You own 100 shares of a stock that's been sitting in your account, and you've heard that selling covered calls can generate extra income from those shares. But when you look at the options chain on your broker's platform, the Greeks, strike prices, and expiration dates feel overwhelming.

Start your free trial of QuantWheel to find covered call trades easier and also track your covered calls automatically and get real-time alerts for optimal exit points.

Find trades easier with QuantWheel →

Here's the reality: selling a covered call is one of the most straightforward options strategies, but the terminology makes it seem more complex than it actually is. Once you understand the mechanics and walk through your first trade, you'll wonder why you waited so long to start.

This guide breaks down exactly how to sell a covered call, from the requirements and mechanics to execution and management. By the end, you'll have the confidence to execute your first covered call trade.

What Is a Covered Call? (TL;DR)

A covered call is an options strategy where you sell a call option on stock you already own, collecting premium income in exchange for capping your upside profit potential at the strike price.

Here's how it works in simple terms:

The Setup: You own 100 shares of XYZ stock trading at $50 per share ($5,000 total position).

The Trade: You sell one call option with a $55 strike price expiring in 30 days. Someone pays you $100 in premium for that option.

Three Possible Outcomes:

- Stock stays below $55: The option expires worthless. You keep your 100 shares + the $100 premium. You can sell another covered call next month.

- Stock goes above $55: Your shares get "called away" (sold) at $55. You keep the premium + the profit from $50 to $55 ($500 + $100 = $600 total profit, or 12% in one month).

- Stock drops below $50: You still own the shares and keep the premium, but the $100 premium only partially offsets your paper loss on the stock.

The Trade-Off: You collect income now (premium) but give up unlimited upside. If XYZ rallies to $75, your shares are sold at $55, and you miss the move from $55 to $75.

Why Traders Use It: Covered calls work best on stocks you're willing to sell at the strike price, in markets that are trading sideways or rising modestly. The premium you collect reduces your effective cost basis and provides income while you wait.

Why Sell Covered Calls?

Selling covered calls serves several strategic purposes for stock owners:

Generate Income from Stocks You Already Own. Instead of waiting passively for your stock to appreciate, selling covered calls creates immediate income through premium collection. This is particularly valuable during sideways or slow-moving markets where your stock isn't producing gains through price appreciation alone.

Reduce Your Cost Basis Over Time. Every premium you collect lowers your effective cost basis in the stock. If you bought shares at $50 and collect $1 per share in premium monthly, your cost basis drops to $49, then $48, then $47 over three months. This downside cushion accumulates over time, giving you more margin for error if the stock declines.

Create a Selling Plan with a Profit Target. Rather than hoping your stock reaches your target price, a covered call creates a structured exit. If you'd be happy selling your shares at $55, selling a covered call at the $55 strike means you'll either collect premium while waiting or sell at your target price plus the premium. Either outcome meets your objective.

Outperform Buy-and-Hold in Flat Markets. During periods when stocks trade sideways for weeks or months, covered calls consistently outperform passive holding. The premium you collect is real income, while buy-and-hold produces zero returns in flat markets.

The strategy has trade-offs. You cap your upside at the strike price, meaning you'll miss explosive rallies if they occur. You're also still exposed to downside risk if the stock drops significantly, though the premium provides a small cushion. These limitations make covered calls best suited for stocks you believe will trade sideways to moderately higher, not stocks you expect to rocket upward.

Requirements for Selling Covered Calls

Before you can sell your first covered call, you need to meet specific requirements:

Stock Ownership. You must own at least 100 shares of the underlying stock in your brokerage account. Covered calls are sold in contracts, with each contract covering 100 shares. If you own 200 shares, you can sell up to 2 covered calls. If you only own 75 shares, you cannot sell a covered call until you purchase at least 25 more shares.

Options Trading Approval. Your broker requires options trading approval before you can sell covered calls. Most brokers classify this as Level 1 or Level 2 options trading. The approval process typically involves completing an application where you disclose your investing experience, financial situation, and understanding of options risks. Approval is usually granted within 1-2 business days for most applicants.

Sufficient Knowledge. While brokers have approval requirements, true readiness requires understanding the mechanics, risks, and management decisions involved in covered calls. You should understand concepts like strike prices, expiration dates, premium, and assignment before risking real capital.

Appropriate Account Type. Covered calls can be sold in most account types including individual taxable accounts, IRAs, Roth IRAs, and margin accounts. However, some retirement account custodians have restrictions on options trading, so verify your specific account's capabilities.

Platform Access. You need a trading platform that allows options trading. Most modern brokerages offer this, though some charge per-contract commissions while others offer commission-free options trading. Platforms vary significantly in their options interfaces, from basic to advanced, so consider ease of use when choosing where to trade.

Step 1: Choose the Right Stock for Covered Calls

Not all stocks make good covered call candidates. Selecting the wrong underlying stock is one of the most common mistakes beginners make.

Look for Stocks You're Willing to Sell. This is the most important criterion. Before selling a covered call, ask yourself: "Would I be happy selling these shares at the strike price?" If the answer is no because you believe the stock could rally significantly or you want to hold it long-term regardless of price, don't sell a covered call. The strategy works best when you'd be satisfied with either outcome—keeping the premium or selling at the strike.

Favor Stable, Moderate-Volatility Stocks. The best covered call candidates typically have moderate volatility—high enough to generate meaningful premium but not so volatile that the stock frequently gaps beyond your strike price. Blue-chip stocks, dividend payers, and established companies in stable industries often work well. Tech stocks can work but require more active management due to their tendency for large moves.

Check Implied Volatility for Premium Potential. Higher implied volatility generates higher premium. Before selling a covered call, check the option premium as a percentage of the stock price. Premiums of 1-3% per month are typical targets. If you're only getting 0.3% per month, the juice might not be worth the squeeze. Conversely, extremely high IV might signal upcoming volatility you'd prefer to avoid.

Consider Earnings and Events. Avoid selling covered calls right before earnings announcements unless you intentionally want to capture elevated premium and accept the risk. Stocks can move 10-20% or more on earnings, potentially blowing through your strike price or causing significant losses on the stock. Check the earnings calendar before opening positions.

Liquidity Matters. Choose stocks with liquid options markets where the bid-ask spread is tight. Wide spreads mean you're giving up profit to market makers. As a rule of thumb, look for option spreads less than 10% of the bid price. Apple, Microsoft, and S&P 500 ETFs like SPY have excellent liquidity. Small-cap stocks often have wide spreads that erode profits.

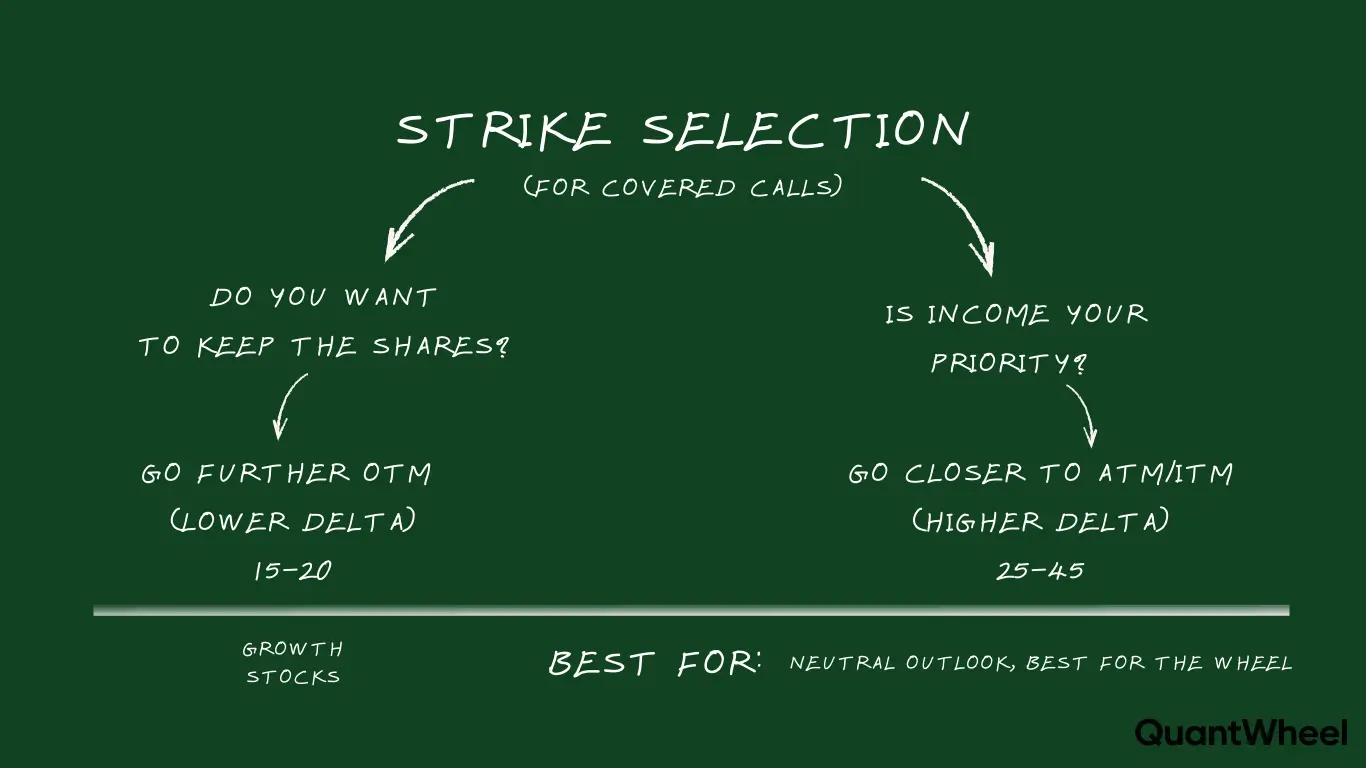

Step 2: Select Your Strike Price

The strike price you choose determines your risk-reward profile. This is where strategy meets personal preference.

Understanding the Trade-Off. Higher strike prices (further out-of-the-money) offer more upside potential but collect less premium. Lower strike prices (at-the-money or in-the-money) collect more premium but cap your profits sooner and increase the likelihood of assignment.

Out-of-the-Money (OTM) Strikes. Selling calls above the current stock price is the most common approach. For example, if your stock trades at $50, you might sell the $52 or $55 strike. This gives the stock room to appreciate while still generating income. The premium is lower than at-the-money strikes, but you keep any stock appreciation up to the strike price.

At-the-Money (ATM) Strikes. Selling calls at or very near the current stock price maximizes premium collection. If your stock is at $50, selling the $50 call generates the highest premium. However, even small upward moves result in assignment. This approach works when you're neutral to slightly bearish on the stock or when you specifically want to exit the position near current prices.

In-the-Money (ITM) Strikes. Selling calls below the current stock price generates even more premium but almost guarantees assignment at expiration. If your stock is at $50 and you sell the $45 call, you're essentially committing to sell your shares at $45 plus keeping the substantial premium. This is less common for covered calls but can work if you want to exit a position while collecting maximum premium.

Practical Strike Selection Strategy. A balanced approach is to sell strikes 2-5% above the current stock price with 30-45 days to expiration. This typically generates 1-2% premium while allowing reasonable room for stock appreciation. If the stock is at $50, consider the $51-$53 strikes. Adjust based on your outlook—bullish traders go further OTM, neutral traders go closer ATM.

The Delta Shortcut. Option delta indicates the probability of the option expiring in-the-money.

A 0.30 delta call has roughly a 30% chance of being in-the-money at expiration. Many covered call sellers target the 0.20-0.30 delta range as a balance between premium collection and assignment probability. Your broker's platform shows delta for each strike.

Step 3: Choose Your Expiration Date

Time until expiration significantly impacts your premium and management flexibility.

Monthly Expirations (30-45 Days). Standard monthly expiration dates are the most liquid and offer a good balance between premium collection and time commitment. Selling 30-45 day options and repeating monthly is a common rhythm for covered call sellers. This provides about 12 opportunities per year to collect premium and adjust your strategy based on market conditions.

Weekly Expirations (7-10 Days). Some traders prefer weekly expirations to collect premium more frequently and maintain flexibility. While individual weekly premiums are smaller, selling 4 weeklies in a month can sometimes generate more total premium than one monthly. However, this requires more active management and incurs more transaction costs. Weeklies work well for experienced traders in liquid stocks.

Longer-Term Expirations (60-90 Days). Selling calls with more time generates higher absolute premium but lower premium per day. Some traders use this approach to reduce management frequency and trading costs. The trade-off is being committed to a strike price for longer, reducing your ability to adjust to changing market conditions.

The Time Decay Factor. Option premium decays over time, with the most rapid decay occurring in the final 30 days before expiration. This is why 30-45 day expirations are popular—you capture the accelerating time decay period. Options with 60+ days to expiration decay more slowly in the early weeks, meaning you're waiting longer for premium to accumulate.

Match Timeframe to Your Outlook. If you have a specific one-month view on a stock, sell the monthly expiration. If you're uncertain about the near-term but confident in your medium-term outlook, longer expirations provide more breathing room. Shorter expirations suit traders who want to actively respond to market changes.

Standard Recommendation for Beginners. Start with 5-15 day expirations until you develop a feel for time decay, strike selection, and management. Once comfortable, experiment with weeklies or longer terms based on your preferences and the specific stock's behavior.

Find Covered Call opportunities that fit you inside QuantWheel →

Step 4: Execute the Trade on Your Broker Platform

Once you've selected your stock, strike price, and expiration, it's time to place the trade. The exact steps vary by broker, but the core process is similar.

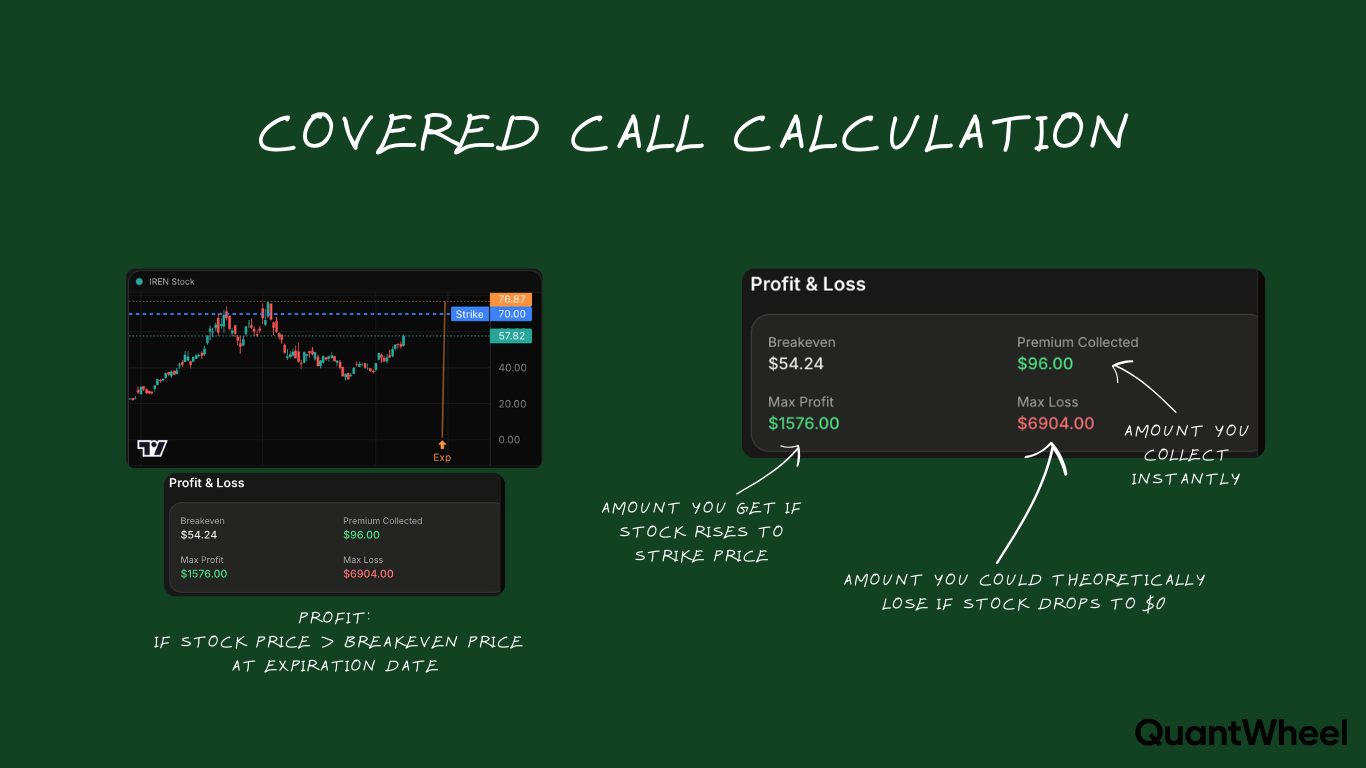

Navigate to the Options Chain. In your broker's platform, pull up the stock's options chain. This displays all available strike prices and expiration dates with their corresponding bid/ask prices. Look for the expiration date you selected (e.g., 30 days out) and find the strike price you want to sell.

Select "Sell to Open" a Call Option. The order type is critical. You're selling to open a position, not buying. In most platforms, you'll select "Sell" or "Sell to Open" for a call option. Do not select "Buy to Open"—that's the opposite trade. You're the premium collector, not the premium payer.

Choose Your Order Type. For beginners, a limit order is recommended over a market order. With a limit order, you specify the minimum premium you're willing to accept. For example, if the call's bid is $1.20 and ask is $1.25, you might place a limit order at $1.22. This ensures you don't get filled at an unfavorable price. Market orders can result in worse fills, especially in stocks with wider bid-ask spreads.

Specify Quantity. One contract covers 100 shares. If you own 100 shares, sell 1 contract. If you own 300 shares, you can sell up to 3 contracts. Never sell more contracts than you have shares to cover—that would be a naked call, which carries unlimited risk and requires higher-level options approval.

Review Your Order Details. Before submitting, verify: stock symbol, expiration date, strike price, call (not put), sell to open, number of contracts, limit price, and that it's matched with your existing shares. A wrong input here can result in costly mistakes.

Submit and Confirm Execution. After submitting, you'll receive a fill confirmation showing the exact premium per share you received. Options premium is quoted per share, so a $1.20 premium means $120 per contract (100 shares × $1.20). This premium is immediately credited to your account and is yours to keep regardless of what happens next.

Example Trade Execution. You own 200 shares of XYZ trading at $50. You decide to sell 2 covered calls at the $52 strike expiring in 35 days. The bid is $1.10, ask is $1.15. You place a limit order to sell 2 contracts at $1.12. The order fills at $1.13. You receive $226 total premium ($1.13 × 100 shares × 2 contracts), credited immediately to your account.

Step 5: Monitor and Manage Your Position

After selling your covered call, your work isn't done. Active management can significantly improve your results.

Track Stock Price Relative to Strike. Your primary monitoring task is watching where the stock trades relative to your strike price. If the stock stays well below your strike, you're on track to keep the shares and the premium. If the stock approaches or exceeds your strike, you need to decide whether to let assignment happen or take action.

Consider Closing Early at 50-80% Profit. Many experienced traders don't hold covered calls until expiration. When the option loses 50-80% of its value, they buy it back (close the position) and either sell a new call or wait. For example, if you sold a call for $1.00 and it's now worth $0.20, you can buy it back for $0.20, locking in $0.80 profit. This frees you to sell another call with more time value, potentially generating more total premium than waiting for expiration.

Rolling Up and Out When Threatened. If your stock rallies toward your strike and you want to keep the shares, you can "roll" the covered call. This means buying back the current call and simultaneously selling a new call at a higher strike or later expiration (or both). You collect a credit for the roll, keeping your shares while extending the position. Rolling is most effective when done before the option goes deep in-the-money.

Accept Assignment When Appropriate. If your stock blows through your strike price and assignment is inevitable, sometimes the best move is to accept it. You achieved your profit target (strike price + premium), and forcing a roll might commit you to a position you no longer want. Remember: assignment is not a failure—it's selling your stock at your predetermined target price.

Set Alerts for Key Price Levels. Rather than checking positions constantly, set price alerts on your phone or within your broker's platform. For example, if you sold a $55 call on a $50 stock, set an alert at $54. This notifies you when the position needs attention without requiring constant monitoring.

Managing in Different Scenarios. If the stock drops significantly below your strike, you can either wait for expiration (keeping the premium) or sell a new call at a lower strike on the same position. If the stock trades sideways near your strike, waiting for expiration and collecting full premium is usually optimal. If the stock rallies strongly and you want to keep it, rolling up and out extends your position.

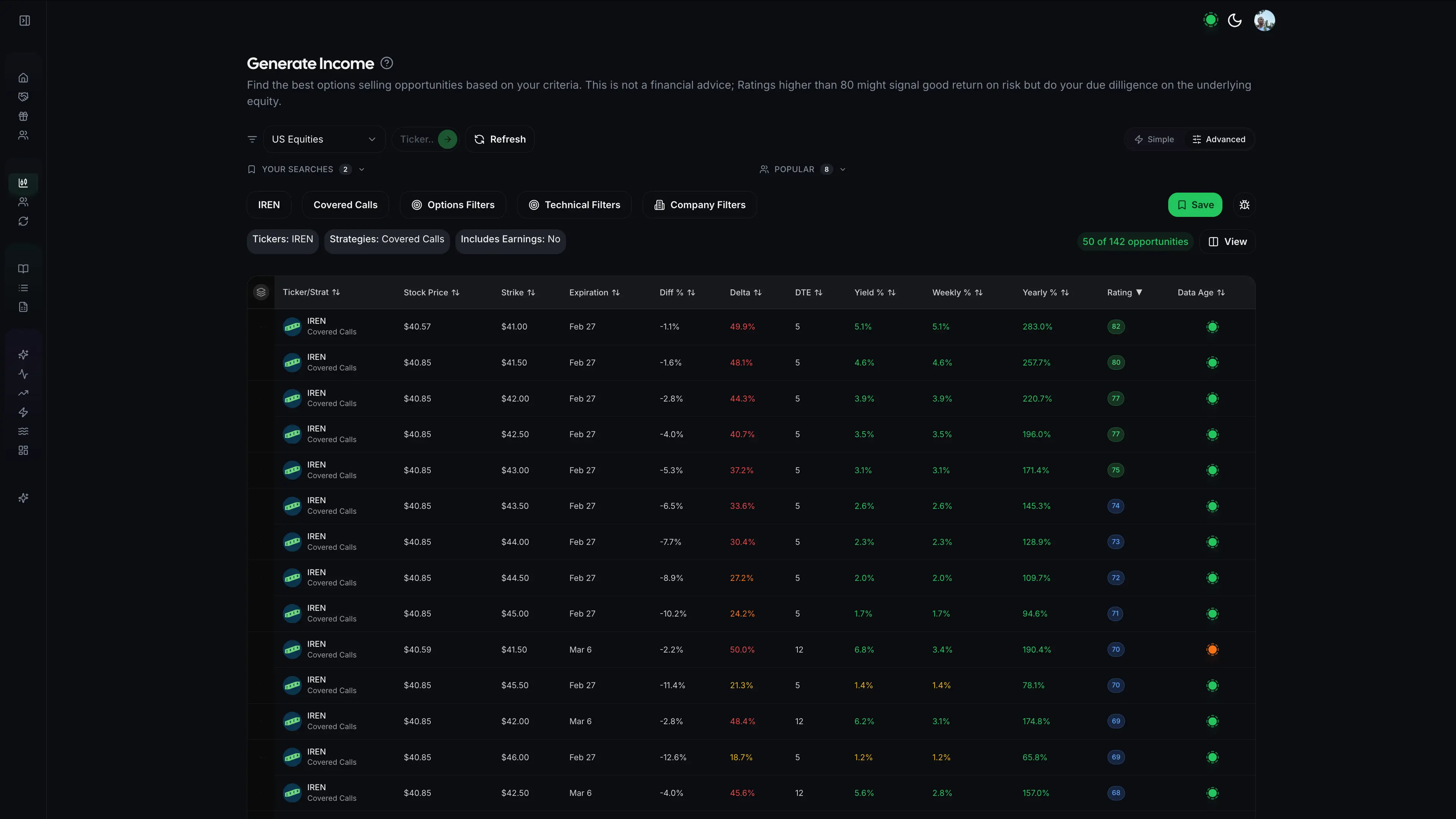

Tools for Tracking. Manual tracking in spreadsheets becomes challenging with multiple covered call positions. Here's where most traders struggle: calculating cost basis adjustments after assignments, tracking which positions need attention, and remembering your rules across multiple tickers. This is exactly why traders use tools like QuantWheel to automate position tracking, cost basis adjustments, and alerts for when to close or roll positions.

Create a full trading system inside QuantWheel →

Finding trades ->managing trades (alerts) -> help with rolling trades -> journaling trades.

Common Mistakes to Avoid When Selling Covered Calls

Even with a solid understanding of the mechanics, certain mistakes trip up new covered call sellers.

Selling Calls on Stocks You Desperately Want to Keep. The fastest way to regret a covered call is selling one on a stock you love and never want to sell, only to watch it rally and get called away. If you're emotionally attached to a position or believe it has significant upside, don't cap that upside with a covered call. The premium isn't worth the frustration of giving up a winner.

Ignoring Earnings Dates. Selling a covered call that expires just after earnings without realizing it is a classic beginner mistake. Stocks can move 10-30% on earnings. If you sell a covered call and earnings cause a huge rally, your shares are gone at the strike. If earnings cause a crash, the small premium doesn't offset the stock loss. Always check earnings dates before selling covered calls.

Chasing High Premium Without Questioning Why. If a stock's options are paying unusually high premium—say 5% per month when similar stocks pay 1-2%—ask why. High premium usually signals high risk: upcoming earnings, FDA announcements, legal issues, or extreme volatility. Sometimes the premium is justified, but often you're being paid to take on risk you haven't fully assessed.

Selling Too Far In-the-Money. New traders sometimes see huge premium on in-the-money calls and sell them without understanding that assignment is almost certain. If your stock is at $50 and you sell the $45 call for $6, yes, you collected $6, but your shares are already $5 in-the-money. You'll likely be assigned, and you've just committed to selling at $45 when the market is at $50. This rarely makes sense unless you specifically want to exit the position.

Forgetting About Cost Basis and Taxes. When your covered call gets assigned, you're selling stock, which triggers a taxable event. If you bought the shares 11 months ago and they get called away, that's a short-term capital gain taxed at your ordinary income rate. If you'd waited one more month for long-term treatment, you'd pay lower taxes. Factor holding periods into your strike and expiration selection.

Not Tracking Cost Basis After Assignment. Here's where it gets complicated: if you get assigned and immediately want to run the wheel strategy (sell cash-secured puts to buy the stock back, then sell covered calls again), your cost basis calculation becomes critical. Your broker shows the assignment price, but your real cost basis includes all the premiums collected through the full cycle. Missing this calculation leads to poor decision-making on future strikes. Most traders handle this manually in spreadsheets—or they use QuantWheel, which automatically adjusts cost basis through assignments and full wheel cycles.

Selling Calls with Insufficient Liquidity. If you sell a covered call on a thinly-traded stock with wide bid-ask spreads, you'll lose money to the spread when entering and again when exiting. If the bid-ask spread is $0.30 wide on a $1.00 option, you're giving up 30% of your premium to market makers. Stick to liquid underlying stocks with tight option spreads.

When to Close Your Covered Call Early

You don't have to hold covered calls until expiration. Many experienced traders close positions early to lock in profits and free up capital for new opportunities.

The 50% Rule. A widely-followed guideline is to buy back your covered call when it's lost 50% of its value. If you sold a call for $1.00 and it's now worth $0.50, you've captured half the maximum profit. By closing here and selling a new call, you potentially generate more total premium than holding the original call to expiration. Time decay slows dramatically in the final weeks, making early closes attractive.

When the Stock Pulls Back Sharply. If your stock drops significantly and your covered call becomes worth very little, buying it back locks in profit and frees you to make a new decision. You can sell a new call at a lower strike that's more realistic given the stock's new price, generating fresh premium rather than waiting for the original call to expire worthless.

When You Want to Participate in Upside. If news breaks or the stock starts rallying strongly and you believe there's significant further upside, you can buy back the covered call (at a loss if it's now in-the-money) to remove the upside cap. You give back some or all of your premium, but you're now free to participate in the rally. This is a strategic choice: take a small loss on the option to potentially capture a larger gain on the stock.

Rolling vs. Closing. Closing a position means buying back the call and being done with it. Rolling means buying back the current call and simultaneously selling a new one at a different strike or expiration. Rolling extends your position while collecting additional premium. Closing completely frees you from the obligation. Choose based on whether you want to stay engaged with covered calls on that stock or not.

The Math of Early Closing. When you sell a covered call for $1.00, your maximum profit is $1.00. If the call drops to $0.20, you can close for $0.80 profit, keeping 80% of max profit. If you held to expiration, you'd get $1.00, but that might take 3 more weeks. By closing now and selling a new 30-day call for $0.90, you collected $0.80 + $0.90 = $1.70 total over the same period. This compounding of premium is how active management improves returns.

Advanced Considerations: Rolling Covered Calls

Rolling is one of the most powerful management techniques for covered call sellers, but it requires understanding when and how to do it effectively.

What Rolling Means. Rolling a covered call means closing your existing short call by buying it back, then simultaneously selling a new call with either a later expiration date, a higher strike price, or both. The goal is to extend the position while collecting additional premium, avoiding assignment while maintaining income generation.

When to Roll. Consider rolling when your stock has rallied close to or above your strike price and you want to keep the shares. If your stock is at $53 and you sold the $52 call, you're at risk of assignment. Rather than letting the shares go, you can roll to the $55 call expiring next month, collecting a credit (additional premium) for the roll and keeping your shares.

Rolling Up and Out. The most common roll is "up and out"—rolling to a higher strike price and later expiration. This gives your stock more room to run while extending your time horizon. For example, rolling from a $50 call expiring this week to a $52 call expiring next month. You typically collect net premium for this roll because the later expiration has more time value.

Rolling for a Credit. The golden rule of rolling covered calls is to always collect a credit. This means the call you're selling brings in more money than the call you're buying back costs. If you can't roll for a credit, the position math doesn't favor rolling—you're better off accepting assignment or buying back the call without rolling to a new one.

When Rolling Doesn't Make Sense. If your stock has rallied far beyond your strike—say you sold the $50 call and the stock is now $60—rolling is usually a mistake. You'd have to buy back a deeply in-the-money call (expensive) and would get minimal credit for rolling to $65. At this point, accept that you achieved your profit target and let the shares be called away. Forced rolls to keep shares you've already committed to selling often leads to worse outcomes.

Calculating Roll Returns. When evaluating a roll, calculate the annualized return of the roll itself. If rolling costs you $0.50 to buy back the old call and you collect $0.80 for the new call, you net $0.30. Compare this to other opportunities. If the return is attractive, roll. If it's mediocre, assignment might be preferable.

Tools for Roll Analysis. Manually calculating every possible roll option (different strikes × different expirations) is tedious and time-consuming. You need to compare the credit, time added, and annualized return for each possibility. QuantWheel's Roll Assistant automates this, analyzing every possible roll and recommending the optimal one based on your preferences—whether you want maximum return, minimum time, or a specific strike price target. This turns a 30-minute calculation into a 30-second decision.

Covered Calls and the Wheel Strategy

Covered calls are the second leg of the popular wheel strategy, and understanding how they connect creates a more complete income-generating system.

How the Wheel Works. The wheel strategy combines cash-secured puts and covered calls in a cycle: (1) Sell cash-secured puts on a stock you'd like to own, collecting premium. (2) If assigned, you now own the stock at the strike price. (3) Immediately sell covered calls on those shares, collecting more premium. (4) If the covered call gets assigned, your shares are sold and you return to step one. The cycle "wheels" around, generating premium at every stage.

Why Covered Calls Complete the Wheel. The weakness of buying stock and holding it is that you generate no income during flat periods. Covered calls solve this by monetizing your stock position through premium collection. In the wheel strategy, even if you're assigned on a cash-secured put (forcing you to buy stock), you immediately begin generating income through covered calls, making the assignment part of the plan rather than a problem.

Cost Basis Tracking Through the Wheel. Here's where wheel traders often struggle: calculating accurate cost basis across multiple cycles. If you're assigned on a $50 cash-secured put after collecting $2 premium, your real cost basis is $48. If you then sell covered calls for $1.50 and get assigned at $52, your total gain is $52 - $48 + $1.50 = $5.50, not the simple $2 your broker might show. Tracking this manually through multiple wheel cycles becomes a spreadsheet nightmare. QuantWheel automatically tracks cost basis adjustments through every leg of the wheel, showing you your true breakeven and profit at all times.

Managing Wheel Positions. When running the wheel, your covered calls should generally be sold at strikes where you'd be happy starting a new cycle. If you're assigned at $50 and sell the $52 call, you're targeting a $4 total profit ($2 from the original put + $2 from stock appreciation). This becomes your new baseline for the next wheel cycle if assigned. Consistent strike selection relative to your cost basis is key to wheel profitability.

Combining Strategies for Consistent Income. Traders running the wheel on multiple stocks can generate weekly or monthly income streams as different positions expire at different times. The covered call stage is when you're already holding the bag (the shares), so the premium is pure income with no additional capital required. This capital efficiency makes covered calls particularly attractive within the wheel framework.

Tax Implications of Covered Calls

Covered calls create specific tax situations that affect your after-tax returns, especially if you're not aware of them.

Premium is Income Immediately. When you sell a covered call, the premium you collect is not taxed immediately as income. Instead, it remains in a sort of limbo until the position resolves. If the call expires worthless, the premium is taxed as a short-term capital gain. If you buy back the call, the difference between what you sold it for and what you bought it back for is taxed as a short-term capital gain or loss. Tax treatment depends on the outcome, not the initial collection.

Assignment Creates Stock Sale. When your covered call is assigned, you're selling your stock at the strike price. This triggers capital gains taxes on the stock sale. Your holding period for the stock determines whether it's a short-term or long-term gain. If you held the stock for more than one year, it's long-term (lower tax rate). Less than one year is short-term (ordinary income rate).

Covered Calls Can Reset Holding Period. Here's a tricky rule: if you sell an in-the-money covered call on stock you've held for less than one year, it can suspend or reset your holding period for long-term capital gains purposes. This means if you're approaching the one-year mark and you sell a deep in-the-money call, you might inadvertently prevent yourself from getting long-term gains treatment. Consult IRS Publication 550 or a tax advisor if you're in this situation.

Straddle Rules. If you sell and buy back the same covered call multiple times on the same stock within a short period, you could trigger wash sale rules or straddle rules that affect your ability to deduct losses. These are complex edge cases, but if you're actively trading covered calls (weekly expirations, constant rolling), be aware these rules exist.

Record Keeping Is Critical. Proper tax reporting requires tracking each covered call trade: when opened, what premium, when closed, at what price, and how it relates to the underlying stock position. Most brokers provide year-end tax documents (1099-B), but these don't always correctly account for complex option strategies across multiple cycles. Keeping your own records—or using a platform that tracks all of this automatically—prevents expensive tax mistakes.

Covered Calls in Different Market Conditions

The effectiveness of covered calls varies significantly depending on whether the market is rising, falling, or moving sideways.

Sideways Markets (Best for Covered Calls). When stocks trade in a range without significant upward or downward moves, covered calls shine. You collect premium month after month while the stock stays below your strike. Over time, these premium payments add up, significantly outperforming simple buy-and-hold during flat periods. Sideways markets are where the strategy generates consistent income with minimal assignment risk.

Slowly Rising Markets (Good for Covered Calls). When stocks trend gradually higher, covered calls work well with proper strike selection. By selling strikes slightly above the current price, you participate in the upside while collecting premium. You might get assigned occasionally, but you're selling at profit targets, which is a successful outcome. The key is not being too aggressive with strike selection—give your stocks room to rise.

Strongly Rising Markets (Challenging for Covered Calls). In bull markets where stocks are rallying aggressively, covered calls underperform simple stock ownership. You get assigned frequently, missing the big rallies beyond your strike prices. Premium collection doesn't compensate for the upside you surrender. During strong bull runs, many traders reduce or pause covered call selling, preferring to let their stocks run without caps.

Falling Markets (Poor for Covered Calls). When stocks are declining significantly, the premium you collect from covered calls provides minimal protection against losses. If your stock drops from $50 to $40, the $1 premium you collected barely offsets the $10 per share loss. Covered calls are not a hedging strategy—they generate income but don't protect capital in bear markets. In prolonged downtrends, the strategy becomes "selling your winners and holding your losers," which is the opposite of good trading.

Adjusting Strategy to Market Conditions. Experienced traders scale their covered call activity based on market regimes. In neutral to slightly bullish markets, they're aggressive with covered calls. In strongly bullish markets, they either stop selling them or sell much further out-of-the-money strikes to participate more in upside. In bearish markets, they reduce stock exposure entirely rather than trying to cover losses with small premiums.

Comparing Covered Calls to Alternatives

Covered calls aren't the only way to generate income from stocks you own. Understanding the alternatives helps you choose the right strategy for your situation.

Covered Calls vs. Buy-and-Hold. Pure stock ownership offers unlimited upside and simplicity but generates no income during flat periods and provides no downside protection. Covered calls trade unlimited upside for consistent income and slightly reduced cost basis. Buy-and-hold wins in strong bull markets; covered calls win in sideways to moderately bullish markets. Most long-term investors use a hybrid approach: hold core positions without options, sell covered calls on positions they'd be willing to trim.

Covered Calls vs. Cash-Secured Puts. Both strategies collect premium, but cash-secured puts are bullish bets that you'll acquire stock, while covered calls are positions you already hold. Cash-secured puts generate income while waiting to own stock; covered calls generate income from stock you already own. In the wheel strategy, these strategies connect: cash-secured puts get you into positions, covered calls generate income while you hold them.

Covered Calls vs. Collar Strategy. A collar involves selling a covered call and simultaneously buying a protective put. This caps both your upside and downside, creating a defined range of outcomes. Collars provide downside protection that covered calls don't but cost money (the put purchase reduces your net premium). Use collars when you want to hold stock through a specific period (earnings, market uncertainty) with limited risk. Use covered calls when you're comfortable with stock ownership and want income without paying for protection.

Covered Calls vs. Dividend Stocks. Both provide income, but in different forms. Dividends are typically 1-3% annually, paid quarterly, with no cap on upside. Covered calls can generate 6-24% annualized premium but cap your upside. Dividends are reliable and predictable; covered call income requires active management. Many traders combine both: own high-quality dividend stocks and sell covered calls on them, stacking both income sources.

Final Thoughts: Is Selling Covered Calls Right for You?

Covered calls suit specific types of traders in specific situations. Understanding whether you're one of them determines if this strategy belongs in your portfolio.

Covered calls work best if you: own stocks you'd be willing to sell at specific prices, prefer generating income over maximizing upside, have time to monitor positions and make management decisions, are comfortable with moderate complexity beyond simple buy-and-hold, and expect markets to trade sideways to moderately higher in the near term.

Covered calls are not ideal if you: believe your stocks will rally aggressively, are emotionally attached to positions and never want to sell, need simple strategies without management decisions, expect significant downward moves (where premium won't protect you), or prefer purely passive investing with no ongoing decisions.

Starting Your First Covered Call. If you decide covered calls fit your situation, start small with a single position on a stock you know well and are comfortable selling. Use a 30-45 day monthly expiration and a strike 3-5% above the current price. This conservative first trade helps you understand the mechanics and emotions involved. As you gain experience, you can expand to multiple positions, experiment with different strikes and expirations, and develop your own preferences.

The learning curve is moderate—not as simple as buy-and-hold, but far simpler than advanced option strategies. The math is straightforward, the risk is limited to stock ownership (which you already have), and the potential for consistent income generation makes covered calls one of the most practical option strategies for stock owners looking to improve their returns in non-trending markets.

Start your free trial of QuantWheel to automate covered call tracking, get alerts when positions hit 50% profit, and see real-time roll recommendations when your strikes are threatened. Focus on trading decisions, not spreadsheet management.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The trade examples, profit examples, and tax advice used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.