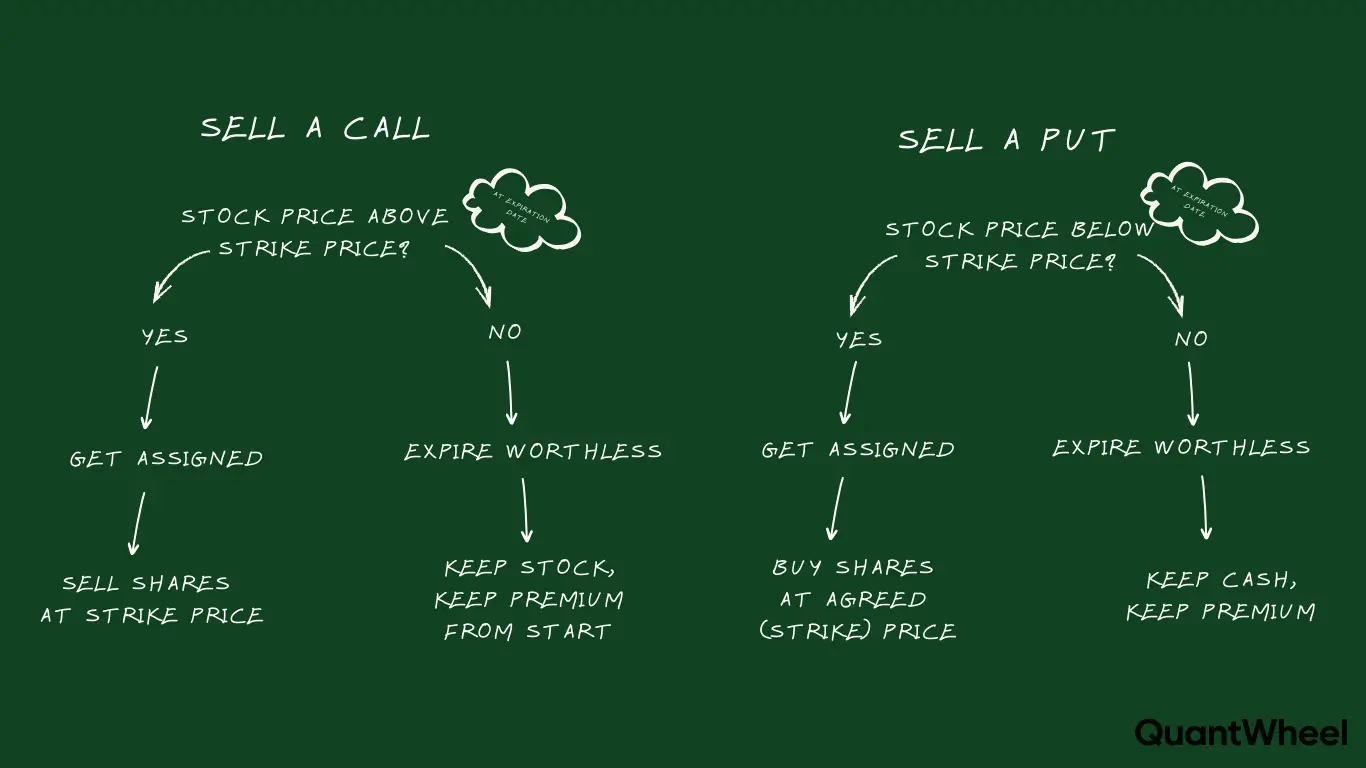

Options expiration selection is the process of choosing when your option contract ends. Every option has an expiration date - the last day the contract is valid. After this date, the option either exercises (if in-the-money) or expires worthless (if out-of-the-money).

For wheel strategy traders, expiration selection affects three critical factors:

- Premium collected - Longer expirations typically offer more total premium

- Theta decay rate - Shorter expirations decay faster per day

- Management frequency - Shorter expirations require more attention

The expiration you choose should match your trading style, available time, and market conditions.

TLDR: How to Choose Your Options Expiration

For most wheel strategy traders, 30-45 DTE (days to expiration) is the sweet spot. Here's why in simple terms:

Think of options like ice cubes melting. The premium you collect is like getting paid to watch ice melt. Ice melts fastest right before it disappears completely - that's theta decay acceleration.

The 30-45 DTE Range:

- You sell an option with 45 days left

- You collect good premium (maybe $200 on a $5,000 position = 4%)

- You wait for it to hit 50% profit (usually around 21 DTE)

- You close early and start again

- You repeat this 6-8 times per year instead of holding to expiration

Simple Example: You have $5,000 to sell a cash-secured put on AMD at $50 strike.

- 45 DTE option: Collect $200 premium, close at 50% profit ($100 gain) in ~24 days

- 14 DTE option: Collect $80 premium, close at 50% profit ($40 gain) in ~7 days

- 60 DTE option: Collect $250 premium, but takes 36+ days to reach 50% profit

Over a year, the 45 DTE strategy wins because theta decay accelerates as expiration approaches. You're capturing the best part of time decay while avoiding the risky final 2 weeks.

Quick Decision Framework:

- Plenty of time to trade? → 30-45 DTE monthly options

- Very busy schedule? → 45-60 DTE, less frequent management

- High IV environment? → 14-21 DTE to capture premium before IV drops

- Low IV environment? → 45+ DTE to collect enough premium to matter

Weekly vs Monthly Options: The Complete Comparison

The first major decision in expiration selection is whether to trade weekly or monthly options. Each approach has distinct advantages and trade-offs that affect your returns, time commitment, and stress levels.

Weekly Options (0-7 DTE)

Weekly options expire every Friday, giving you 52 potential expiration dates per year. These contracts feature rapid theta decay and require active management.

Advantages of Weekly Options:

- Fastest theta decay per day

- Higher annualized return potential

- Quick capital recycling

- Flexibility to adjust frequently

- Can capitalize on short-term events

Disadvantages of Weekly Options:

- Requires constant monitoring

- Higher transaction costs (52 trades vs 12 per year)

- More stressful management

- Less time for positions to work

- Higher risk of gamma exposure near expiration

Who Should Trade Weeklies:

- Full-time traders with time for daily management

- Traders comfortable with active position monitoring

- Those trading highly liquid underlyings (SPY, QQQ, AAPL)

- Experienced traders who understand gamma risk

Real Example - Weekly Strategy: You sell a $100 strike put on SPY every Monday with 5 DTE, collecting $80 premium. Over 52 weeks, that's potentially $4,160 in premium if every trade works perfectly. However, transaction costs ($1-2 per trade × 52 = $52-104) and the occasional loss eat into returns.

Monthly Options (30-45 DTE)

Monthly options are the standard expiration cycle used by most wheel traders. These contracts expire on the third Friday of each month.

Advantages of Monthly Options:

- Optimal theta decay acceleration zone

- Better work-life balance

- Lower transaction costs

- More time for positions to recover

- Collect meaningful premium per trade

Disadvantages of Monthly Options:

- Slower capital recycling

- Less flexibility for short-term adjustments

- May tie up capital during low-IV periods

- Fewer trading opportunities per year

Who Should Trade Monthlies:

- Part-time traders with day jobs

- Traders seeking "boring" systematic income

- Those managing 10+ positions simultaneously

- Traders focusing on capital efficiency over activity

Real Example - Monthly Strategy: You sell a $100 strike put on SPY with 45 DTE, collecting $250 premium. You close at 50% profit (~$125 gain) around 21 DTE. You repeat this approximately 8 times per year, generating roughly $1,000 in realized gains with 8 total transactions.

The Math: Weekly vs Monthly Returns

Let's compare annualized returns using the same $10,000 capital:

Weekly Strategy (5 DTE):

- Premium per trade: $80

- Trades per year: 52

- Gross premium: $4,160

- Transaction costs (52 trades × $1.50): -$78

- Win rate (95%): $3,952

- Net return: ~39.5%

Monthly Strategy (45 DTE, close at 50%):

- Premium per trade: $250

- Close at 50% profit: $125 realized

- Trades per year: 8-9

- Gross premium: $1,125

- Transaction costs (9 trades × $1.50): -$13.50

- Win rate (92%): $1,035

- Net return: ~10.4%

Wait - weekly looks better, right? Not quite. The weekly strategy assumes:

- Zero losses (unrealistic)

- Perfect execution every week

- No opportunity cost when markets are quiet

- You never miss a week

- No stress or burnout

The monthly strategy is more realistic for sustainable, long-term wheel trading. The annualized return includes transaction costs, realistic win rates, and assumes you're closing profitable positions early rather than holding to expiration.

Hybrid Approach: The Best of Both Worlds

Many experienced wheel traders use a hybrid approach:

- Core positions: 30-45 DTE monthlies on 70% of capital

- Tactical positions: 7-14 DTE weeklies on 30% of capital during high-IV events

This combines the sustainability of monthly expirations with the flexibility to capitalize on short-term opportunities.

Example Hybrid Portfolio:

- AMD 45 DTE put: $500 capital

- NVDA 45 DTE put: $500 capital

- TSLA 45 DTE put: $500 capital

- SPY 7 DTE put (high IV spike): $150 capital

Understanding DTE: Days to Expiration Strategy

DTE (Days To Expiration) is the number of calendar days remaining until the option expires. Understanding theta decay curves at different DTE levels is essential for maximizing returns.

The Theta Decay Curve

Theta decay isn't linear - it accelerates as expiration approaches. Here's how time decay works across different timeframes:

60+ DTE (Slow Decay Zone):

- Theta decay: ~0.02-0.05 per day

- Premium mostly from IV and delta

- Time decay is minimal

- Capital intensive relative to theta collected

45 DTE (Entry Zone):

- Theta decay: ~0.05-0.08 per day

- Balanced premium collection

- Optimal starting point for most trades

- Good theta-to-premium ratio

30 DTE (Acceleration Zone):

- Theta decay: ~0.08-0.12 per day

- Decay starting to accelerate

- Sweet spot for many traders

- Strong risk-reward balance

21 DTE (Peak Efficiency Zone):

- Theta decay: ~0.12-0.18 per day

- Rapid time decay

- Common profit-taking point

- Risk still manageable

14 DTE (High Risk Zone):

- Theta decay: ~0.18-0.25 per day

- Very fast decay

- Gamma risk increasing

- Exit zone for most traders

7 DTE (Danger Zone):

- Theta decay: ~0.25-0.40 per day

- Extreme decay and gamma risk

- Large price moves = large P&L swings

- Only for experienced traders

0-3 DTE (Expiration Week):

- Theta decay: ~0.40-1.00 per day

- Maximum gamma exposure

- Avoid unless expert in pin risk

- High stress, high risk

The 45-21 Strategy: Most Popular Among Wheel Traders

The most common wheel strategy approach is:

- Sell options at 45 DTE (collect good premium)

- Close at 50% profit, typically around 21 DTE (capture peak theta)

- Repeat (6-8 cycles per year)

Why This Works:

When you sell at 45 DTE and close at 21 DTE, you capture roughly 50% of the premium in the first 50% of the time. This happens because theta accelerates as you move from 45 to 21 DTE.

You're essentially harvesting the most efficient part of the decay curve and then starting fresh, avoiding the gamma risk and stress of expiration week.

Real Numbers Example:

You sell an AMD $120 put at 45 DTE for $400 premium:

- Day 1 (45 DTE): Sell for $400

- Day 12 (33 DTE): Option worth ~$280 (30% profit)

- Day 24 (21 DTE): Option worth ~$200 (50% profit) ← Close here

- Day 45 (0 DTE): Option worth $0 (100% profit) ← But you avoided expiration risk

By closing at $200, you realized $200 profit in 24 days. You can now redeploy that capital into a new 45 DTE trade, effectively compounding your returns.

Adjusting DTE for Different Market Conditions

Your DTE selection should adapt to the current market environment:

High Implied Volatility (IV Rank > 50):

- Target: 14-21 DTE

- Capture inflated premium before IV crush

- Shorter duration reduces exposure to volatility collapse

- Higher premium-per-day justifies shorter timeframe

Low Implied Volatility (IV Rank < 30):

- Target: 45-60 DTE

- Need longer timeframe to collect sufficient premium

- More time allows for mean reversion

- Premium-per-day is low, so extend duration

Normal Volatility (IV Rank 30-50):

- Target: 30-45 DTE

- Standard wheel strategy approach

- Balanced risk-reward

- Consistent with systematic strategy

Earnings Events:

- Before earnings: 30+ DTE if avoiding, 7-14 DTE if playing

- After earnings: Return to normal 30-45 DTE

- IV often elevated before earnings, then collapses after

- Decision depends on your risk tolerance

Strike Selection and Expiration: The Combined Decision

Expiration selection doesn't exist in isolation - it works in combination with your strike selection. These two decisions are interconnected and should be made together.

Delta-Expiration Relationship

The delta of your option (probability of finishing in-the-money) interacts with your expiration selection:

Conservative Strategy (0.10-0.20 delta):

- Optimal expiration: 45-60 DTE

- Lower delta = less premium

- Longer timeframe ensures sufficient premium

- Lower probability of assignment

- More capital efficient over time

Moderate Strategy (0.20-0.30 delta):

- Optimal expiration: 30-45 DTE

- Most common wheel strategy approach

- Balanced premium and assignment risk

- Sweet spot for most traders

- Good repeatable system

Aggressive Strategy (0.30-0.50 delta):

- Optimal expiration: 21-30 DTE

- Higher delta = more premium

- Shorter timeframe manages assignment risk

- Requires active monitoring

- Higher win rate on assignment outcomes

Premium-to-Risk Ratio Across Expirations

The amount of premium you collect relative to your risk changes with expiration:

Short Expirations (7-14 DTE):

- Premium: 1-2% of stock price

- Risk: Full stock assignment

- Ratio: Lower premium-to-risk

- Makes sense only in high IV

Medium Expirations (30-45 DTE):

- Premium: 2-4% of stock price

- Risk: Full stock assignment

- Ratio: Optimal premium-to-risk

- Best risk-adjusted returns

Long Expirations (60-90 DTE):

- Premium: 4-6% of stock price

- Risk: Full stock assignment

- Ratio: Good premium-to-risk, but capital tied up longer

- Lower capital efficiency

Example Comparison (AMD at $120):

7 DTE, $115 strike (0.25 delta):

- Premium: $85 (0.71% of stock price)

- Risk: $11,500 capital commitment

- Return if successful: 0.74% in 7 days

45 DTE, $115 strike (0.30 delta):

- Premium: $350 (2.9% of stock price)

- Risk: $11,500 capital commitment

- Return if successful: 3.0% in 45 days (or 1.5% in 24 days if closed at 50%)

90 DTE, $115 strike (0.35 delta):

- Premium: $580 (4.8% of stock price)

- Risk: $11,500 capital commitment

- Return if successful: 5.0% in 90 days

The 45 DTE option offers the best annualized return when you factor in the 50% profit-taking rule and capital redeployment.

Advanced Expiration Selection Strategies

Once you master the basics, these advanced techniques can optimize your wheel strategy returns.

The Rolling Expiration Ladder

Instead of entering all positions at the same expiration, stagger them across multiple expiration cycles:

Example Portfolio:

- Week 1: Open AMD 45 DTE put

- Week 2: Open NVDA 45 DTE put

- Week 3: Open PLTR 45 DTE put

- Week 4: Open TSLA 45 DTE put

This creates a rolling ladder where positions mature at different times, providing:

- Regular opportunities to redeploy capital

- Reduced concentration risk

- Consistent monthly cash flow

- Natural diversification across time

Managing multiple expirations becomes complex with 10+ positions. After tracking three different expiration cycles manually in spreadsheets, I realized I needed better position management. QuantWheel's calendar view shows exactly which positions need attention each week, automatically tracking DTE across your entire portfolio so you never miss an optimal closing opportunity.

Seasonal Expiration Adjustments

Volatility patterns change throughout the year, requiring expiration adjustments:

January-March (Tax Season):

- Often lower volatility

- Target: 45-60 DTE for sufficient premium

- More capital preservation focus

April-August (Summer Doldrums):

- Typically low volatility

- Target: 30-45 DTE standard approach

- Selective stock picking matters more

September-October (Volatility Season):

- Historically higher volatility

- Target: 14-30 DTE to capture elevated premium

- More frequent monitoring needed

November-December (Holiday Season):

- Mixed volatility

- Target: 30-45 DTE for post-holiday deployment

- Consider tax-loss harvesting implications

Earnings-Aware Expiration Selection

Earnings announcements create volatility spikes that affect expiration selection:

Avoiding Earnings (Conservative):

- Check earnings calendar before trade

- Select expiration that expires BEFORE earnings

- Or choose expiration well AFTER earnings (30+ days post-earnings)

- Avoids IV crush and large price moves

Playing Earnings (Aggressive):

- Sell options 7-14 DTE before earnings

- Collect inflated premium from elevated IV

- Close immediately after earnings announcement

- Requires strong conviction in stock stability

Real Example - NVDA Earnings Play:

NVDA announces earnings in 10 days:

Conservative Approach:

- Sell 7 DTE put (expires before earnings)

- Or sell 45 DTE put (earnings in rear-view)

- Avoids earnings volatility completely

Aggressive Approach:

- Sell 14 DTE put with earnings in middle

- Collect 60% higher premium from elevated IV

- Plan to close immediately after earnings

- Accept higher risk for higher reward

The "Widow Maker" Expirations to Avoid

Some expiration dates carry unique risks that wheel traders should understand:

Monthly OpEx Week (Third Friday):

- Highest trading volume

- Potential for pin risk (stock pinned to strike)

- Market makers defending positions

- Can create unusual price action

Major Holiday Weeks:

- Low liquidity

- Wider bid-ask spreads

- Unpredictable price moves

- Better to close early and wait

FOMC Announcement Weeks:

- Federal Reserve meeting dates

- Extreme volatility potential

- Consider closing positions before announcement

- Or extend expiration past the event

Quadruple Witching (Quarterly):

- Stock index futures, options, and single stock futures expire

- March, June, September, December

- Increased volatility and volume

- Price action can be erratic

Managing Expiration Selection Across Multiple Positions

As your wheel strategy portfolio grows, managing different expirations becomes increasingly complex. Here's how to stay organized.

Position Sizing Across Expirations

Allocate your capital across different expiration timeframes:

Example $50,000 Portfolio:

- 60% in 30-45 DTE positions ($30,000)

- 25% in 45-60 DTE positions ($12,500)

- 15% in 14-21 DTE opportunistic positions ($7,500)

This diversification ensures:

- Regular capital availability for new opportunities

- Reduced correlation between positions

- Consistent monthly closing opportunities

- Flexibility for market changes

The Expiration Calendar System

Create a visual system to track upcoming expirations:

Week-by-Week View:

- Week 1: AMD (19 DTE), PLTR (25 DTE)

- Week 2: NVDA (12 DTE), TSLA (18 DTE)

- Week 3: SPY (9 DTE), QQQ (15 DTE)

- Week 4: New positions opening

This calendar approach helps you:

- Visualize position maturity

- Plan closing dates in advance

- Identify heavy workload weeks

- Balance position management time

When I was managing 15+ wheel positions across different expirations, I lost track of my AMD position that was at 80% profit at 8 DTE. By the time I noticed three days later, it had reversed and I gave back half my gains. That's when I realized manual tracking wasn't scalable. QuantWheel's alert system now notifies me when any position hits my profit target, regardless of which expiration cycle it's in.

Optimizing Management Time

Different expirations require different time commitments:

Weekly Options (5-7 DTE):

- Check daily

- 10-15 minutes per day

- Higher stress level

- Best for 3-5 positions maximum

Monthly Options (30-45 DTE):

- Check 2-3x per week

- 20-30 minutes per session

- Lower stress level

- Scalable to 10-15 positions

Longer Options (60+ DTE):

- Check weekly

- 15-20 minutes per week

- Minimal stress

- Set-and-forget approach

Choose your expiration strategy based on the time you can realistically commit. Burnout is real, and managing too many short-term positions will lead to mistakes.

Tax Implications of Expiration Selection

Expiration selection affects your tax situation more than most traders realize.

Short-Term vs Long-Term Capital Gains

Options held less than 1 year are taxed as short-term capital gains (ordinary income rate), regardless of the underlying holding period.

Weekly/Monthly Options:

- Always short-term gains

- Taxed at ordinary income rates (up to 37%)

- More frequent transactions = more taxable events

- Consider tax-loss harvesting opportunities

Longer Expirations (60-90 DTE):

- Still short-term gains

- Fewer taxable events per year

- Slightly more tax efficient

- Less transaction cost impact

Assignment and Tax Considerations

When you get assigned, your expiration selection affects cost basis:

Example - Premium and Cost Basis:

You sell a $100 strike put for $3 premium with 45 DTE:

- Assignment happens at expiration

- Your cost basis: $97 per share ($100 - $3 premium)

- This $97 basis determines future capital gains

Your broker shows $100 cost basis, but your real basis is $97. Tracking this through multiple wheel cycles becomes critical for accurate tax reporting. QuantWheel automatically adjusts your cost basis when assignments happen, tracking your real breakeven through CSP → assignment → covered call → exit. Come tax season, you have accurate records instead of trying to reconstruct months of premium adjustments.

Wash Sale Rules and Expiration Selection

Shorter expirations increase wash sale risk:

Wash Sale Definition: If you sell a stock at a loss and repurchase it (or a substantially identical security) within 30 days, you cannot claim the loss for tax purposes.

How Expiration Affects This:

- Weekly expirations = more frequent trades = higher wash sale risk

- Monthly expirations = fewer trades = easier to manage wash sales

- Be careful closing losing positions and reopening immediately

Strategy to Avoid Wash Sales:

- Wait 31 days before re-entering the same underlying

- Trade similar but different underlyings (rotate stocks)

- Use longer expirations to reduce trade frequency

- Keep detailed records of all transactions

Common Expiration Selection Mistakes

Learn from these common errors that cost wheel traders thousands in potential profits.

Mistake #1: Always Using the Same Expiration

The Error: Selling 45 DTE every single time regardless of market conditions.

Why It's Wrong: Market conditions change. High IV environments favor shorter expirations to capture premium before IV crush. Low IV environments require longer expirations to collect sufficient premium.

The Fix: Adjust your DTE based on IV rank:

- IV Rank < 30: Use 45-60 DTE

- IV Rank 30-50: Use 30-45 DTE

- IV Rank > 50: Use 14-30 DTE

Mistake #2: Holding to Expiration

The Error: Selling options and always holding until expiration day for "maximum profit."

Why It's Wrong: The last 2 weeks before expiration carry massive gamma risk with minimal additional theta decay reward. A single large move against you can wipe out weeks of gains.

The Fix: Close at 50-70% profit, typically around 21 DTE. Redeploy capital into new positions. You capture the best part of theta decay while avoiding expiration week risk.

Mistake #3: Selling Too Short Without Time to Manage

The Error: Selling 7 DTE options every week because "the theta is highest."

Why It's Wrong: Short expirations require constant attention. Miss one week of management and a position can blow up. Transaction costs accumulate. Stress and burnout are real.

The Fix: Only trade weekly options if you have genuine time for daily management. Most part-time traders should stick to 30-45 DTE for sustainable, lower-stress trading.

Mistake #4: Ignoring Earnings Calendar

The Error: Selling a 30 DTE option without checking if earnings is in 15 days.

Why It's Wrong: Earnings create massive volatility and IV crush. Your position can move against you dramatically overnight, or IV collapse eliminates closing opportunities at your profit target.

The Fix: Always check the earnings calendar before opening a position. Decide whether you're playing earnings (aggressive) or avoiding it (conservative). Select your expiration accordingly.

Mistake #5: Poor Record Keeping Across Expirations

The Error: Not tracking which positions expire when, missing profit-taking opportunities.

Why It's Wrong: With 10+ positions across different expirations, manual tracking fails. You miss optimal closing points, hold too long, or close too early. Your actual returns suffer.

The Fix: Implement a systematic tracking system. Whether it's a detailed spreadsheet or a platform like QuantWheel that automates expiration tracking, you need visibility into every position's DTE and P&L at all times.

Tools and Resources for Expiration Selection

The right tools make expiration selection easier and more profitable.

Option Chain Analysis

Understanding how to read option chains for different expirations:

Key Metrics to Compare:

- Premium collected (absolute dollars)

- Premium as % of stock price

- Theta (daily decay)

- Open interest (liquidity)

- Bid-ask spread (transaction cost)

What to Look For:

- Consistent open interest (shows liquidity)

- Tight bid-ask spreads (reduces friction)

- Reasonable premium for risk taken

- Appropriate delta for your strategy

Theta Decay Calculators

Use theta calculators to visualize decay across different expirations:

Inputs Needed:

- Current stock price

- Strike price

- Days to expiration

- Implied volatility

- Interest rates

Outputs to Analyze:

- Expected theta decay per day

- Projected option value at various dates

- Break-even scenarios

- Profit targets with timeframes

IV Rank and Percentile Tools

IV rank helps you adjust your expiration selection:

IV Rank Formula: (Current IV - 52-week low IV) / (52-week high IV - 52-week low IV) × 100

How to Use for Expiration Selection:

- IV Rank 0-20: Extend to 45-60 DTE

- IV Rank 20-40: Standard 30-45 DTE

- IV Rank 40-60: Consider 21-30 DTE

- IV Rank 60-80: Shorter 14-21 DTE

- IV Rank 80-100: Very short 7-14 DTE

Building Your Personal Expiration Selection Framework

Create a systematic approach that matches your lifestyle and trading goals.

Step 1: Define Your Time Commitment

Questions to Answer:

- How much time do I have for trading per day?

- Can I check positions during market hours?

- Do I want this to be my full-time focus or side income?

- What's my stress tolerance for active management?

Time-Based Recommendations:

- 10-15 min/day: Stick to 45-60 DTE

- 30 min/day: Use 30-45 DTE comfortably

- 1+ hour/day: Can manage 14-30 DTE or weekly options

- Full-time: All expiration ranges available

Step 2: Set Your Return Targets

Realistic Expectations:

- Conservative (45-60 DTE): 8-12% annual return

- Moderate (30-45 DTE): 12-18% annual return

- Aggressive (14-21 DTE): 18-25% annual return

- Very Aggressive (Weekly): 25-35% annual return (with high risk/stress)

Choose the expiration strategy that aligns with your target returns while matching your time commitment and risk tolerance.

Step 3: Create Your Expiration Rules

Example Rule Set:

Normal Market Conditions (IV Rank 30-50):

- Default to 30-45 DTE

- Close at 50% profit around 21 DTE

- 6-8 trades per position per year

High Volatility (IV Rank > 50):

- Shorten to 14-30 DTE

- Capture elevated premium before IV crush

- Close at 50% profit or after volatility event

Low Volatility (IV Rank < 30):

- Extend to 45-60 DTE

- Need longer timeframe for sufficient premium

- Close at 60% profit to justify longer hold

Around Earnings:

- Conservative: Exit 5+ days before earnings

- Aggressive: Open 7-14 DTE before earnings, close immediately after

Step 4: Track and Optimize

Metrics to Monitor:

- Average holding period by expiration

- Win rate by expiration timeframe

- Average return per trade by expiration

- Time spent managing per expiration type

- Stress level (subjective but important)

Quarterly Review:

- Which expirations worked best?

- Which expirations caused the most stress?

- Are you achieving your return targets?

- Do you need to adjust your framework?

After six months of tracking results across different expirations, I realized my 21 DTE trades had the best risk-adjusted returns, but my manual spreadsheet couldn't give me that insight easily. QuantWheel's analytics dashboard now shows me exactly which expiration ranges perform best for my trading style, helping me continuously optimize my approach.

Real-World Examples: Expiration Selection in Action

Let's look at how experienced wheel traders apply expiration selection principles.

Example 1: Conservative Income Seeker

Profile:

- Capital: $50,000

- Time: 30 min/day

- Goal: 10% annual return with low stress

Expiration Strategy:

- Uses exclusively 45 DTE options

- Targets 0.20 delta strikes

- Closes at 50-60% profit (~21-28 DTE)

- Manages 5-8 positions simultaneously

Typical Year:

- 8 trades per position × 5 positions = 40 total trades

- Average return per trade: 1.5% (after closing at 50% profit)

- Annual return: ~10-12%

- Time commitment: Manageable

- Stress level: Low

Example 2: Aggressive Growth Trader

Profile:

- Capital: $25,000

- Time: 1-2 hours/day

- Goal: 25% annual return, willing to accept higher stress

Expiration Strategy:

- Uses 14-21 DTE options primarily

- Targets 0.30 delta strikes

- Closes at 50% profit (~7-10 DTE)

- Manages 8-12 positions simultaneously

Typical Year:

- 15 trades per position × 8 positions = 120 total trades

- Average return per trade: 0.8%

- Annual return: ~20-25%

- Time commitment: Significant

- Stress level: High

Example 3: Balanced Hybrid Approach

Profile:

- Capital: $75,000

- Time: 45 min/day

- Goal: 15% annual return with moderate stress

Expiration Strategy:

- 70% in 30-45 DTE core positions

- 30% in 14-21 DTE tactical positions during high IV

- Targets 0.25 delta on core, 0.30 on tactical

- Closes core at 50% profit, tactical at 40-50%

Typical Year:

- Core: 8 trades × 6 positions = 48 trades

- Tactical: 12 trades × 3 positions = 36 trades

- Total: 84 trades

- Average return: ~1.2% per trade

- Annual return: ~14-16%

- Time commitment: Moderate

- Stress level: Medium

Conclusion: Your Expiration Selection Action Plan

Options expiration selection isn't a one-size-fits-all decision. The right expiration for you depends on your available time, risk tolerance, return goals, and current market conditions.

Key Takeaways:

- 30-45 DTE is the default sweet spot for most wheel traders, balancing theta decay efficiency with manageable risk

- Close at 50% profit around 21 DTE to capture peak theta while avoiding expiration week gamma risk

- Adjust for volatility: shorter in high IV environments, longer in low IV conditions

- Match expiration to your lifestyle: weekly options demand daily attention, monthly options work for part-time traders

- Avoid common mistakes: don't hold to expiration, don't ignore earnings, don't use the same expiration blindly

The most successful wheel traders develop a systematic expiration selection framework that matches their personal situation. They track results, adjust based on data, and continuously optimize their approach.

Start with 30-45 DTE if you're new to the wheel strategy. As you gain experience and data on your performance, adjust your expiration selection to maximize your risk-adjusted returns while maintaining a sustainable trading lifestyle.

The goal isn't to find the "perfect" expiration - it's to find the consistent, repeatable expiration strategy that you can execute week after week, month after month, without burning out. Boring consistency wins over aggressive optimization every time.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.