You're holding 100 shares of stock. You want to generate income by selling covered calls. But which strike price should you choose?

This is the question that determines whether you optimize your income, keep your shares, or accidentally cap your upside at exactly the wrong level. After managing hundreds of covered call positions, I've learned that strike selection is both simpler and more nuanced than most traders think.

Make trade selection easier with QuantWheel →

Quick Overview: Strike Selection Framework

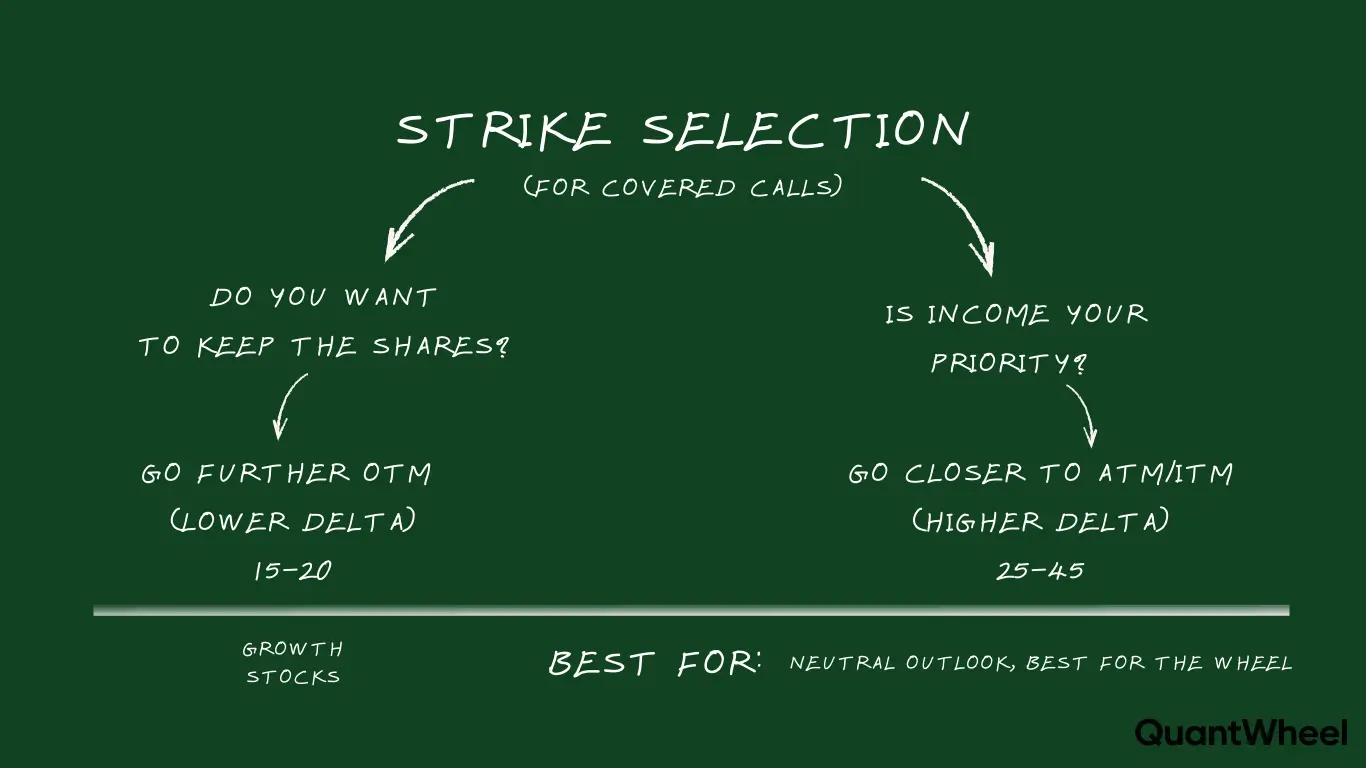

Before diving deep, here's what you need to know: strike selection is the balance between how much premium you collect and how likely you are to lose your shares. Higher strikes give you more upside potential but less premium. Lower strikes give you more premium but higher assignment probability.

TLDR: How to Select Covered Call Strike Price (Simple Answer)

For most wheel strategy traders, the 30-delta strike offers the optimal balance. This means selling a call that has approximately a 30% probability of finishing in-the-money at expiration.

Here's a simple example:

- You own 100 shares of AMD at $150 (your cost basis)

- AMD is currently trading at $155

- The $160 call (30 days out) has a 0.30 delta

- This call trades for $3.50, giving you $350 in premium

- You have a 70% probability of keeping your shares

- If assigned, you profit: $10 capital gain ($160-$150) + $3.50 premium = $13.50 per share ($1,350 total)

The decision tree:

- Want to keep your shares? → Sell 20-30 delta (out-of-the-money)

- Want maximum income? → Sell 50+ delta (at-the-money or in-the-money)

- Want to exit the position? → Sell in-the-money calls below current price

- Uncertain about direction? → Sell 30-40 delta as a balanced approach

Key rule: Never sell calls below your adjusted cost basis (including premium from any puts you sold) unless you want to realize a loss.

Understanding the Strike Selection Spectrum

The Three Strike Zones

Out-of-the-Money (OTM) Calls

- Strike price above current stock price

- Lower premium collected

- Lower assignment probability

- Keep shares and upside potential

- Best for: Long-term holdings you don't want to sell

At-the-Money (ATM) Calls

- Strike price near current stock price

- Moderate to high premium

- ~50% probability of assignment

- Balanced risk-reward profile

- Best for: Neutral market outlook, maximizing theta decay

In-the-Money (ITM) Calls

- Strike price below current stock price

- Highest premium collected

- High probability of assignment

- Essentially committing to sell

- Best for: Exiting positions, bearish outlook

The Premium vs. Protection Trade-off

Every strike selection involves this fundamental trade-off:

More Premium = Less Protection

- Closer strikes collect more premium

- But you have less room for stock appreciation

- Higher chance of giving up your shares

Less Premium = More Protection

- Further strikes collect less premium

- But you keep more upside potential

- Lower chance of assignment

There's no "right" answer – only the right answer for YOUR goals.

The Delta-Based Approach (Most Practical)

Delta is your best friend for strike selection. It tells you two critical things:

- How much the option price moves when the stock moves $1

- The approximate probability of finishing in-the-money

Delta Guidelines for Covered Calls

Note: Yield ranges represent historical observations and may vary significantly based on market volatility, individual execution, and stock selection. Past results do not guarantee future outcomes.

0.20 Delta (Conservative)

- ~20% probability of assignment

- Strikes typically 5-10% out-of-the-money

- Lower premium (~0.5-1.5% of stock price)

- Best for: Stocks you definitely want to keep

- Annual yield: 6-8% in historical examples

0.30 Delta (Balanced) ⭐ RECOMMENDED

- ~30% probability of assignment

- Strikes typically 2-5% out-of-the-money

- Moderate premium (~1-2% of stock price)

- Best for: Wheel strategy, balanced income generation

- Annual yield: 10-15% in historical examples

0.40 Delta (Aggressive)

- ~40% probability of assignment

- Strikes near current price

- Good premium (~2-3% of stock price)

- Best for: Neutral to slightly bearish outlook

- Annual yield: 15-20% in historical examples

0.50+ Delta (Maximum Income)

- 50%+ probability of assignment

- At-the-money or in-the-money strikes

- Highest premium (~3-5%+ of stock price)

- Best for: Positions you're ready to exit

- Annual yield: 20-30%+ in historical examples

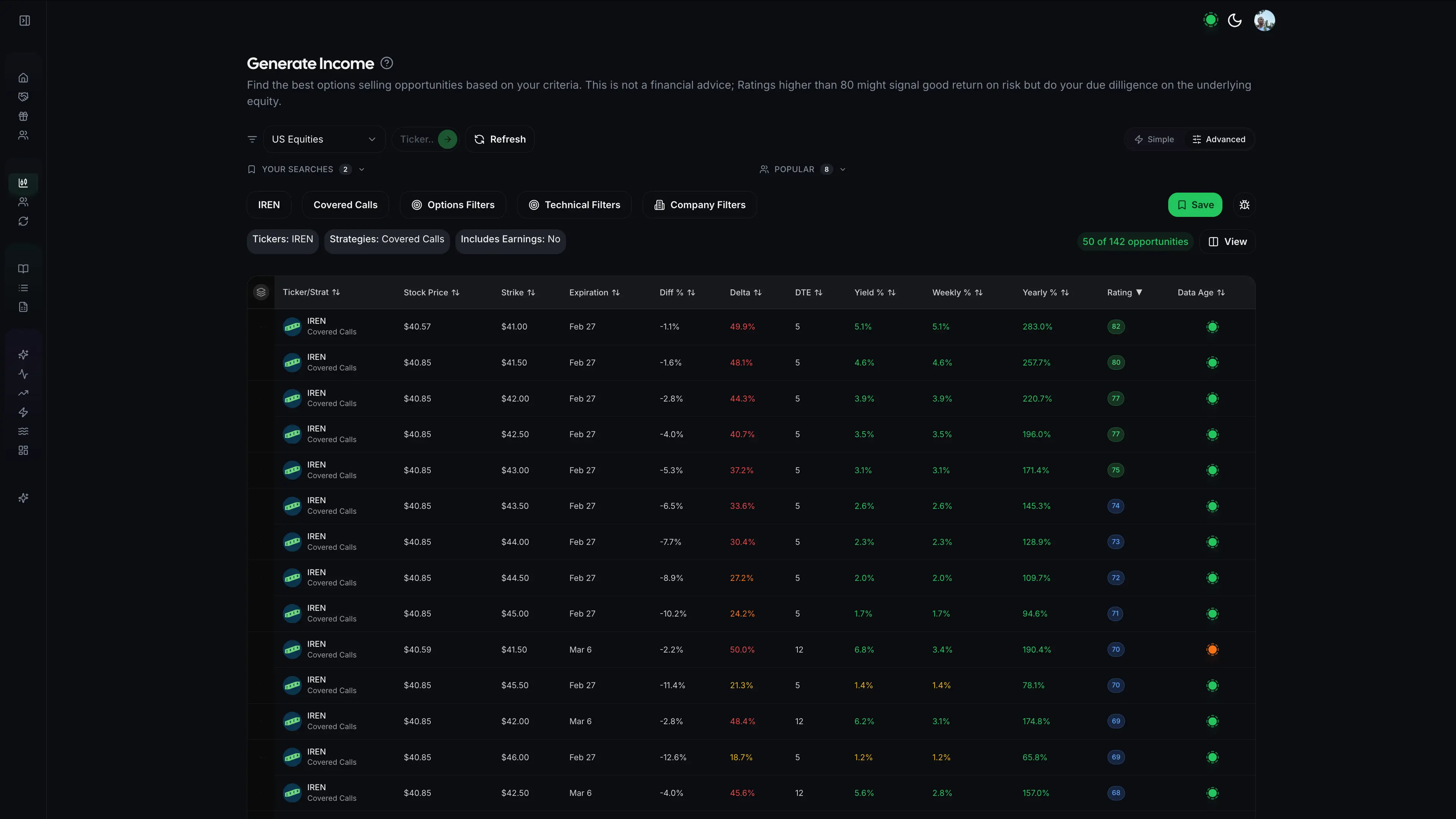

Real Example: AMD and IREN Strike Selection

Let's say AMD is trading at $155:

| Strike | Delta | Premium | Assignment Prob | Your Decision |

|---|---|---|---|---|

| $150 (ITM) | 0.65 | $8.50 | 65% | Want to exit position |

| $155 (ATM) | 0.50 | $5.00 | 50% | Maximum premium, neutral |

| $160 (OTM) | 0.30 | $3.00 | 30% | Balanced approach ⭐ |

| $165 (OTM) | 0.15 | $1.50 | 15% | Keep shares, lower premium |

| $170 (OTM) | 0.08 | $0.75 | 8% | Very conservative |

Most wheel strategy traders would choose the $160 strike (0.30 delta) for the optimal balance.

Make trade selection easier with QuantWheel →

Cost Basis Considerations (Critical)

Your cost basis determines which strikes are actually profitable for you.

Calculating Your Adjusted Cost Basis

If you bought the stock outright:

- Cost basis = Purchase price

If you got assigned from a cash-secured put (wheel strategy):

- Cost basis = Strike price - Premium collected on put

- Example: Assigned at $50 strike, collected $2 put premium → Real cost basis = $48

Here's where most traders make a mistake: your broker shows $50, but your real cost is $48. This is exactly why tracking becomes critical when running the wheel strategy.

This is where platforms like QuantWheel automatically adjust your cost basis when assignments happen – no manual tracking needed. Your real breakeven is calculated for you, so you know which strikes are profitable.

The Golden Rule of Strike Selection

Never sell calls below your adjusted cost basis unless you want to realize a loss.

Bad example:

- Adjusted cost basis: $48 (after $2 put premium)

- You sell $45 strike calls

- If assigned, you sell at $45 – below your $48 cost

- You've locked in a $3 loss per share

Good example:

- Adjusted cost basis: $48

- You sell $52 strike calls for $2 premium

- If assigned, you sell at $52

- Your profit: $4 capital gain + $2 call premium = $6 per share

Income Goals vs. Assignment Risk

If Your Primary Goal Is Income

Maximize premium collection:

- Target 40-50 delta strikes

- Consider weekly options for more frequent premium

- Accept higher assignment probability

- Run this on stocks you're comfortable selling

Income-focused strike selection:

- Sell at-the-money or slightly in-the-money

- Choose shorter expirations (7-14 DTE)

- Roll positions when they hit 50% profit

- Reinvest premium immediately

If Your Primary Goal Is Stock Appreciation

Minimize assignment risk:

- Target 15-20 delta strikes

- Use monthly options (more premium for same delta)

- Accept lower immediate income

- Run this on stocks with growth potential

Growth-focused strike selection:

- Sell out-of-the-money calls (2-5% above current price)

- Choose longer expirations (30-45 DTE)

- Only sell calls when stock is extended

- Be prepared to buy back calls if stock momentum shifts

Time to Expiration and Strike Selection

Weekly Options (7-10 DTE)

Advantages:

- Faster theta decay

- More frequent premium collection

- Greater annual yield potential

Strike considerations:

- Need closer strikes for meaningful premium

- Higher management intensity

- Better for stable, low-volatility stocks

Best strikes: 30-40 delta

Monthly Options (30-45 DTE)

Advantages:

- Better premium for out-of-the-money strikes

- Less management required

- Smoother income stream

Strike considerations:

- Can sell further out for same premium

- Better for volatile stocks

- More time for stock to move against you

Best strikes: 20-30 delta

The 21-Day Sweet Spot

Many experienced traders target 21-30 DTE as the optimal balance:

- Theta decay accelerates after 30 DTE

- Still enough time premium for good strikes

- Allows 50% profit targets with time to spare

Managing Different Market Conditions

Bullish Market (Stock Rising)

Strike selection strategy:

- Use higher delta (closer strikes) early in move

- Switch to lower delta (further strikes) as stock extends

- Consider selling fewer contracts to keep some upside

- Be prepared to roll up and out if stock surges

Specific approach: Start: 40-50 delta → As stock rises: 20-30 delta

Neutral Market (Sideways Movement)

Strike selection strategy:

- This is ideal for covered calls

- Use 30-40 delta strikes consistently

- Maximize premium collection

- The wheel strategy thrives here

Specific approach: Consistent 30 delta, monthly options, close at 50% profit

Bearish Market (Stock Declining)

Strike selection strategy:

- Lower strikes collect premium but guarantee assignment

- Higher strikes collect minimal premium

- Consider if you want to hold through decline

- May be time to close position entirely

Specific approach: If holding: 20 delta defensive calls If exiting: In-the-money calls to maximize exit value

The Rolling Decision and Strike Selection

When your covered call goes in-the-money and you don't want assignment, you can "roll" to a new strike.

When to Roll

Roll when:

- Stock rises above your strike

- You don't want to sell your shares

- You can collect additional credit

- Time to expiration is 21 days or less

Strike Selection When Rolling

Roll up and out:

- Close current call (buy back)

- Sell new call at higher strike, later expiration

- Collect net credit if possible

Example rolling scenario:

- Original: $155 call, 14 DTE, stock now at $160

- Roll to: $165 call, 45 DTE

- Collect additional $2 credit

- Buy yourself more time and higher strike

Platforms like QuantWheel's Roll Assistant compare all possible roll options and calculate which generates the best return – eliminating the manual math and decision paralysis.

Strike Selection for Different Stock Types

High Volatility Stocks (Meme Stocks, Growth Tech)

Characteristics:

- Large daily swings

- High implied volatility

- Significant premium available

Strike approach:

- Use wider strikes (further OTM)

- Shorter expirations to capitalize on volatility

- 20-25 delta to avoid getting blown through

- Be prepared for large adverse moves

Example stocks: NVDA, TSLA, GME, AMD

Low Volatility Stocks (Blue Chips, Utilities)

Characteristics:

- Steady, predictable movement

- Lower implied volatility

- Limited premium

Strike approach:

- Closer strikes needed for meaningful premium

- 35-45 delta acceptable

- Monthly options for better time premium

- More consistent, boring income

Example stocks: KO, JNJ, PG, VZ

Dividend Stocks

Special consideration: Dividend capture

Strike approach:

- Don't sell calls before ex-dividend date (you want the dividend)

- Sell calls after ex-dividend (stock typically drops)

- Factor dividend into effective yield calculation

- Consider strikes above ex-div adjusted price

Common Strike Selection Mistakes

Mistake #1: Chasing Premium

The trap: Selling calls too close to current price for maximum premium

Why it's bad:

- High assignment probability

- Missing upside moves

- Constantly buying back for losses

- Reduced total returns

The fix: Accept less premium for better position management

Mistake #2: Ignoring Cost Basis

The trap: Selling strikes below your real cost basis

Why it's bad:

- Locking in guaranteed losses

- Defeating the purpose of the strategy

- Poor tax consequences

The fix: Always calculate adjusted cost basis first (especially after assignments)

Mistake #3: Using Same Strike Every Time

The trap: "I always sell 30 delta" regardless of conditions

Why it's bad:

- Market conditions change

- Stock conditions change

- Volatility fluctuates

The fix: Adjust delta targets based on:

- Current IV level (high IV → further strikes)

- Stock momentum (strong momentum → further strikes)

- Your conviction (less conviction → closer strikes)

Mistake #4: Forgetting Upcoming Events

The trap: Selling calls before earnings or major events

Why it's bad:

- Massive volatility after events

- Can blow through your strike

- Event-driven assignment

The fix: Check earnings calendars before selling calls (or sell after events with inflated IV)

Mistake #5: Emotional Strike Selection

The trap: "I really don't want to sell this stock, so I'll sell the $200 strike" (when stock is at $150)

Why it's bad:

- Collecting pennies

- Not worth the capital commitment

- Poor risk-adjusted returns

The fix: If you don't want to sell, either:

- Don't sell calls

- Accept reasonable assignment risk

- Run covered calls only on positions you're okay selling

Advanced Considerations

Strike Selection and Tax Efficiency

Short-term vs long-term:

- Covered calls reset the holding period if "in-the-money"

- Selling ITM calls can convert would-be long-term gains to short-term

- Consider tax implications before strike selection

Qualified covered calls:

- Strikes can't be "too deep" in-the-money

- Must be >85% of stock price (varies by time)

- Check IRS rules if tax optimization matters

Strike Spacing and Liquidity

Liquid options:

- Strike spacing: typically $1-$5 increments

- Choose strikes with volume and open interest

- Tighter bid-ask spreads

Illiquid options:

- Wide strike spacing

- Use mid-price orders

- May need to accept wider strikes than ideal delta

Institutional Strike Selection (Large Positions)

Special considerations:

- Can't always sell at desired delta

- Must consider open interest capacity

- May need to ladder strikes

- Slippage on large orders

Strike Selection Tools and Automation

Manual Strike Selection Process

Step-by-step:

- Determine your cost basis

- Identify minimum acceptable strike

- Check delta for nearby strikes

- Calculate premium yield

- Assess assignment probability

- Make decision

Time required: 5-10 minutes per position

Automated Strike Selection

After tracking 15+ covered call positions manually, the spreadsheet becomes overwhelming. Which calls are profitable to close? What's the optimal roll? Which strikes maximize return?

This is exactly why platforms built for options sellers exist. QuantWheel's Roll Assistant analyzes all possible strikes across all expirations, calculates expected return for each, and recommends the optimal selection – cutting decision time from 10 minutes to 10 seconds.

For wheel strategy traders managing multiple positions, this automation means focusing on strategy rather than spreadsheet maintenance.

Your Strike Selection Checklist

Before selling any covered call, verify:

- Cost basis calculated (including any put premium)

- Minimum strike determined (above cost basis for profit)

- Target delta selected (20-40 based on goals)

- Premium checked (worthwhile for the risk)

- Expiration chosen (weekly vs monthly)

- Earnings date verified (no surprises upcoming)

- Assignment comfort confirmed (okay selling at this strike?)

- Liquidity assessed (volume and open interest adequate)

Conclusion: Your Strike Selection Strategy

Strike selection isn't about finding the "perfect" strike – it's about aligning your strike with your goals.

For most wheel strategy traders:

- Start with 30-delta strikes

- Use 30-45 DTE expirations

- Always stay above your adjusted cost basis

- Close or roll at 50% profit with 21+ DTE remaining

- Accept assignment as part of the plan

Remember: Conservative strike selection may generate less premium per trade, but keeping your shares and collecting premium repeatedly often outperforms aggressive strikes that result in constant assignments.

Track your results. Adjust based on what works for YOUR portfolio and risk tolerance. Strike selection is both a science (delta, probability) and an art (market conditions, conviction).

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.