When you sell cash-secured puts or covered calls as part of the wheel strategy, you’re collecting premium. But that premium isn’t just one thing – it’s actually made up of two distinct components: intrinsic value and extrinsic value. Understanding the difference between these two types of value is essential for making smart decisions about when to close positions, roll options, or let them expire.

Start your free trial of QuantWheel →

This guide breaks down exactly what intrinsic and extrinsic value are, how they affect your wheel strategy trades, and how to use this knowledge to improve your trading decisions.

TL;DR: Intrinsic vs Extrinsic Value in Options

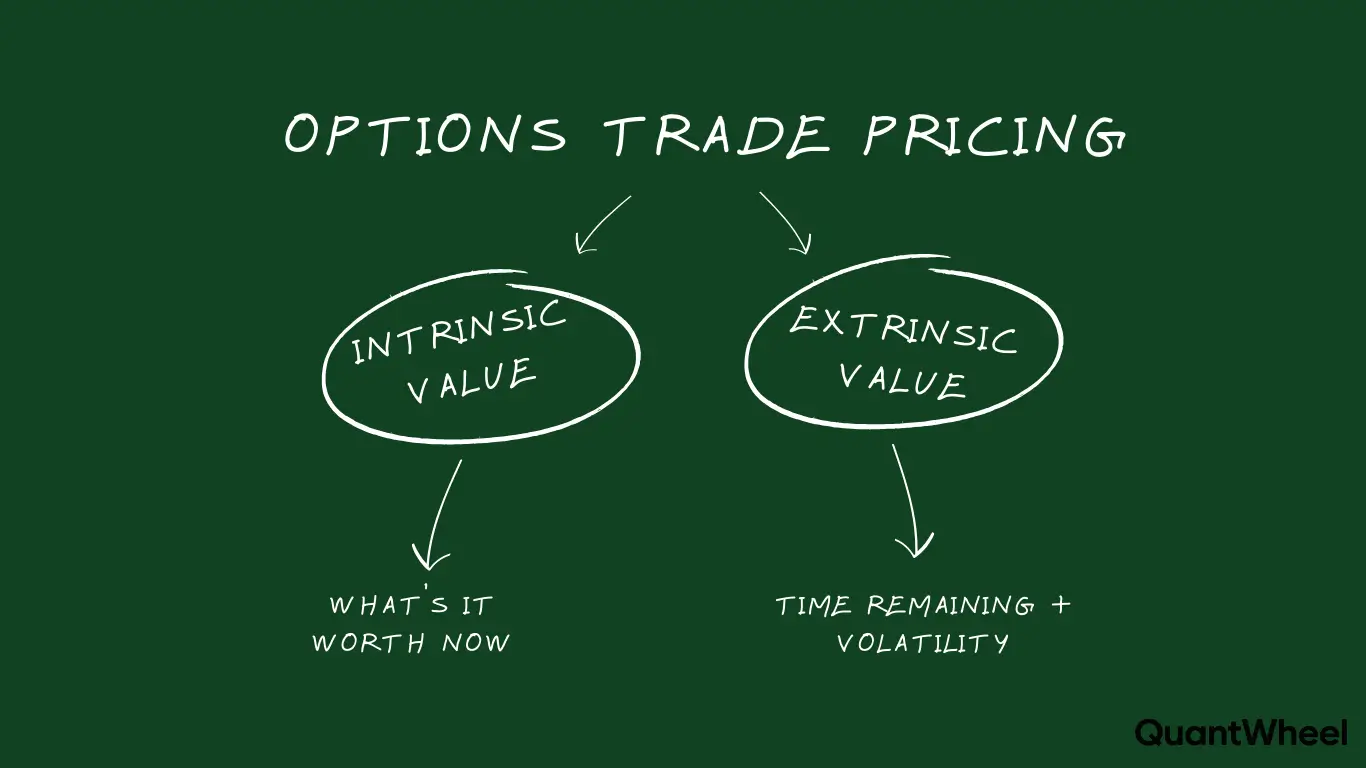

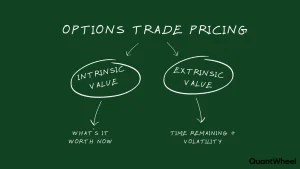

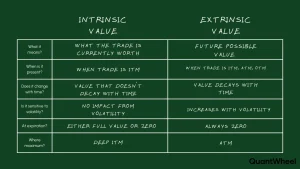

Intrinsic value is the real, immediate profit built into an option – the amount it’s already “in the money.” If you own a call option with a $50 strike and the stock is trading at $55, you have $5 of intrinsic value because you could exercise the option and immediately profit.

Extrinsic value (also called time value) is the extra premium beyond intrinsic value that traders pay for the possibility the option could become more valuable. This portion of an option’s price exists because there’s still time for the stock to move.

Simple example: You sell a cash-secured put with a $100 strike when the stock is at $105. The option trades for $3.00. Since the stock is above the strike, there’s zero intrinsic value (the option is out of the money). The entire $3.00 premium is extrinsic value – pure time value that will decay to zero by expiration if the stock stays above $100.

Key formula: Option Premium = Intrinsic Value + Extrinsic Value

For wheel strategy traders, this matters because you’re selling extrinsic value. Understanding how this value decays helps you maximize profit by closing positions early when you’ve captured most of the available premium, or rolling positions before extrinsic value disappears completely.

What Is Intrinsic Value in Options?

Intrinsic value represents the amount an option is “in the money” – the real, tangible value you could capture if you exercised the option right now.

How to Calculate Intrinsic Value

The calculation is straightforward:

For call options: Intrinsic Value = Stock Price – Strike Price (if positive, otherwise zero)

For put options: Intrinsic Value = Strike Price – Stock Price (if positive, otherwise zero)

Intrinsic Value Examples

Call option example:

- Stock price: $150

- Call strike: $140

- Intrinsic value: $150 – $140 = $10

The call is $10 in the money. If you exercised it, you’d buy stock at $140 and could immediately sell at $150 for a $10 profit per share.

Put option example:

- Stock price: $95

- Put strike: $100

- Intrinsic value: $100 – $95 = $5

The put is $5 in the money. If you exercised it, you’d sell stock at $100 when the market price is only $95.

Out of the money example:

- Stock price: $105

- Put strike: $100

- Intrinsic value: $0

The put is out of the money. There’s no benefit to exercising it, so intrinsic value is zero. This is the typical scenario for wheel strategy traders selling puts – you want the option to stay out of the money with zero intrinsic value.

Key Rules About Intrinsic Value

- Intrinsic value can never be negative – it’s either positive or zero

- Out-of-the-money options always have zero intrinsic value

- At-the-money options have zero intrinsic value (stock price equals strike)

- Only in-the-money options have intrinsic value greater than zero

- Intrinsic value doesn’t decay – it only changes when the stock price moves relative to the strike

For wheel strategy traders, you’re typically selling out-of-the-money options, which means you’re collecting premium that consists entirely of extrinsic value. This is by design – you want to avoid assignment and let the options expire worthless.

What Is Extrinsic Value in Options?

Extrinsic value, also called time value, is the portion of an option’s premium that exists beyond intrinsic value. It represents what traders are willing to pay for the possibility that the option could become more valuable before expiration.

What Creates Extrinsic Value?

Extrinsic value is influenced by several factors:

Time until expiration: The more time remaining, the more extrinsic value an option has. A 45-day option has significantly more extrinsic value than a 7-day option at the same strike. This is why wheel traders often sell 30-45 day options – there’s meaningful extrinsic value to collect.

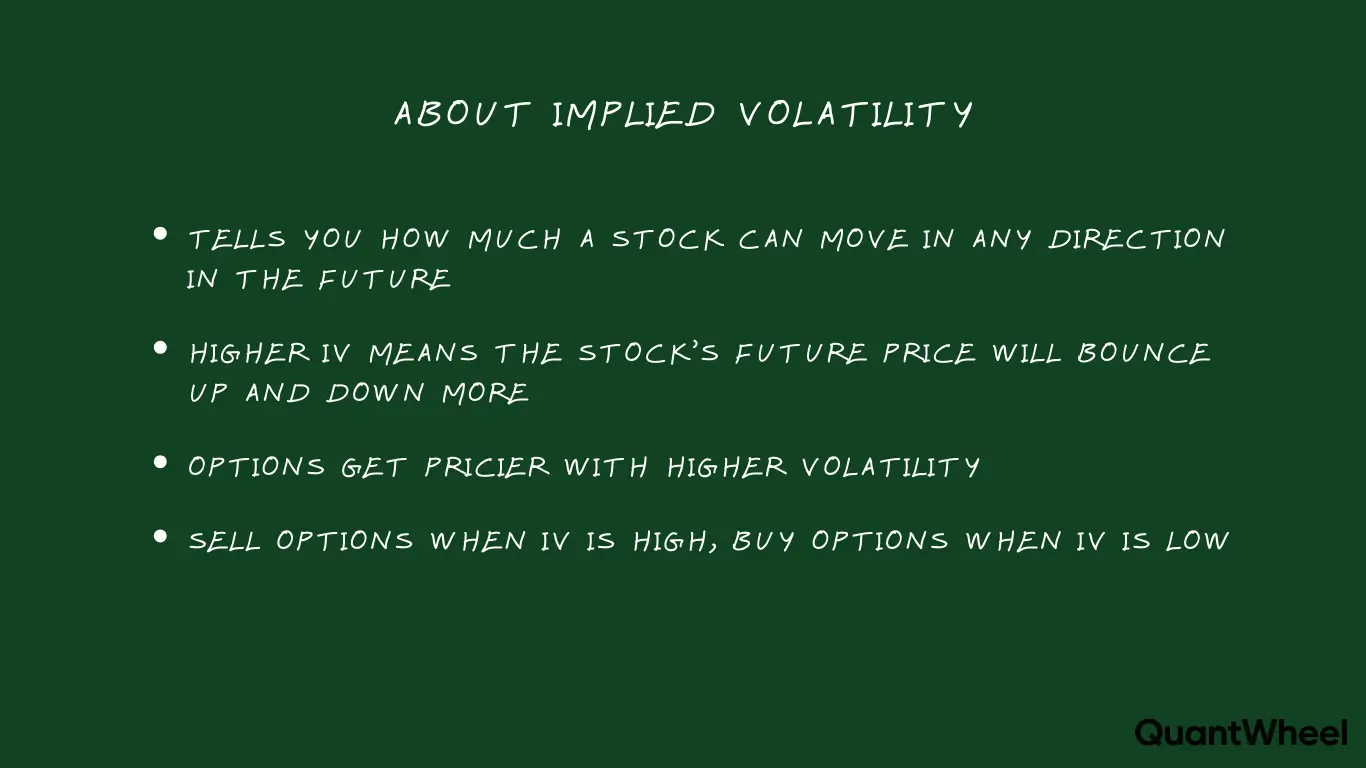

Implied volatility: When traders expect larger price swings (high implied volatility), extrinsic value increases. This is why selling options during high IV periods is attractive – you collect more premium for the same strike and expiration.

Distance from strike: At-the-money options have the maximum extrinsic value. As you move further in or out of the money, extrinsic value decreases. This creates the familiar options pricing curve.

Interest rates and dividends: These have minor effects on extrinsic value, but they’re less relevant for typical wheel strategy time frames.

How to Calculate Extrinsic Value

The formula is simple:

Extrinsic Value = Total Option Premium – Intrinsic Value

Extrinsic Value Examples

Example 1: Out-of-the-money put (typical wheel trade)

- Stock price: $105

- Put strike: $100

- Option price: $2.50

- Intrinsic value: $0 (out of the money)

- Extrinsic value: $2.50 – $0 = $2.50

The entire premium is extrinsic value. You’re collecting $250 per contract for selling time value. If the stock stays above $100 through expiration, this entire $2.50 decays to zero and you keep all the premium.

Example 2: In-the-money put

- Stock price: $95

- Put strike: $100

- Option price: $7.00

- Intrinsic value: $100 – $95 = $5.00

- Extrinsic value: $7.00 – $5.00 = $2.00

Even though the option is in the money, there’s still $2.00 of extrinsic value. This is the time value portion. As expiration approaches, this $2.00 will decay toward zero while the $5.00 intrinsic value remains (assuming the stock stays at $95).

Example 3: At-the-money call

- Stock price: $50

- Call strike: $50

- Option price: $3.80

- Intrinsic value: $0 (stock equals strike)

- Extrinsic value: $3.80 – $0 = $3.80

At-the-money options have maximum extrinsic value because there’s maximum uncertainty about whether they’ll expire in or out of the money. The entire $3.80 is time value.

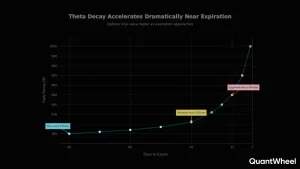

Extrinsic Value Decay (Theta Decay)

Here’s what wheel strategy traders need to understand: extrinsic value decays over time, and this decay accelerates as expiration approaches. This decay is called theta, and it’s what “theta gang” refers to.

Typical decay pattern:

- With 45 days until expiration: Slow, steady decay

- With 30 days until expiration: Decay accelerates

- With 21 days until expiration: Rapid decay begins

- With 7 days until expiration: Extremely rapid decay

- At expiration: All extrinsic value reaches zero

Many wheel traders target the 21-45 day window because this is where you can collect meaningful premium while benefiting from accelerating theta decay. Some traders close positions early when they’ve captured 50-80% of maximum profit, then open a new position to capture fresh extrinsic value rather than waiting for the final slow decay to zero.

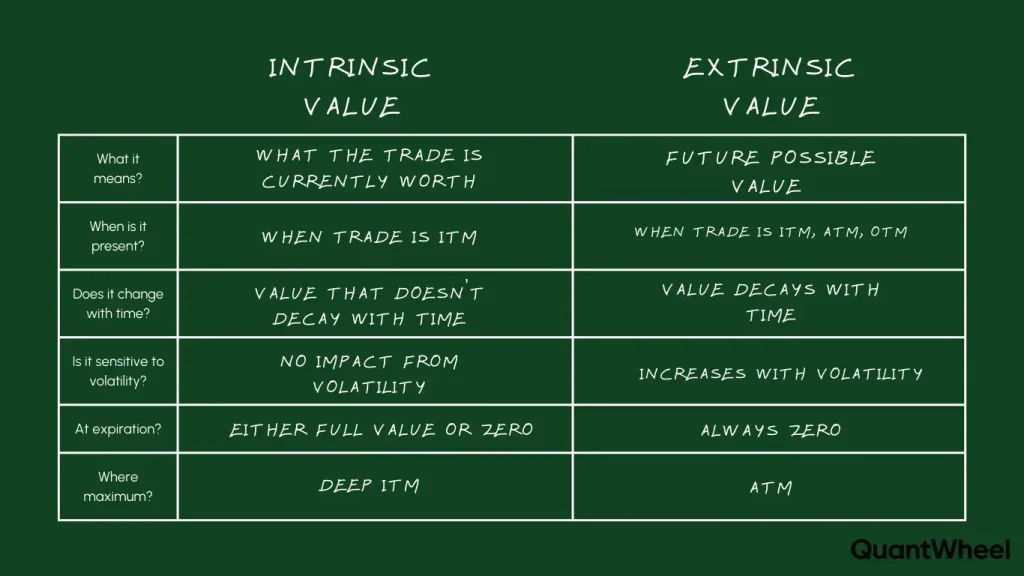

Intrinsic vs Extrinsic Value: Side-by-Side Comparison

| Feature | Intrinsic Value | Extrinsic Value |

|---|---|---|

| What it represents | Real profit if exercised now | Premium paid for future potential |

| Can it be zero? | Yes, for OTM options | Approaches zero near expiration |

| Does it decay? | No, only changes with stock movement | Yes, continuously decays (theta) |

| Maximum amount | Unlimited (no ceiling) | Highest at-the-money |

| At expiration | Remains if ITM | Always becomes zero |

| For OTM options | Always zero | Contains all the premium |

| For ITM options | Positive amount | Still exists until expiration |

| What creates it | Stock price vs strike difference | Time, volatility, uncertainty |

For wheel strategy traders, this comparison reveals why you’re primarily in the business of selling extrinsic value. You sell out-of-the-money options (zero intrinsic value) with 30-45 days of time remaining (maximum extrinsic value capture) and profit as that extrinsic value decays to zero.

How Intrinsic and Extrinsic Value Affect Your Wheel Strategy

Understanding the intrinsic/extrinsic split isn’t just academic – it directly impacts your trading decisions throughout the wheel cycle.

Selling Cash-Secured Puts

When you sell a cash-secured put in the wheel strategy, you’re typically targeting out-of-the-money strikes. This means zero intrinsic value and 100% extrinsic value in your collected premium.

Decision-making framework:

When considering early closes: If you’ve collected 50-70% of the maximum extrinsic value in the first few weeks, closing the position and opening a new one can be more profitable than waiting for the final 30-50% to decay slowly. QuantWheel tracks your profit percentage automatically, showing you when you’ve hit common profit-taking thresholds.

When the stock moves against you: If the stock drops toward your strike, the option gains intrinsic value. Understanding how much of the current premium is intrinsic (real value you’d need the stock to reverse) versus extrinsic (will decay with time) helps you decide whether to roll down, take assignment, or wait it out.

When choosing strikes: Strikes closer to the current stock price have more extrinsic value but higher assignment risk. Understanding this trade-off helps you select the right delta for your risk tolerance.

Managing Covered Calls

After assignment, you’re selling covered calls. Similar principles apply, but your goal is usually to collect premium while accepting the possibility of selling your shares.

Decision-making framework:

When the stock rallies: If your covered call moves in the money, most of its premium becomes intrinsic value. The remaining extrinsic value tells you how much extra premium holders are paying for time. If there’s very little extrinsic value left, you might choose to roll up and out to collect more extrinsic value rather than letting your shares get called away.

When to close early: Just like with puts, capturing 50-80% of a covered call’s maximum profit means you’ve collected most of the extrinsic value. The remaining profit happens slowly. Opening a new covered call with fresh extrinsic value can be more efficient.

When rolling positions: If you need to roll a covered call to avoid assignment, you’re essentially closing a position with little remaining extrinsic value and opening a new one with more extrinsic value. The net credit you receive is largely the difference in extrinsic value between the two positions.

Example: Full Wheel Cycle with Intrinsic/Extrinsic Analysis

Let’s walk through a complete wheel trade and see how these concepts apply at each decision point:

Step 1: Sell cash-secured put

- Stock: $105

- Sell $100 strike put, 35 days to expiration

- Collect $2.80 premium ($280 per contract)

- Intrinsic value: $0

- Extrinsic value: $2.80

Analysis: You’re collecting pure extrinsic value. Your breakeven is $97.20 ($100 strike minus $2.80 premium).

Step 2: Stock stays at $105, 14 days later

- Put now worth $0.80

- Intrinsic value: still $0

- Extrinsic value: $0.80

- Profit: $2.00 (71% of max profit)

Analysis: You’ve collected 71% of the extrinsic value in 40% of the time. Many traders would close here for $0.80, realizing $200 profit, then sell a new put with fresh extrinsic value rather than waiting 21 more days for the final $80.

Step 3: Stock drops to $98 (hypothetical scenario)

- Put now worth $3.20

- Intrinsic value: $100 – $98 = $2.00

- Extrinsic value: $3.20 – $2.00 = $1.20

Analysis: The option is now in the money. Of the $3.20 premium, $2.00 is real intrinsic value (the amount you’re underwater if assigned), and $1.20 is remaining extrinsic value. You have 21 days for $1.20 of extrinsic value to decay and possibly for the stock to recover. You need the stock back above $100 at expiration to avoid assignment.

Step 4: Stock recovers to $104, position expires

- Put expires worthless

- Intrinsic value: $0

- Extrinsic value: $0

- Total profit: $280

Analysis: All the extrinsic value you sold decayed to zero. The option never developed intrinsic value that would have forced assignment.

This example shows how monitoring intrinsic versus extrinsic value throughout a trade helps you make informed decisions about when to close, when to roll, and what outcomes to expect. QuantWheel automatically tracks your position’s current value and profit percentage, making it easy to spot when you’ve captured the majority of available extrinsic value.

Common Mistakes: Intrinsic and Extrinsic Value Edition

Understanding these concepts helps you avoid several common wheel strategy mistakes:

Mistake 1: Waiting for worthless expiration on deep ITM options

If your short put is significantly in the money near expiration, almost all remaining premium is intrinsic value with minimal extrinsic value. Waiting for expiration hoping for a miracle means you’re not getting paid (no extrinsic value to collect) while taking assignment risk. It’s often better to take assignment or roll the position to collect new extrinsic value.

Mistake 2: Not closing positions at 50-80% profit

Many beginners hold positions until expiration trying to capture 100% of the premium. But the final 20-50% is mostly extrinsic value that decays very slowly in the last week. Closing early and opening a new position with fresh extrinsic value often produces better returns. This is one of the most powerful techniques experienced wheel traders use.

Mistake 3: Selling far out-of-the-money options with too little extrinsic value

Selling a $90 put when the stock is at $110 might feel safe, but the extrinsic value is tiny because the option is so far out of the money. You’re taking up capital and accepting (small) risk for very little premium. Understanding the extrinsic value available at different strikes helps you find the sweet spot between safety and income.

Mistake 4: Ignoring implied volatility’s impact on extrinsic value

Implied volatility directly affects extrinsic value. Selling options when IV is very low means you’re collecting minimal extrinsic value. Waiting for higher IV periods, or at least being aware of current IV levels, helps you collect more premium for the same risk. Many wheel traders specifically target stocks with elevated IV to maximize extrinsic value collection.

Mistake 5: Not accounting for intrinsic value when rolling

When you roll a position, you’re buying back the current option and selling a new one. If the option you’re buying back has significant intrinsic value, you’re paying real money, not just recapturing time value. Understanding how much is intrinsic versus extrinsic helps you evaluate whether a roll makes financial sense or if taking assignment might be better.

Advanced Concepts: Intrinsic and Extrinsic Value

For traders who want to go deeper, here are some additional considerations:

Extrinsic Value Across Different Volatility Environments

The same option can have vastly different extrinsic value depending on implied volatility:

Low IV environment (15% implied volatility):

- Stock: $100

- 30-day ATM call: might be $1.50

- Almost all extrinsic value

- Less attractive for selling premium

High IV environment (50% implied volatility):

- Stock: $100

- 30-day ATM call: might be $5.00

- Still almost all extrinsic value

- Much more attractive for selling premium

Same stock, same strike, same expiration – but the extrinsic value triples in the high IV environment. This is why wheel traders often focus on stocks with elevated IV or wait for overall market volatility to increase before opening new positions.

The Extrinsic Value Curve

Extrinsic value isn’t distributed evenly across strikes. It follows a curve:

- Deep out-of-the-money: Very little extrinsic value (low probability of profit)

- Slightly out-of-the-money: Moderate extrinsic value (common wheel strategy target)

- At-the-money: Maximum extrinsic value (highest uncertainty)

- Slightly in-the-money: Still high extrinsic value, but now with intrinsic value too

- Deep in-the-money: Mostly intrinsic value, minimal extrinsic value

Understanding this curve helps you select strikes that balance premium collection with assignment risk.

Extrinsic Value and Earnings Announcements

Before earnings, options have inflated extrinsic value due to elevated implied volatility. After earnings (regardless of the stock’s movement), implied volatility crashes and extrinsic value collapses. This phenomenon is called “IV crush.”

Some wheel traders specifically sell options before earnings to capture the elevated extrinsic value, accepting the higher risk of large stock movements. Others avoid earnings entirely. There’s no right answer, but understanding that much of the pre-earnings premium is temporary extrinsic value helps you make informed decisions.

Intrinsic Value at Expiration: Assignment Mechanics

At expiration, all extrinsic value disappears. If your short put or call has any intrinsic value remaining (even $0.01), it will typically be exercised:

- Short put with intrinsic value: You’ll be assigned shares at the strike price

- Short call with intrinsic value: Your shares will be called away at the strike price

This is why the intrinsic/extrinsic split matters most as expiration approaches. You can estimate your assignment likelihood by whether the option has intrinsic value and how much extrinsic value provides a buffer.

Tools for Tracking Intrinsic and Extrinsic Value

While you can manually calculate intrinsic and extrinsic value for each position, having tools that automatically track these components makes wheel strategy trading much more manageable, especially when you’re running multiple positions simultaneously.

Manual Calculation Method

For each position:

- Check current stock price

- Calculate intrinsic value (stock price vs strike, minimum zero)

- Check current option price

- Subtract intrinsic from option price to get extrinsic value

- Track extrinsic value decay over time

- Decide on position management based on remaining value split

This works fine for one or two positions but becomes tedious as your wheel portfolio grows.

QuantWheel’s Approach

QuantWheel automatically tracks option values and calculates your profit percentage on each position, making it easy to spot when you’ve captured 50%, 70%, or more of maximum profit without manual calculations. The platform shows your current position value, helping you make informed decisions about early closes or rolls.

When you get assigned, QuantWheel automatically adjusts your cost basis to reflect the premium collected, solving one of the biggest pain points in wheel strategy tracking – knowing your real cost basis after assignment. This is critical for tax reporting and for deciding on covered call strikes.

For wheel traders managing 10, 15, or 20+ positions across multiple stocks, having this automation means you can focus on strategy and execution rather than spreadsheet maintenance.

Start your free trial of QuantWheel →

Practical Takeaways: Using Intrinsic and Extrinsic Value in Your Trading

Here’s how to apply these concepts immediately in your wheel strategy trading:

1. Check profit percentage regularly: When a position has captured 50-80% of max profit, you’ve collected most of the extrinsic value. Consider closing and opening a new position with fresh extrinsic value rather than waiting weeks for the final decay.

2. Target high IV stocks: Higher implied volatility means more extrinsic value for the same strike and expiration. You’re in the business of selling extrinsic value, so selling when it’s abundant improves your risk-reward ratio.

3. Focus on the 21-45 day window: This timeframe offers substantial extrinsic value to collect while benefiting from accelerating theta decay. Options too far out decay slowly; options too close have little value left to capture.

4. When in trouble, know what you’re paying: If you need to roll or close a losing position, understanding how much is intrinsic value (real loss) versus extrinsic value (remaining time value) helps you make smart decisions about whether to roll, take assignment, or close.

5. Don’t pay for intrinsic value unnecessarily: When rolling positions, try to roll to strikes and expirations where you’re collecting more extrinsic value than you’re paying to close the current position. Paying to close positions with high intrinsic value can be expensive.

6. Use at-the-money as a reference point: ATM options have maximum extrinsic value. When selecting strikes, you can mentally compare the extrinsic value at your chosen strike to the maximum available ATM to gauge if you’re getting paid appropriately for your risk.

7. Track extrinsic value decay rate: If a position’s extrinsic value is decaying faster than expected, you’re winning. If it’s staying stubbornly high or increasing (stock moving toward your strike), you might need to adjust your plan.

Understanding intrinsic versus extrinsic value transforms wheel strategy from “sell options and hope they expire worthless” to “systematically collect time value while managing real value risk.” It’s the difference between guessing and knowing why you’re making each trading decision.

Conclusion: Master the Components to Master the Strategy

The wheel strategy works because you’re systematically selling extrinsic value – time premium that will decay to zero if the stock stays above your put strike or below your call strike. Understanding the split between intrinsic value (real, immediate value) and extrinsic value (time-based premium) helps you make better decisions about position management, early closes, rolling, and assignment.

Every option premium you collect is some combination of these two values. As a wheel trader, you want to:

- Sell options with substantial extrinsic value (30-45 days, reasonable IV)

- Collect most of that extrinsic value efficiently (close at 50-80% profit)

- Avoid situations where you’re buying back high intrinsic value (losing positions)

- Let extrinsic value decay work in your favor through theta

The concepts are simple, but applying them consistently across multiple positions requires discipline and good tracking. Whether you’re using spreadsheets or a platform like QuantWheel, make sure you can quickly see your position values and profit percentages so you can spot opportunities to close early and redeploy capital into fresh extrinsic value.

Intrinsic and extrinsic value aren’t just theoretical concepts – they’re the practical foundation of every decision you make in the wheel strategy.

Start your free trial of QuantWheel →

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.