If you sell options for income, everything works beautifully — until it doesn’t.

This guide covers everything you need to know about black swan protection for options portfolios.

Author: David Romic – retail options trader and active member in the options trading communities on Reddit (u/thedavidromic).

I share wheel strategy setups, trade management, and lessons learned from real positions.

Scroll down to find advices on how to navigate the black swan event and save time reading.

TL;DR — Black Swan Protection in Plain English

Black swan protection means buying insurance for your options portfolio so that one terrible day in the market doesn’t destroy everything.

A simple analogy:

Imagine you’re running a lemonade stand (your wheel strategy) and every week you make $50 selling lemonade (collecting premium). Life is great, but once every few years, a massive storm comes through and destroys your entire stand, costing you $5,000 in damage (a market crash wiping out your positions).

Black swan protection is like paying $2 a week for storm insurance. Most weeks, that $2 feels wasted. But when the storm hits, your insurance pays out enough to rebuild the stand and keep going.

In real options trading terms: you spend about 1–3% of your portfolio each year buying deep out-of-the-money put options. These puts are cheap because nobody expects a crash. But when a crash does happen — like in 2008, 2020, or 2022 — those cheap puts explode in value and offset the losses in the rest of your portfolio.

The key takeaway: Black swan protection isn’t about making money (which you can also do but this isn’t the topic) – It’s about making sure you survive the worst day so you can keep making money on all the other days.

What Is a Black Swan Event?

The term “black swan” was popularized by Nassim Nicholas Taleb in his 2007 book The Black Swan: The Impact of the Highly Improbable. He defined it using three criteria: the event is a surprise to the observer, it has a major impact, and after it happens, people rationalize it as if it were predictable all along.

In financial markets, a black swan event is an extreme, unexpected move that falls far outside what normal statistical models predict. Standard risk models assume that stock returns follow a bell-curve distribution. Under that assumption, a daily drop of 10% or more should essentially never happen — maybe once in several thousand years. Yet we’ve seen multiple events of that magnitude in just the past two decades.

In October 2008, the S&P 500 fell over 40% from its peak in a matter of weeks during the global financial crisis. In March 2020, the COVID pandemic triggered one of the fastest 30%+ declines in market history, with the S&P 500 crashing from 3,386 to 2,237 in just 23 trading days. In 2022, a grinding bear market driven by inflation and rate hikes pulled the index down over 25% from its highs.

Why Black Swan Events Are Especially Dangerous for Options Sellers

When you sell a cash-secured put, you’re making a commitment: you agree to buy 100 shares of stock at the strike price if the stock falls below that level.

In a normal market environment, this works in your favor. The stock stays above your strike, the option expires worthless, and you keep the premium.

But during a black swan event, the stock doesn’t just dip below your strike but it continues crashing down.

If you sold a put on a stock at a $50 strike and collected $2 in premium, your effective cost basis is $48.

Manageable if the stock drops to $45.

Not manageable if the stock drops to $30.

Now multiply that by 10 or 15 positions and you’ve got a big problem on your hands.

That’s the reality many wheel strategy traders face during a crash. Every one of your cash-secured puts gets assigned simultaneously.

Your capital is now fully deployed in stocks that are all falling at the same time and you have no cash left to sell more puts, buy more hedges, or take advantage of the recovery.

This is the correlation problem.

During normal market conditions, your positions are diversified.

For covered call sellers, the risk is different but still severe.

You own the stock. You’ve sold calls against it.

When the crash hits, your short calls expire worthless (small comfort), but your stock positions crater in value. The premium you collected doesn’t come close to covering the losses.

This is why black swan protection matters more for premium sellers than for almost any other type of investor. Your strategy has a defined upside (the premium collected) but a much larger potential downside (the full decline of the underlying stock). Without explicit crash protection, the math eventually catches up with you.

Understanding Tail Risk: Why Normal Models Fail

To understand why black swan protection is necessary, you need to understand why traditional risk management falls short.

Most risk models in finance are built on the assumption that returns are normally distributed — the classic bell curve. Under a normal distribution, about 68% of returns fall within one standard deviation of the mean, 95% within two standard deviations, and 99.7% within three. A move of four or five standard deviations should be almost impossible.

The problem is that real market returns don’t follow a normal distribution. They have what statisticians call “fat tails” — the extreme ends of the distribution curve are much thicker than the bell curve predicts. In practice, this means that crashes of 5%, 10%, or even 20% in a short period happen far more frequently than models suggest.

Value at Risk (VaR), one of the most widely used risk metrics, is particularly vulnerable to this flaw. A 99% VaR might tell you that your maximum daily loss is $10,000 under normal conditions. But it tells you nothing about what happens in the other 1% of scenarios — which is precisely where black swan events live.

This is the fundamental gap that tail risk hedging addresses. Instead of relying on models that assume extreme events don’t happen, you explicitly build protection against them. You acknowledge that the models are wrong about tails and construct a portfolio that can absorb the impact.

For wheel strategy traders, this awareness is especially critical. When you’re running multiple short put positions, your portfolio’s risk profile is concentrated in the left tail — the crash scenario. Your strategy performs well in the middle of the distribution (flat to moderately bullish markets) and suffers catastrophically in the far left tail (crashes). Black swan protection reshapes that risk profile by adding positive exposure to the very scenarios that hurt you most.

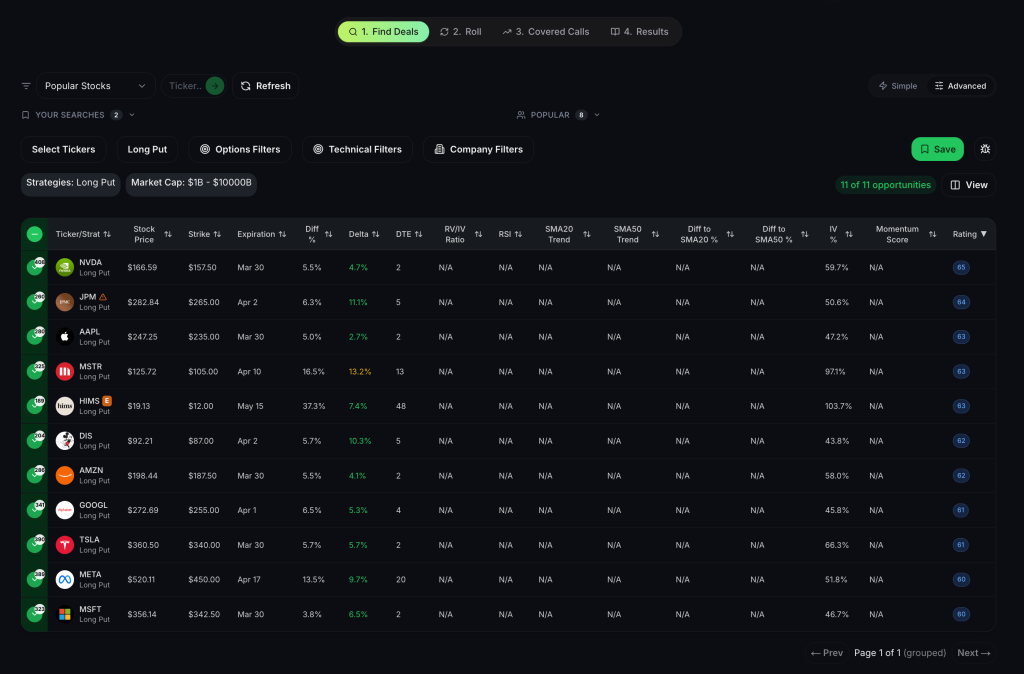

Black Swan Protection Strategy 1: Deep Out-of-the-Money Put Options

You can choose to buy OTM put options in broader markets like SPY or to buy puts on normal stocks. Image above shows the latter.

Find optimal deep OTM puts for protection →

The most straightforward black swan hedge is buying deep out-of-the-money (OTM) put options on a broad market index like SPY or QQQ. These are sometimes called “crash puts” or “tail risk puts.”

Let’s say the S&P 500 is trading at 5,000. You buy SPY put options with a strike price of 3,750 — roughly 25% below the current level.

These puts are very far from the current price, so they’re cheap. You might pay $2–$5 per contract for options with 90–120 days until expiration.

In a normal market, these puts expire worthless. You lose the premium you paid. That’s the cost of insurance.

But if a black swan event sends the market down 30% or more, those puts go from being worth nearly nothing to being worth $50, $100, or more per contract.

A position that cost you $500 could be worth $10,000 or more — enough to offset a significant portion of the losses in your short put positions.

Key parameters for deep OTM crash puts:

The strike price matters. Most tail risk practitioners target puts that are 20–30% out of the money. Too close to the current price and they’re expensive. Too far away and they don’t provide enough protection in a moderate crash. The 25–30% OTM range has historically offered the best protection-to-cost ratio.

Expiration selection also matters. Shorter-dated puts (30–45 days) are cheaper per contract, but you need to roll them more frequently, and you lose premium every month. Longer-dated puts (90–180 days) cost more upfront but give you longer protection windows and more time for a crash to develop. Many practitioners prefer the 90–120 day range and roll positions quarterly.

Position sizing depends on your portfolio and risk tolerance, but a common guideline is allocating 1–2% of your total portfolio value annually to crash puts. This means if you have a $100,000 portfolio, you’d spend roughly $1,000–$2,000 per year on deep OTM puts. It’s a drag on performance in good times, but it can be the difference between a recoverable drawdown and a portfolio-ending loss during a crash.

One important consideration: don’t try to time your hedges. The entire point of black swan protection is that you can’t predict when the event will happen. Maintain your hedges consistently. The temptation to drop your insurance after a year of calm markets is strong, but that’s exactly when you’re most vulnerable.

Black Swan Protection Strategy 2: VIX Call Options

The CBOE Volatility Index (VIX) measures the implied volatility of S&P 500 options and is often called the market’s “fear gauge.” During calm markets, VIX typically trades between 12 and 20. During a crisis, it can spike to 40, 60, or even above 80.

This inverse relationship between the stock market and VIX makes VIX call options a powerful black swan hedge. When stocks crash, VIX surges, and your VIX calls gain substantial value.

During the 2020 COVID crash, VIX went from around 14 to over 82 in less than a month. During the 2008 financial crisis, it spiked above 80 as well. These aren’t small moves — they represent 400–500% increases from normal levels.

Here’s how to implement a VIX hedge. You buy call options on the VIX itself (which are options on VIX futures, not the VIX index directly) with strike prices above the current VIX level. For example, if VIX is at 15, you might buy calls with a strike of 30 or 40. During a crash, when VIX spikes to 50 or 60, those calls become extremely valuable.

There are some important nuances. VIX options are settled in cash, not in VIX shares. They are European-style, meaning they can only be exercised at expiration. And VIX options are priced based on VIX futures, not the spot VIX, which means they can behave differently than you’d expect if you’re only watching the VIX index.

For wheel strategy traders, VIX calls can complement deep OTM puts nicely. Your SPY puts protect against the direct decline in your underlying positions. Your VIX calls benefit from the volatility spike that accompanies the decline. Together, they provide overlapping layers of protection.

The cost of VIX calls as a hedge typically runs 0.5–1.5% of portfolio value annually, depending on strike selection and expiration. Because VIX tends to mean-revert (it always comes back down after a spike), the time decay on VIX calls is significant. This makes position sizing and expiration selection critical. Many traders use 60–90 day VIX calls and roll them monthly to maintain continuous coverage.

Black Swan Protection Strategy 3: Put Spreads and Collars

If the cost of outright crash puts feels too high for your portfolio, put spreads offer a more capital-efficient alternative.

A put spread involves buying a put at one strike price and selling another put at a lower strike price. For example, you might buy a SPY put at a strike of 4,000 and sell a SPY put at 3,500 when SPY is trading at 5,000. The put you sell partially offsets the cost of the put you buy, making the overall hedge cheaper.

The tradeoff is that your protection is capped. In this example, you’re protected between 4,000 and 3,500 — a 20% to 30% decline. If the market falls more than 30%, you don’t get additional protection. For most black swan events, this range captures the bulk of the damage, but it’s worth understanding the limitation.

Collars are another variation. A collar involves owning the underlying stock (or ETF), buying a protective put below the current price, and selling a covered call above the current price. The premium from the call you sell pays for some or all of the put you buy, creating a low-cost or zero-cost hedge.

The downside of a collar is that it caps your upside. If the market rallies strongly, your covered call limits your gains. For wheel strategy traders who are already comfortable with capping upside through covered calls, this tradeoff may feel natural.

For portfolio-level black swan protection, you can apply a collar structure to your entire position: continue selling covered calls on your assigned stocks (you’re doing this already as part of the wheel), and use a portion of that call premium to fund index puts. This creates a self-financing hedge where your income strategy partially pays for your crash protection.

Black Swan Protection Strategy 4: Cash Reserves and Position Sizing

Not all black swan protection requires buying derivatives. One of the most effective hedges is also the simplest: holding cash.

Cash does two things during a black swan event. It limits your exposure (money in cash can’t lose value in a stock crash), and it gives you the ability to act offensively when prices are at their lowest. While other traders are forced to sell into the panic, you have the capital to buy quality assets at deeply discounted prices.

For wheel strategy traders, position sizing is a form of black swan protection that many overlook. If you’re using 100% of your available capital to sell cash-secured puts, you have zero buffer when a crash hits. Every position gets assigned. You have no cash to manage the situation.

A more resilient approach is to keep 20–30% of your capital in cash or short-term treasuries at all times. This means you can only run the wheel on 70–80% of your portfolio. Your income is lower during normal times, but your survival probability during a crash is dramatically higher.

This also connects to sector diversification. If you’re running the wheel on 10 stocks and 8 of them are in the tech sector, a tech-specific meltdown creates outsized risk. Spreading your wheel positions across sectors — tech, healthcare, financials, energy, consumer staples — reduces the probability that a single sector crash takes down your entire portfolio.

Here’s where tracking becomes critical. When you’re managing 10, 15, or 20 wheel positions across multiple sectors, monitoring your aggregate exposure, sector concentration, and available cash becomes a real challenge. Spreadsheets work when you have 3 positions. At 10 or more, things break. You miss expirations. You lose track of cost basis after assignments. You don’t realize you’re 60% concentrated in tech until it’s too late.

This is exactly why platforms like QuantWheel exist — built specifically for wheel traders who need to see their full portfolio picture at a glance. Automatic cost basis tracking, sector exposure views, and position alerts mean you always know where you stand, especially during the volatile moments when it matters most.

[QUANTWHEEL SCREENSHOT] Feature: Portfolio dashboard showing sector allocation and aggregate exposure Caption: “QuantWheel shows your sector concentration and total capital deployment in real time — so you never accidentally over-concentrate during a volatile market.” CTA: “See Your Portfolio Exposure →” links to /features

Black Swan Protection Strategy 5: Tail Risk ETFs and Managed Strategies

For traders who prefer a simpler approach, tail risk ETFs and managed tail risk strategies offer an accessible alternative to building your own hedge from scratch.

The Cambria Tail Risk ETF (TAIL) is one example. It holds a portfolio of U.S. Treasury bonds combined with a ladder of out-of-the-money put options on the S&P 500. During calm markets, TAIL tends to decline slowly as the put options expire worthless. During crashes, the puts increase in value, and the fund can generate significant positive returns.

Allocating 5–10% of your portfolio to an ETF like TAIL provides a form of passive black swan protection. You don’t need to manage individual options positions, roll expirations, or worry about strike selection. The fund handles the hedging mechanics for you.

The tradeoff is cost and drag. Tail risk ETFs typically lose 5–10% per year during normal markets due to the ongoing cost of put options and time decay. Over a multi-year bull market, this drag is significant. The bet you’re making is that the protection during the next crash more than compensates for the drag during good times.

Other approaches include managed futures strategies and long volatility funds, which tend to profit during periods of market stress. These are more complex and typically only available to larger accounts or through institutional allocations, but they represent another layer of potential black swan protection for traders with the means to access them.

Building a Black Swan Protection Plan for Your Wheel Strategy Portfolio

Now let’s put it all together. How do you build a practical black swan protection plan that works alongside your wheel strategy without destroying your income?

Step 1: Assess your current exposure. Look at your total capital deployed in wheel positions. How much is in cash-secured puts? How much is in assigned stock? What’s your sector breakdown? If you don’t know the answers off the top of your head, that’s a sign you need better tracking. You can’t hedge what you can’t measure.

Step 2: Set your protection budget. A reasonable range is 1–3% of total portfolio value per year. On a $100,000 portfolio, that’s $1,000–$3,000 annually — roughly $80–$250 per month. Think of it as the insurance premium for your trading business. If spending $200 per month means you avoid a $40,000 drawdown during the next crash, the math is overwhelmingly in your favor.

Step 3: Choose your hedging instruments. For most wheel traders, a combination of deep OTM index puts (for direct crash protection) and a modest cash reserve (20–30% of capital uninvested) provides the best balance. If you want additional protection, VIX calls or a small tail risk ETF allocation can supplement.

Step 4: Implement systematically. Buy your hedge puts on a regular schedule — quarterly is common. Don’t try to time market fear. Roll positions before they expire. Keep a log of your hedging costs so you can track the annual drag and adjust sizing if needed.

Step 5: Rebalance after stress events. If a crash does occur and your hedges pay off, rebalance back to your target allocation. Take profits on your puts (or let them expire if the crash continues), and use the capital to rebuild your wheel positions at lower, more favorable prices. This is where black swan protection can actually boost long-term returns — it gives you capital to deploy when everyone else is forced to sell.

The Antifragile Wheel: How Protection Actually Improves Performance

This might sound counterintuitive, but a well-hedged portfolio can outperform an unhedged one over a full market cycle. The concept comes from Nassim Taleb’s framework of “antifragility” — systems that get stronger from stress rather than weaker.

Here’s the logic. An unhedged wheel strategy portfolio might generate 2% per month in premium during good times. Over 30 months of a bull market, that’s a 60% return. Then a black swan event hits and the portfolio drops 40%. Your net gain after 30 months: 20%. And it takes another 12–18 months just to recover, during which your capital is tied up in deeply underwater positions and you’re unable to sell puts at attractive strikes.

A hedged portfolio generates slightly less — maybe 1.5% per month after hedging costs, or 45% over the same 30-month bull period. Then the crash hits, but your hedges limit the drawdown to 15%. Your net gain after 30 months: 30%. You recover faster because your positions are less damaged. You have cash to deploy at crash prices. Within a few months, you’re back to full operation, selling puts on quality stocks at elevated premiums.

Over a 10-year period that includes two or three significant corrections, the hedged approach doesn’t just preserve capital — it compounds more effectively because it avoids the deep holes that take years to climb out of.

This is the real argument for black swan protection. It’s not about fear. It’s about math. Avoiding large drawdowns is the single most powerful driver of long-term compound returns. A portfolio that never drops more than 20% will almost always outperform one that drops 50% and recovers, even if the hedging costs create a modest drag during good years.

Common Mistakes in Black Swan Hedging

Even traders who understand the value of black swan protection often make implementation mistakes that reduce or eliminate the effectiveness of their hedges.

Mistake 1: Hedging only after a scare. The worst time to buy crash puts is after volatility has already spiked. Options are most expensive when fear is highest. The best time to buy protection is when nobody thinks they need it — during calm, low-VIX markets when puts are cheap. This is psychologically difficult, but it’s how effective hedging works.

Mistake 2: Letting hedges lapse. After paying for protection for 12 or 18 months without a crash, many traders abandon their hedges to save money. This is like canceling your home insurance because your house hasn’t burned down. The risk hasn’t changed — you’ve just stopped paying for coverage.

Mistake 3: Buying too little protection. A single SPY put on a $200,000 portfolio isn’t meaningful protection. Size your hedges so that the payout in a 30% crash scenario actually moves the needle. Run the math: if the market drops 30%, how much do your current hedges pay out? If the answer is less than 10% of your portfolio losses, you’re underhedged.

Mistake 4: Ignoring the cost basis problem. During a crash, all your short puts get assigned simultaneously. Your broker shows one cost basis. Your real cost basis — factoring in all the premium you’ve collected through the wheel cycle — is different. If you panic-sell because you think you’re down 30% when your real drawdown is only 20% after premiums, you lock in unnecessary losses.

This is a genuine problem for wheel traders under stress. Accurate cost basis tracking matters most during the moments when you’re least likely to sit down and update a spreadsheet. QuantWheel’s automatic cost basis adjustment handles this — when you get assigned, your real cost basis is already calculated, including all premium collected. During a crash, knowing your actual numbers can be the difference between a smart decision and a panic-driven mistake.

Mistake 5: Over-hedging. Spending 5–6% of portfolio value annually on protection is too much for most retail traders. The drag overwhelms the benefit in all but the most severe crashes. Keep your hedge budget in the 1–3% range and focus on capital-efficient structures like put spreads rather than outright puts if cost is a concern.

Black Swan Protection for Small Accounts

If you’re trading with a $25,000 or $50,000 account, you might think black swan protection is only for large portfolios. It’s not, but you do need to be more creative with implementation.

For small accounts, the simplest approach is position sizing discipline. Don’t use more than 50–60% of your capital for cash-secured puts. The remaining 40–50% in cash is your hedge. It won’t profit from a crash, but it limits your exposure and gives you ammunition for the recovery.

If you want options-based protection, consider buying 1–2 deep OTM SPY puts per quarter. At current prices, a 25% OTM SPY put with 90 days to expiration might cost $100–$300 per contract. On a $50,000 portfolio, spending $400–$800 per year on crash puts represents a hedge budget of about 1–1.5% — right in the sweet spot.

Another small-account-friendly approach is using weekly SPY put debit spreads as a rolling hedge. These are cheaper than outright puts and can be sized to match your risk tolerance. The protection is capped, but for a small account, even partial protection is far better than none.

When Black Swan Protection Doesn’t Work

Transparency is important, so let’s be clear about the limitations.

Black swan protection doesn’t protect against slow, grinding bear markets. A market that declines 2% per month for 12 months results in a similar total drawdown as a crash, but your puts expire worthless along the way because the moves are incremental. Protection against slow declines comes from position management (rolling, closing losers early) rather than crash hedges.

Black swan protection is also expensive during extended low-volatility periods. If you hedge consistently for 5 years without a significant crash, you’ve spent 5–15% of portfolio value on protection that never paid off. That’s a real cost, and it’s the reason many traders abandon their hedges — which, as noted above, is itself a risk.

Protection also doesn’t eliminate losses. Even a well-hedged portfolio will decline during a black swan event. The goal isn’t to make money during a crash (though some hedges might). The goal is to reduce the drawdown from catastrophic to manageable. A 15% drawdown is survivable. A 50% drawdown is not, especially for options sellers who need capital to continue operating.

And finally, hedges can fail in unexpected ways. Liquidity can dry up during a crisis, making it difficult to sell your hedge positions at fair value. Counterparty risk exists, though it’s minimal for exchange-traded options. And if the crash is caused by a gap move (market opens sharply lower without trading through intermediate prices), your hedge may not provide as much protection as backtests suggest.

None of these limitations means you shouldn’t hedge. They mean you should hedge with realistic expectations. Black swan protection is risk management, not risk elimination. It shifts the distribution of outcomes in your favor, but it doesn’t guarantee a profit.

Real-World Black Swan Events and What They Taught Us

Let’s look at three recent black swan events and the lessons they hold for options sellers.

The 2008 Financial Crisis. The S&P 500 dropped over 50% from peak to trough. VIX spiked above 80. Options premiums went through the roof, but so did assignment risk. Traders who were selling puts on financial stocks got assigned on positions that dropped 70–80%. Lesson: sector concentration kills. If your wheel positions were spread across sectors and you held deep OTM index puts, you survived. If you were concentrated in financials without protection, you didn’t.

The 2020 COVID Crash. The S&P 500 fell 34% in 23 trading days, one of the fastest declines in history. Then it recovered almost completely within 5 months. Traders who panic-sold during the crash locked in catastrophic losses. Traders who had hedges in place were able to ride out the volatility and even deploy capital at the lows. Lesson: speed matters. By the time you realize you need protection, it’s too late to buy it. Hedges must be in place before the event.

The 2022 Bear Market. Unlike 2008 and 2020, this was a slower decline driven by inflation and interest rate hikes. The S&P 500 dropped about 25% over 9 months. Crash puts provided less value because the decline was gradual. Cash reserves and position management (rolling, closing losers, reducing position sizes) were more effective hedges. Lesson: no single hedge works in every scenario. A diversified protection approach — some puts, some cash, some discipline rules — covers more bases than any single instrument.

Putting It All Together: A Sample Black Swan Protection Framework

Here’s a practical framework for a $100,000 wheel strategy portfolio. This is an educational example, not a recommendation. Adjust the numbers based on your own risk tolerance, account size, and market conditions.

Capital allocation: Deploy 70% ($70,000) in wheel positions. Keep 30% ($30,000) in cash or short-term treasuries as a buffer.

Hedging budget: 2% of total portfolio = $2,000 per year, or roughly $500 per quarter.

Hedge instruments: Each quarter, buy 2–3 deep OTM SPY puts (25–30% below current price, 90–120 day expiration) using your $500 quarterly budget. This provides meaningful crash protection across the entire portfolio.

Position management rules: Close any individual wheel position at a 20% loss on the underlying. Roll aggressively before assignment if the position is challenged. Monitor sector concentration — no more than 30% in any single sector.

Crash response plan: If a hedge pays off during a crash, use the profits to buy quality stocks at depressed prices. Resume selling puts at higher premiums (volatility spikes mean bigger premiums). Don’t try to catch the exact bottom — scale back into positions over 4–8 weeks.

How QuantWheel Helps You Stay Protected

Managing black swan protection alongside 10 or more wheel positions is complex. You need to track your hedge expirations, monitor sector concentration, know your true cost basis on every position, and maintain awareness of your overall portfolio risk.

This is operational, not theoretical. And it’s where most wheel traders break down — not because they don’t understand hedging, but because tracking everything manually is a full-time job.

QuantWheel was built specifically for this kind of portfolio management. Automatic cost basis tracking through assignments. Real-time position dashboards. Sector concentration views. Alert systems that notify you when positions need attention. When a crash happens, you’ll know exactly where you stand — your real cost basis, your true drawdown, and which positions need immediate action.

Black swan protection starts with knowledge. You can’t protect a portfolio you can’t see clearly.

Start your free trial of QuantWheel →

Risk Disclosure: Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.