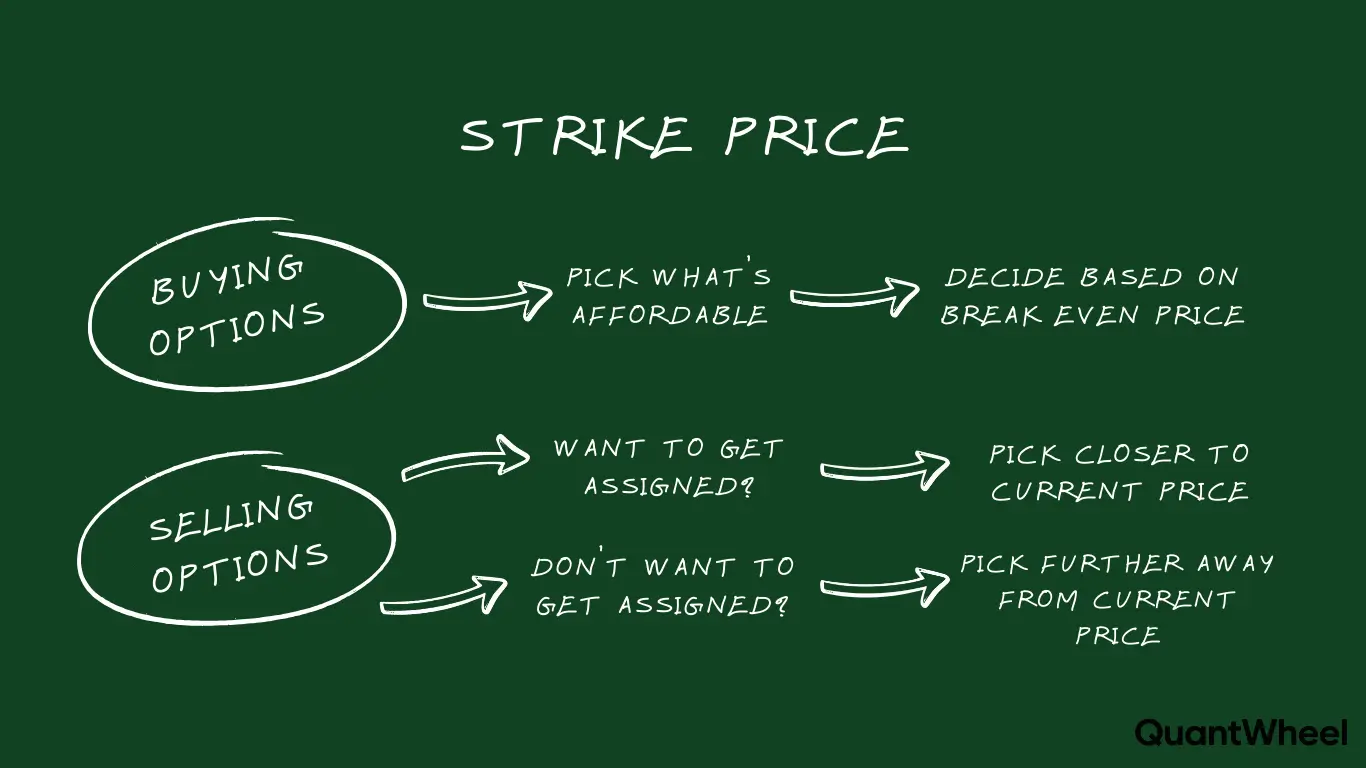

Choosing the right strike price can make or break your wheel strategy results. Too aggressive and you'll get assigned on every trade with stocks falling against you. Too conservative and you'll barely collect enough premium to justify the capital requirement.

After managing hundreds of wheel positions, I've learned that strike selection is less about complicated formulas and more about matching strikes to your actual goals. Here's exactly how to choose strikes that work for your specific situation.

TLDR: How to Choose Strike Price for Wheel Strategy

The right strike price depends on whether you're selling puts or calls, and what you want to happen:

For Cash-Secured Puts (Starting the Wheel):

- Target the 30-delta level for the best balance of premium and safety

- At 30-delta, you have approximately 70% chance of keeping the premium and 30% chance of assignment

- This typically places your strike 5-10% below the current stock price, depending on volatility

Example: Stock XYZ trades at $100. The 30-delta put is at the $95 strike, paying $2.50 premium.

- You collect $250 per contract upfront

- If the stock stays above $95, you keep the $250

- If the stock drops below $95, you buy 100 shares at $95 (but your real cost is $92.50 after the premium)

- Your breakeven is $92.50, giving you 7.5% downside cushion

For Covered Calls (After Assignment):

- If you want to sell the stock: Choose strikes at or slightly above your cost basis (30-40 delta)

- If you want to keep the stock: Choose strikes far above current price (15-20 delta)

- Never sell calls below your adjusted cost basis unless you're willing to take a loss

The Quick Decision Framework:

- More premium = Higher strike (closer to current price) = More assignment risk

- More safety = Lower strike (further from current price) = Less premium

- Your sweet spot is typically 30-delta, which balances both goals

Why this matters: Your broker won't show you the adjusted cost basis after assignment. Most traders use spreadsheets to track this, but it breaks down after 5-10 positions. Tools like QuantWheel automatically calculate your real cost basis when you get assigned, so you always know where to set your covered call strikes without risking losses.

Discover for yourself inside QuantWheel →

Understanding Strike Price Basics for the Wheel

Before diving into specific selection strategies, let's clarify what we're actually choosing.

What Is Strike Price?

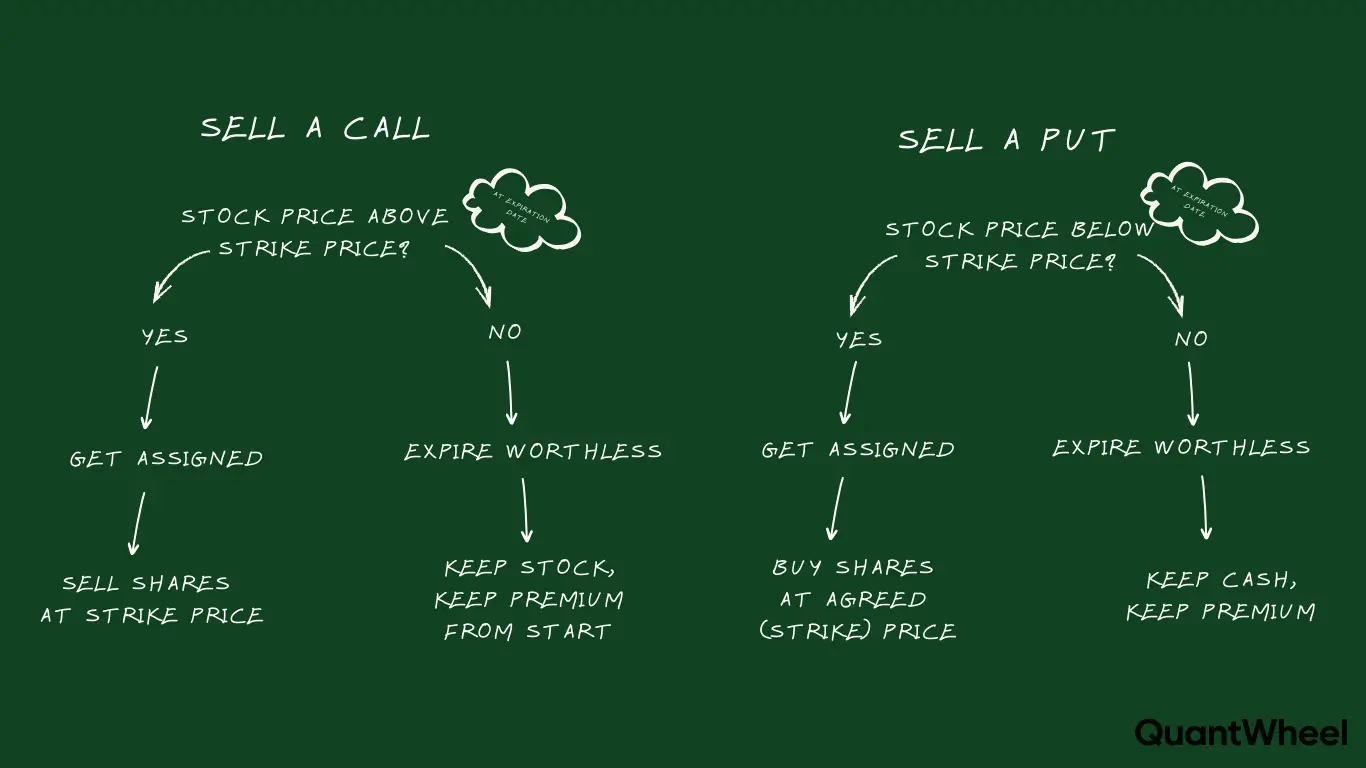

The strike price (also called the exercise price) is the predetermined price at which you agree to buy or sell stock when selling options.

For cash-secured puts: The strike is the price you'll pay to buy 100 shares if assigned.

For covered calls: The strike is the price you'll receive for selling your 100 shares if assigned.

Strike Price vs. Current Stock Price

Options are classified based on their strike relative to the current stock price:

Out-of-the-Money (OTM):

- Puts: Strike below current price (Example: $95 put when stock is $100)

- Calls: Strike above current price (Example: $105 call when stock is $100)

- Lower premium, lower probability of assignment

At-the-Money (ATM):

- Strike at or very near current price (Example: $100 strike when stock is $100)

- Highest premium, roughly 50% probability of assignment

- Approximately 50-delta

In-the-Money (ITM):

- Puts: Strike above current price (Example: $105 put when stock is $100)

- Calls: Strike below current price (Example: $95 call when stock is $100)

- Higher premium but already "in the hole" on assignment

For wheel strategy, you typically sell out-of-the-money options to collect premium while minimizing immediate assignment.

The Delta Approach to Strike Selection

Delta is the most practical tool for choosing strikes because it tells you both the probability of assignment and how much the option price will move with the stock.

What Is Delta?

Delta represents two things:

- Directional exposure: How much the option price changes per $1 move in the stock

- Approximate probability: The rough percentage chance the option expires in-the-money

Examples:

- A 30-delta put means approximately 30% chance of assignment (stock finishing below strike)

- A 20-delta call means approximately 20% chance of assignment (stock finishing above strike)

- A 50-delta option (at-the-money) has roughly 50/50 odds

Why Delta Beats "Percentage Below Current Price"

Many traders say "I sell puts 5% below the current price" or "I target strikes 10% out-of-the-money."

This approach has a fatal flaw: it ignores volatility.

A strike 5% below current price might be:

- 15-delta on a stable utility stock (low risk)

- 40-delta on a volatile meme stock (high risk)

Delta automatically adjusts for volatility, giving you consistent risk across different stocks.

The 30-Delta Sweet Spot for Wheel Strategy

Through backtesting and real trading, the 30-delta level emerges as the optimal balance for most wheel traders:

What 30-delta means:

- Approximately 70% probability of profit (keeping premium)

- Approximately 30% probability of assignment

- Typically 5-10% out-of-the-money, depending on volatility

Why 30-delta works:

- Collects meaningful premium (usually 1-3% of strike per 30-45 days)

- Provides downside cushion before assignment

- Aligns with "high probability" trading (70% win rate)

- Not so far out that premium becomes negligible

Example comparison on $100 stock with 30 days to expiration:

| Delta | Strike | Premium | Assignment Probability | Return if Kept |

|---|---|---|---|---|

| 15-delta | $93 | $0.75 | 15% | 0.75% |

| 30-delta | $95 | $1.50 | 30% | 1.50% |

| 40-delta | $97 | $2.25 | 40% | 2.25% |

| 50-delta | $100 | $3.00 | 50% | 3.00% |

The 30-delta level gives you 1.50% return in 30 days (roughly 18% annualized) with only 30% assignment risk.

Strike Selection for Cash-Secured Puts

When you're starting the wheel or adding new positions, you're selling cash-secured puts. Here's how to choose the right strike.

Standard Approach: Target 30-Delta

The process:

- Open your broker's option chain for your target stock

- Look at the put side for your desired expiration (typically 30-45 days out)

- Find the strike closest to 30-delta

- Check the premium—does it meet your return goals? (Usually 1-3% of strike price)

- If yes, that's your strike. If no, consider a different stock.

Example: Selling puts on stock trading at $52:

- 25-delta put: $50 strike, $0.80 premium (1.6% return)

- 30-delta put: $50 strike, $1.00 premium (2.0% return)

- 35-delta put: $51 strike, $1.30 premium (2.5% return)

The 30-delta level at $50 strike pays $1.00, giving you 2% return if you keep the premium, or buying stock at an effective $49 cost basis if assigned.

Adjusting for Risk Tolerance

Conservative (20-delta):

- Lower assignment probability (20% vs 30%)

- More downside cushion (typically 7-15% below current price)

- Lower premium (0.5-1.5% per month)

- Best for volatile stocks or bear markets

Standard (30-delta):

- Balanced risk/reward

- Moderate cushion (5-10% below current price)

- Good premium (1-3% per month)

- Best for most situations

Aggressive (40-delta):

- Higher assignment probability (40%)

- Less cushion (3-7% below current price)

- Higher premium (2-4% per month)

- Only for stocks you genuinely want to own

When Stock Ownership Is Your Goal

If your primary goal is owning the stock at a specific price, ignore delta and choose your desired purchase price.

Example: You want to own AMD at $120, and it's currently trading at $130.

Instead of targeting 30-delta (which might be $125 strike), sell the $120 put even if it's only 15-delta.

You're essentially:

- Getting paid to place a limit buy order

- Collecting premium while waiting for your price

- Accepting lower premium for your specific entry point

This approach works when you have genuine conviction about the stock at that valuation, not just chasing premium.

Red Flags When Selecting Put Strikes

Premium seems too good:

- If you're getting 5%+ premium on a 30-delta put, something's wrong

- Usually signals upcoming earnings, news, or major volatility

- Check earnings date, news, and why IV is elevated

Strike is too close to current price:

- Don't get tempted by high premium at 50-delta (at-the-money)

- 50% assignment probability is coin-flip territory

- You're no longer in "high probability" trading territory

Strike is below your genuine willingness to own:

- Never sell puts at strikes where you'd be unhappy owning the stock

- Premium isn't worth getting stuck in a position you don't want

- Be honest about your real conviction level

Strike Selection for Covered Calls

After you get assigned on your puts, you now own 100 shares and need to sell covered calls. Strike selection changes because your goal might be different.

Two Scenarios: Keep vs. Sell

Scenario 1: You want to keep the stock

- You got assigned below your target entry, stock is down

- You believe in long-term appreciation

- You want to collect premium while waiting for recovery

→ Choose strikes further out-of-the-money (15-20 delta)

Scenario 2: You're ready to sell the stock

- You got assigned near fair value

- You're fine taking profits

- You want to complete the wheel cycle and free up capital

→ Choose strikes at or slightly above cost basis (30-40 delta)

The Critical Rule: Never Sell Below Adjusted Cost Basis

Here's where most traders mess up covered call strikes: they forget about their adjusted cost basis.

Example of the problem:

You sold a $50 put, collected $2 premium, and got assigned.

- Your broker shows cost basis: $50 per share

- Your REAL cost basis: $48 per share (after premium)

If you sell a covered call at the $49 strike (because it pays good premium), you're locking in a $1 per share LOSS if assigned.

The right approach:

Your adjusted cost basis is $48, so never sell calls below $48 unless you accept the loss.

This is where position tracking becomes critical. Most traders use spreadsheets to track adjusted cost basis, but it breaks down after 5-10 positions. Platforms like QuantWheel automatically calculate your real cost basis when you get assigned, so you always know your true breakeven.

Standard Covered Call Strike Selection

If keeping the stock:

- Target 15-20 delta (far out-of-the-money)

- Strike typically 5-15% above current price

- Lower premium (0.5-1.5% per month) but low probability of losing shares

- Roll up and out if stock rallies toward your strike

If ready to sell:

- Target 30-40 delta (slightly out-of-the-money or at-the-money)

- Strike at or above your adjusted cost basis

- Higher premium (1-3% per month) and reasonable chance of assignment

- Accept assignment and start new wheel cycle

Handling In-the-Money Situations

Sometimes you get assigned on puts and the stock immediately rallies above your strike. Now your shares are "in-the-money" for calls.

Example:

- Bought shares via assignment at $50

- Collected $2 put premium (real cost: $48)

- Stock now trading at $54

Your options:

- Sell ATM or slight OTM calls ($54-55 strike, 40-50 delta)

- High premium ($3-4)

- Likely assignment

- Lock in profit and complete cycle

- Sell further OTM calls ($57-58 strike, 20-30 delta)

- Moderate premium ($1-2)

- Keep shares if you believe in more upside

- Balance premium with keeping gains

- Sell deep OTM calls ($60+ strike, 10-15 delta)

- Low premium ($0.50-1)

- Keep shares and long-term gains

- Minimal income but preserve upside

Most wheel traders choose option 1 or 2—lock in profit or balance upside with income.

Advanced Strike Selection Strategies

Once you're comfortable with the 30-delta standard approach, here are advanced techniques.

Volatility-Adjusted Strike Selection

The 30-delta guideline automatically adjusts for volatility, but you can fine-tune based on implied volatility (IV) rank.

High IV environment (IV rank 70-100):

- Option premiums are inflated

- You can sell further OTM strikes (20-25 delta) and still get attractive premium

- More downside protection with similar returns

Low IV environment (IV rank 0-30):

- Option premiums are deflated

- You might need to move closer to ATM (35-40 delta) for decent premium

- Less downside protection, more assignment risk

Example on $100 stock:

| IV Rank | Premium at 30-delta | Premium at 25-delta | Strategy |

|---|---|---|---|

| 80 (High) | $3.00 | $2.20 | Choose 25-delta for safety |

| 20 (Low) | $1.20 | $0.70 | Stick with 30-delta for income |

In high IV, you get paid to take less risk. In low IV, you need more risk for acceptable returns.

Strike Laddering for Multiple Contracts

If you're selling multiple contracts on the same stock, consider spreading strikes across different deltas.

Example with 3 contracts on $100 stock:

- 1 contract at 25-delta ($94 strike) – conservative

- 1 contract at 30-delta ($96 strike) – standard

- 1 contract at 35-delta ($98 strike) – aggressive

Benefits:

- Diversified assignment risk

- Higher blended premium than all-conservative

- Lower average risk than all-aggressive

Tracking complexity: Different strikes mean different cost bases if assigned, which becomes difficult to track manually. This is another area where automated tracking tools help manage multi-position portfolios.

Earnings-Adjusted Strike Selection

If you're trading through earnings (generally not recommended for beginners), adjust your strikes for the volatility expansion.

Standard approach during earnings:

- Avoid entirely—close positions before earnings

- If you must trade, go much further OTM (15-20 delta)

- Premium will be higher due to elevated IV

- Risk is asymmetric (stocks gap beyond your strikes)

After earnings:

- IV crush provides opportunity

- Sell closer strikes (35-40 delta) for good premium with normalized risk

- Within 1-2 days of earnings announcement for best timing

Practical Strike Selection Examples

Let's walk through real scenarios with specific numbers.

Example 1: Starting a New Wheel Position on SOFI

Setup:

- Stock price: $8.50

- Your goal: Collect premium, willing to own at reasonable price

- Account size: Can handle assignment

Option chain for 30 days out:

| Strike | Delta | Premium | If Assigned | If Kept |

|---|---|---|---|---|

| $7.50 | 20 | $0.15 | Cost basis $7.35 | 2.0% return |

| $8.00 | 30 | $0.25 | Cost basis $7.75 | 3.1% return |

| $8.50 | 45 | $0.40 | Cost basis $8.10 | 4.7% return |

Decision: Choose the $8.00 strike (30-delta)

- Pays $25 per contract

- 30% chance of assignment

- If assigned, you own stock at effective $7.75 (9% below current)

- If expires worthless, you keep $25 (3.1% monthly return)

Example 2: Covered Call After Assignment on AMD

Setup:

- You got assigned at $120 strike

- You collected $3.00 put premium originally

- Real cost basis: $117 per share

- Stock now trading at $122

- You're ready to complete the wheel and take profit

Option chain for 30 days out:

| Strike | Delta | Premium | Profit if Assigned | If Expires |

|---|---|---|---|---|

| $120 | 40 | $3.50 | $3 + $3.50 = $6.50 (5.6%) | Keep shares, keep $3.50 |

| $125 | 25 | $2.00 | $8 + $2 = $10 (8.5%) | Keep shares, keep $2.00 |

| $130 | 15 | $1.00 | $13 + $1 = $14 (12.0%) | Keep shares, keep $1.00 |

Decision: Choose the $120 strike (40-delta)

- Never sell below your $117 cost basis

- $120 strike gives good premium ($3.50)

- If assigned, total profit is $6.50 per share (5.6%)

- If stock pulls back, you keep $3.50 and can sell again

Example 3: Conservative Approach in Bear Market

Setup:

- Market correction underway

- High volatility (VIX above 30)

- You want exposure but need safety

- Looking at AAPL trading at $180

Option chain for 45 days out:

| Strike | Delta | Premium | Distance from Price | If Assigned |

|---|---|---|---|---|

| $165 | 20 | $2.50 | 8.3% below | Cost basis $162.50 (9.7% below) |

| $170 | 25 | $3.50 | 5.6% below | Cost basis $166.50 (7.5% below) |

| $175 | 30 | $5.00 | 2.8% below | Cost basis $170.00 (5.6% below) |

Decision: Choose the $165 strike (20-delta)

- Extra safety in volatile market

- Still collecting $2.50 ($250 per contract)

- If assigned, cost basis is 9.7% below current price

- Worth the premium trade-off for safety

Common Strike Selection Mistakes

Mistake 1: Chasing Premium

The trap: You see a strike paying 5% premium and it looks amazing compared to your usual 2%.

Why it's wrong: High premium signals high risk—the market sees elevated probability of assignment or the stock moving against you.

The fix: Stick to your delta target (usually 30). If premium is unusually high, investigate why (earnings, news, elevated IV).

Mistake 2: Using "Percentage Below Price" Without Delta

The trap: You always sell puts "10% below current price" without checking delta.

Why it's wrong: 10% below on a stable stock might be 15-delta (too conservative), while 10% below on a volatile stock might be 45-delta (too aggressive).

The fix: Use delta as your primary metric, which automatically adjusts for volatility.

Mistake 3: Forgetting Adjusted Cost Basis on Calls

The trap: Your broker shows $50 cost basis, so you sell the $52 call thinking you'll make $2 per share profit.

Why it's wrong: You forget you collected $3 put premium when you got assigned. Your real cost is $47, and the $52 call will give you $5 profit, not $2.

The fix: Track your adjusted cost basis including all premium collected. Most traders use spreadsheets, but they break down after 5-10 positions. Tools like QuantWheel automatically track this for you.

Mistake 4: Selling Strikes You Don't Actually Want

The trap: You sell a $45 put on a $50 stock for great premium, but you'd actually hate owning it below $48.

Why it's wrong: Premium isn't worth getting stuck in positions you don't want.

The fix: Be honest about your real conviction level. Only sell strikes at prices where you'd genuinely be happy owning the stock.

Mistake 5: Ignoring Earnings Date

The trap: You sell options expiring in 30 days without checking if earnings falls within that window.

Why it's wrong: Earnings can cause gaps beyond your strike, turning a "safe" 30-delta position into certain assignment with losses.

The fix: Always check the earnings date before opening positions. Most traders close or roll positions before earnings to avoid binary events.

Tools and Resources for Strike Selection

Finding Delta in Your Broker Platform

Every major broker shows delta in the option chain:

ThinkorSwim (TD Ameritrade):

- Open option chain

- Delta column shows values (will display as -0.30 for puts, 0.30 for calls)

- Use the "Probability of ITM" column as well

Tastyworks:

- Option chain shows delta prominently

- Also shows probability of profit

- Color-coded for quick reference

E*Trade, Fidelity, Schwab:

- Option chain has delta column (sometimes labeled "Δ")

- May need to enable it in column settings

Strike Selection With QuantWheel

For traders managing multiple wheel positions, QuantWheel's screener automatically shows optimal strikes based on your delta preferences.

How it works:

- Set your target delta (default 30-delta)

- Screener filters the entire market for opportunities

- Shows premium, IV rank, and risk metrics

- Automatically suggests strikes meeting your criteria

Why this matters: Instead of manually checking option chains on 50+ stocks, you see the best opportunities across the whole market in minutes.

When you get assigned, QuantWheel automatically adjusts your cost basis so your covered call strikes are always above your real breakeven—no manual tracking needed.

Putting It All Together: Your Strike Selection Checklist

Before selling any option in the wheel strategy, use this checklist:

For Cash-Secured Puts:

- Target strike is at 30-delta (or your preferred risk level)

- Premium meets your return goal (typically 1-3% of strike per month)

- Strike price is a level where you'd genuinely be happy owning the stock

- No earnings announcement between now and expiration

- IV rank is reasonable (not unusually high without understanding why)

- You have sufficient cash to handle assignment

For Covered Calls:

- Strike is at or above your adjusted cost basis (including put premium collected)

- Delta matches your goal (30-40 if ready to sell, 15-20 if keeping shares)

- Premium is worth the risk of losing shares

- No earnings announcement between now and expiration

- You're prepared for either outcome (keeping shares or assignment)

General:

- DTE (days to expiration) is 30-45 days for optimal theta decay

- You understand the max profit, max loss, and breakeven

- Position size is appropriate (not over-allocated to single stock)

Final Thoughts on Strike Selection

Choosing the right strike price isn't about finding the perfect formula—it's about matching strikes to your actual goals and risk tolerance.

The 30-delta guideline works for most wheel traders most of the time because it balances premium income with assignment probability. But your specific situation might call for 20-delta (more conservative) or 40-delta (more aggressive).

What matters most is consistency. Choose a delta target that aligns with your goals, stick to it across different stocks and market conditions, and let the law of large numbers work in your favor.

The traders who succeed with the wheel strategy aren't the ones chasing the highest premium or trying to optimize every strike to perfection. They're the ones who:

- Set clear criteria (usually 30-delta)

- Apply those criteria consistently

- Track their positions accurately (including cost basis adjustments)

- Avoid emotional decisions

And when you're managing 10, 15, or 20+ wheel positions simultaneously, having a system for tracking those strikes and cost bases becomes essential. That's where the spreadsheets break down and professional tools make the difference.

Risk Disclosure

Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.