You sold your first covered call last month and collected $150 in premium. It felt like free money—until the stock rallied 20%, your shares got called away, and you watched from the sidelines as it climbed another 30%. Now you're wondering what went wrong.

The covered call strategy sounds simple: own stock, sell calls, collect premium. But between theory and profit lies a minefield of mistakes that cost traders thousands annually. Some leave money on the table. Others force you to sell stocks you wanted to keep. The worst ones create tax nightmares and emotional decisions that compound into larger losses.

After analyzing thousands of covered call trades and talking with traders managing this strategy across multiple positions, we've identified the seven mistakes that separate profitable covered call traders from those who struggle. More importantly, we'll show you exactly how to fix each one.

Create a trading system inside QuantWheel to avoid mistakes →

TLDR: Most Common Covered Call Mistakes

The quick answer: The seven most common covered call mistakes are selling calls on stocks you want to keep, choosing wrong strike prices, ignoring ex-dividend dates, poor rolling decisions, missing earnings announcements, emotional trading, and failing to track cost basis properly.

Simple example: Imagine you own 100 shares of Apple at $150. You sell a $155 call for $3 premium, thinking you'll collect income while keeping your shares. Apple jumps to $165, your shares get called away at $155, and you miss the extra $10 per share ($1,000 total). You collected $300 in premium but gave up $1,000 in gains—a net $700 mistake. If you'd chosen a $160 strike (less premium but higher breakeven) or rolled the position before expiration, you could have kept your shares or captured more upside.

The fix: Match your strike selection to your actual goals. If you want to keep the shares, sell out-of-the-money calls at higher strikes (15-20 delta). If you're willing to sell, use lower strikes (30-40 delta) for more premium. Track ex-dividend dates, earnings, and have a rolling plan before you enter each trade.

Mistake #1: Selling Covered Calls on Stocks You Want to Keep Long-Term

This is the most emotionally painful mistake, and it's shockingly common. You own 500 shares of a quality company—maybe NVIDIA, Microsoft, or Tesla. You've held it for years, believe in the long-term story, and have no intention of selling. Then someone mentions covered calls as "free income," and you decide to try it.

You sell five covered calls and collect $1,500 in premium. Everything's great until the stock rallies 25% in two months. Suddenly, your shares are about to be called away at a price well below the current market value. You're facing a tough choice: buy back the calls at a loss, roll the position (maybe for a debit), or watch your long-term position disappear.

Why this happens: Traders conflate two different strategies. One is long-term buy-and-hold investing. The other is covered call income trading. They have different goals, different timeframes, and different success metrics. Mixing them creates emotional conflict.

The real cost: Beyond the obvious opportunity cost of missing the rally, you face:

- Tax implications if you've held shares under a year (short-term vs. long-term gains)

- Emotional decision-making when you try to "save" the position by rolling for debits

- Whipsaw losses if you buy back the calls, the stock drops, and you're left with losses on both sides

How to fix it:

Create two separate portfolios mentally:

- Core holdings: Stocks you want to keep 5+ years. Never sell calls on these, or only sell calls so far out-of-the-money (5-10 delta) that assignment is extremely unlikely.

- Trading positions: Stocks you're willing to sell at the strike price. Sell covered calls here with appropriate strikes (20-40 delta).

If you absolutely must generate income from core holdings, consider:

- Selling calls only during extreme volatility spikes (IV rank above 70)

- Using strikes 15-20% above the current price

- Accepting tiny premium in exchange for keeping shares

- Never rolling for a debit—just accept assignment if it happens

Mistake #2: Choosing Strike Prices Based Only on Premium Yield

The second biggest mistake sounds rational on the surface: "I want to maximize my income, so I'll sell the strike that generates the most yield." You calculate that selling the at-the-money or slightly in-the-money call generates 3-5% monthly yield, while the out-of-the-money strike only generates 1-2%.

Easy choice, right? Wrong.

Why this backfires: Higher premium equals higher probability of assignment. When you sell the at-the-money or in-the-money call, you're essentially saying "I want to sell this stock at this price." If you're not mentally prepared for that, you've made a mistake before the trade even starts.

Consider the math: A 30-delta call has roughly a 30% probability of being in-the-money at expiration. If you're selling these weekly, you're facing assignment every 3-4 weeks on average. That's fine if selling is your goal, but it means constant position churn, tracking headaches, and frequent tax events.

Real trader example:

- Owns stock at $48 per share

- Sells 30-delta calls every week for $1.20 premium

- Gets assigned within three weeks when stock hits $51

- Sells at $50 strike, missing the move to $51

- Net result: $2 gain on stock + $1.20 premium from first call + $1.20 from second call = $4.40 total

- Could have: Sold at $51 with no calls = $3 gain, less premium but cleaner execution and lower transaction costs

The fix: Use the Strike Selection Triangle

Balance three factors:

- Desired yield: Premium as percentage of stock price

- Probability of assignment: Based on delta (30-delta = ~30% probability)

- Acceptable sale price: Would you be happy selling here?

Most successful covered call traders target:

- 15-20 delta for stocks they prefer to keep (85-80% chance of keeping shares)

- 25-30 delta for balanced income/retention

- 35-45 delta for stocks they're ready to sell (higher probability of assignment)

The "perfect" strike depends on your goal. If you're using covered calls to exit a position at a target price while collecting extra premium, higher deltas work. If you want repeatable income while maintaining the position, lower deltas are better.

Mistake #3: Ignoring Ex-Dividend Dates

Missing ex-dividend dates is a $200-500 per position mistake that's completely avoidable. Here's how it happens: You sell a covered call on a dividend-paying stock without checking when the ex-dividend date occurs. If your call is in-the-money as the ex-dividend date approaches, you're at serious risk of early assignment.

The mechanics: Option holders can exercise American-style options at any time. When a stock is about to pay a dividend, call holders might exercise early to:

- Capture the dividend (they become stock owners before ex-date)

- Especially if the dividend is larger than the remaining time value in the call

When this happens, you:

- Lose your shares before expiration

- Miss collecting the dividend (it goes to the new owner)

- Still have to deliver shares at the strike price

- Get hit with assignment fees from your broker

Real cost example:

- Own 1,000 shares of AT&T at $18 (hypothetical)

- Sold 10 covered calls at $19 strike for $0.60 premium

- Collected $600 total

- Ex-dividend date approaches, stock pays $0.25 dividend

- Calls get exercised early

- You miss $250 in dividends

- Net result: $600 premium - $250 lost dividend = $350 (compared to $850 if you'd kept both)

How to fix it:

Before selling any covered call:

- Check the ex-dividend date (usually available on your broker platform or Yahoo Finance)

- Check the amount of the dividend

- Calculate if early exercise is likely (dividend larger than time value remaining in call)

Strategy adjustments:

- Conservative: Never sell covered calls that expire between now and ex-dividend date

- Moderate: Only sell out-of-the-money calls before ex-dividend (less likely to be exercised)

- Aggressive: Accept that you might miss the dividend, price it into your decision

The smart approach: Use covered calls on dividend stocks AFTER the ex-dividend date passes. This way you:

- Collect the dividend

- Then sell the call for the next expiration

- Eliminate early assignment risk

- Generate income from two sources (dividend + premium)

Mistake #4: Rolling at the Wrong Time (or Not Rolling at All)

Rolling covered calls—closing the current call and selling a new one at a different strike or expiration—is where many traders lose money through poor timing and decision-making. The mistake comes in two forms: rolling when you shouldn't, and not rolling when you should.

When traders roll incorrectly:

Mistake 4A: Panic Rolling for a Debit

Your covered call goes in-the-money, assignment looks likely, and you panic. You buy back the call for $3 and sell a new one at a higher strike for only $2.50. You've paid $0.50 (a debit) to roll the position. If you do this repeatedly, you're paying to delay the inevitable instead of accepting that the stock reached your price target.

Real example:

- Sold $50 call for $1.50

- Stock rises to $52

- Buy back the call for $2.50 (loss of $1.00)

- Sell $55 call for $1.00

- Net result: Paid $0.50 to move the strike higher

- If stock continues to $55, you'll be tempted to roll again, compounding the problem

Mistake 4B: Never Rolling (Leaving Money on the Table)

The opposite mistake: Your covered call is deep in-the-money with only $0.10 of time value remaining and 20 days until expiration. You could roll to next month for a net credit, but you don't bother. You're essentially letting $0.10 decay to zero instead of collecting another $1.50 in fresh premium.

How to fix rolling decisions:

Rule 1: Only roll for a net credit If you can't roll to a further expiration or higher strike for a credit, you're better off:

- Accepting assignment if you're ready to sell

- Holding until expiration if you still want shares

- Closing the call and keeping shares (if you've changed your mind about selling)

Rule 2: Roll when time value is minimal (under 21 DTE or under 50% of original premium) When your call has:

- Less than 21 days to expiration, AND

- Less than 50% of its original value remaining

Consider rolling to next expiration. You can often collect more premium by rolling out in time, even if keeping the same strike.

Rule 3: Have a rolling plan BEFORE you enter the trade Before selling any covered call, decide:

- At what percentage profit will you close early? (Many traders use 50% profit as a target)

- Will you roll if ITM, or accept assignment?

- What's your maximum acceptable debit to roll? (Suggestion: $0, meaning only credit rolls)

Example of good rolling:

- Sold $50 call for $1.50

- Three weeks later, call is worth $0.60 (60% profit)

- Stock is at $49.50 (still below strike)

- Close the call for $0.60, keeping $0.90 profit

- Sell a new call at $50 or $51 for next month

- Collect fresh premium without waiting for final decay

This approach lets you "take profit" on the option while resetting for another premium collection opportunity.

Mistake #5: Selling Calls Right Before Earnings Announcements

Earnings announcements bring volatility—and with volatility comes both opportunity and risk. The mistake isn't selling covered calls around earnings (sometimes this is the best time). The mistake is selling them without understanding what you're doing.

The two-sided problem:

Problem 1: Missing the IV spike Implied volatility increases before earnings as uncertainty rises. Options become more expensive. If you sell your covered call two weeks before earnings, you miss the elevated premium available in the final week. You're leaving money on the table.

Problem 2: Selling right before earnings without a plan You sell a call three days before earnings to capture the high IV. The stock beats estimates and gaps up 15% overnight. Your shares get called away at the strike, and you miss the massive move. Or worse, you panic and buy back the call for a huge loss.

The smart approach to earnings:

Strategy 1: Sell calls AFTER earnings (IV crush)

- Wait for earnings to pass

- Volatility collapses (IV crush)

- Sell calls at lower absolute premium but better risk/reward

- Less chance of overnight gaps affecting your position

Strategy 2: Sell calls 5-7 days before earnings (maximize IV)

- Capture elevated premium from high IV

- Choose far out-of-the-money strikes (10-15 delta)

- Accept that a big move could mean assignment

- Only do this on stocks you're genuinely willing to sell

Strategy 3: Avoid earnings entirely

- Only sell calls that expire before earnings

- Or only sell calls after earnings has passed

- Accept lower premium in exchange for more predictable outcomes

- Best for conservative traders or positions you want to keep

Red flag example (what not to do):

- Own stock at $100

- Earnings in 2 days

- Sell $105 call for $4 (looks like great premium!)

- Stock beats and gaps to $120

- Your shares are called away at $105

- You collected $4 but missed $15 in upside (net $11 per share loss)

Green flag example (proper execution):

- Own stock at $100

- Earnings in 5 days

- Sell $110 call for $2.50 (capturing IV but giving room for upside)

- Even if stock goes to $115, you're happy to sell at $110 + $2.50 = $112.50 effective

- If stock drops or stays flat, you keep premium and shares

The key: Match your strike selection and timing to your actual willingness to accept assignment. Don't get seduced by high premium without understanding the risk.

Mistake #6: Emotional Decision-Making Instead of Systematic Process

Covered calls are mechanical. Success comes from consistency, not from clever adjustments. Yet many traders abandon their process when emotions take over.

Common emotional mistakes:

Chasing losses: Your call loses money, so you sell another call at a lower strike to "make it back faster." Now you're doubling down on a position that's already against you.

Greed-based strike selection: You sell the highest premium strike available because you want more income this month, ignoring that it's practically at-the-money and will definitely get assigned.

Fear-based buying back: Stock dips slightly, and you panic-buy back your call at a loss, thinking the stock will collapse. Then it recovers, and you've locked in a loss for no reason.

Attachment to positions: You refuse to let shares get called away, even though assignment was always part of your plan. You roll for debits repeatedly, losing money to keep shares you should have sold.

The fix: Create a mechanical system

Before entering any covered call trade, document:

- Strike price and expiration selected

- Premium collected

- Target closing percentage (e.g., "close at 50% profit")

- Assignment plan ("if assigned, immediately look for new entry" or "if assigned, wait for pullback")

- Rolling rules ("only roll for credit" or "never roll, always accept assignment")

- Earnings date and ex-dividend date

During the trade:

- Check positions at specific times (e.g., daily at market close), not constantly

- Follow your rules even when you don't feel like it

- Track what happens when you break rules vs. follow them

The data doesn't lie: Traders who follow consistent covered call rules outperform those who make discretionary decisions by an average of 15-20% annually. The edge isn't in being clever—it's in being consistent.

Example mechanical system:

- Only sell covered calls on stocks you'd be happy to sell

- Target 25-30 delta strikes

- Close at 50% profit or 21 DTE, whichever comes first

- Roll only for net credit

- Never roll more than twice on same position

- Accept assignment without emotion

This system won't be perfect, but it will be profitable over time. And it removes emotion from the equation.

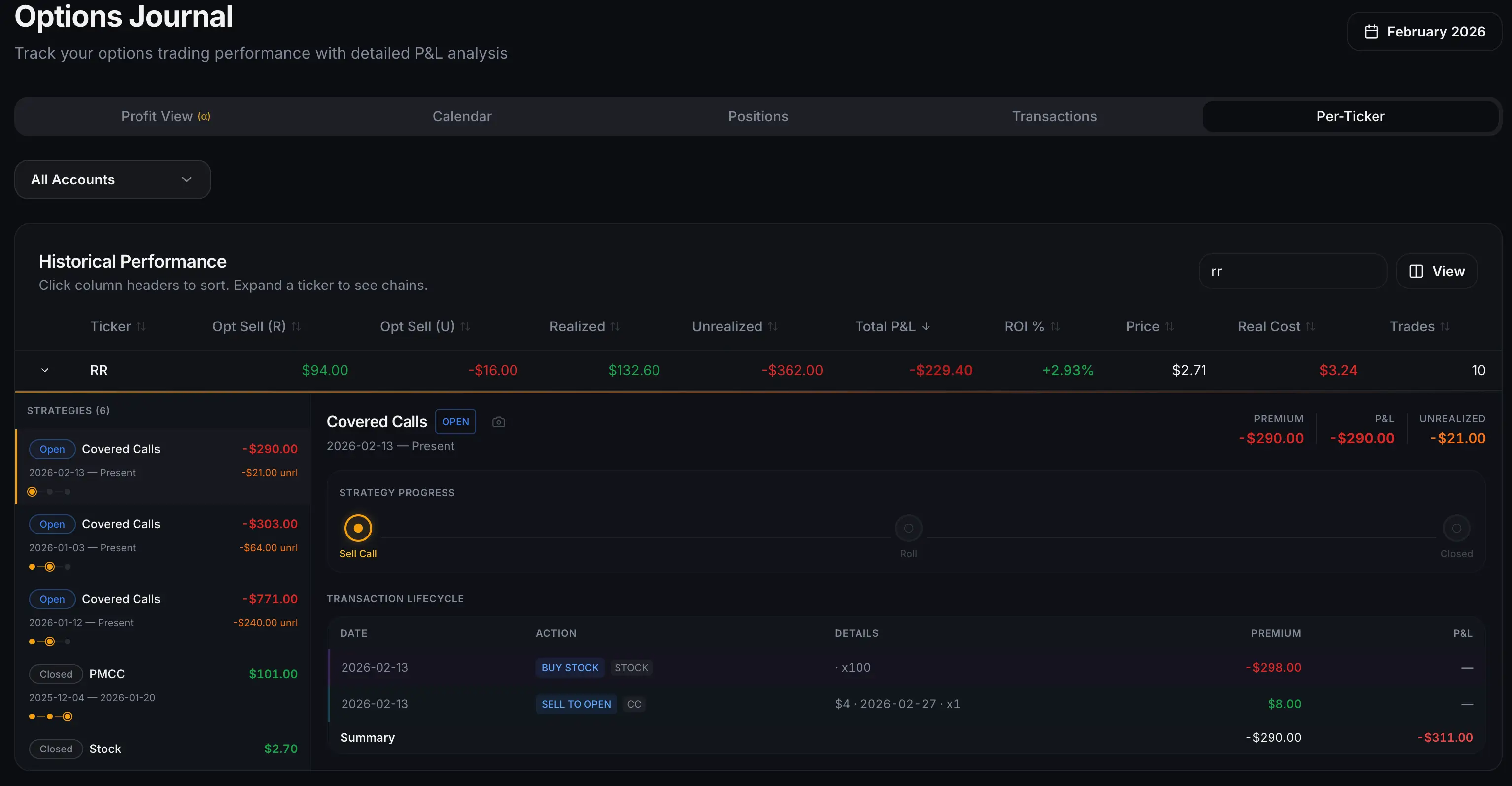

Mistake #7: Not Tracking Cost Basis Through Assignment

This mistake doesn't hurt immediately, but it creates confusion, tax headaches, and poor decision-making over time. When you sell covered calls and get assigned, your tracking needs to be precise—or you'll lose sight of your actual returns and make bad future decisions.

What goes wrong:

You buy stock at $50. You sell a covered call and collect $2 in premium. You get assigned at $52. Simple, right?

Not quite. Here's what you need to track:

- Purchase price: $50

- Premium collected: $2

- Sale price: $52

- Real profit: $4 per share ($2 capital gain + $2 premium)

- Tax treatment: Short-term or long-term depending on holding period

Now multiply this by 10 positions running simultaneously, some with multiple rolls, some with partial assignments, and some held through multiple cycles. Without systematic tracking, you:

- Don't know your real cost basis

- Can't calculate true returns accurately

- Make poor decisions about which strikes to select

- Face a nightmare during tax season

The compounding problem:

After assignment, you want to re-enter the wheel strategy. But should you enter at $50 again? $48? $52? Without knowing your total return from the last cycle (including all premium collected), you're guessing.

Even worse, your broker's cost basis calculation might not include the premium from sold calls. Your broker might show your shares were purchased at $50 and sold at $52 (+$2), but they won't automatically account for the $2 in call premium you collected. That's a separate transaction in their system.

How to fix it:

Manual tracking (minimum): Create a spreadsheet with:

- Ticker

- Purchase date and price

- Call sold date, strike, expiration, premium

- Any rolls (dates, strikes, credit/debit)

- Assignment date and price

- Total premium collected across all calls

- Real cost basis (purchase price - total premium)

- Actual profit (sale price - real cost basis)

Automated tracking (recommended): Use a platform built for this. Spreadsheets break down after 5-10 positions because:

- You forget to update them

- Roll calculations become complex

- It's tedious and error-prone

- No real-time visibility

Here's where most traders struggle: calculating your actual cost basis after assignment. Your broker shows you bought stock at $50, but your real basis after collecting $2 in premium is $48 per share. You need to track this manually across every position.

Unless you're using a platform like QuantWheel that automatically adjusts your cost basis when assignments happen. It tracks your full wheel cycle—cash-secured puts, assignments, covered calls, and exits—calculating your real returns without manual spreadsheet updates.

Get everything calculated for you inside QuantWheel →

Tax preparation benefit:

Come tax season, you need to report:

- Short-term vs. long-term capital gains (depends on holding period)

- Premium collected (always short-term income)

- Wash sales if you rebuy the same stock within 30 days

Proper tracking throughout the year makes April painless. Poor tracking means hours of reconstruction and potential errors that could cost you money.

The bottom line: If you're running covered calls on more than 2-3 positions, automated tracking isn't a luxury—it's essential for maintaining your edge and reducing errors.

How to Avoid All Seven Mistakes: A Systematic Approach

The solution to covered call mistakes isn't trying harder or being smarter. It's having a system that prevents mistakes before they happen.

Create your covered call rulebook:

Position Selection Rules:

- Only sell calls on stocks I'm willing to sell

- Separate "core holdings" (rarely or never sell calls) from "trading positions"

- Check ex-dividend date and earnings date before every trade

- Only enter positions I can actively monitor

Strike Selection Rules:

- Use 15-20 delta for positions I want to keep

- Use 25-35 delta for balanced income/retention

- Use 40-50 delta only for positions I'm exiting

- Never select based on premium yield alone

Management Rules:

- Close at 50% profit or 21 DTE, whichever comes first

- Only roll for net credit

- Never roll more than twice on the same strike

- If stock fundamentals change, close the position entirely

Tracking Rules:

- Record every trade in tracking system (spreadsheet minimum, software preferred)

- Update cost basis immediately after assignment

- Review all positions weekly

- Monthly review of what worked and what didn't

Emotional Control Rules:

- Never deviate from the plan in the middle of a trade

- If I want to change strategy, close the position first, then reset

- Accept that assignment is a good outcome, not a failure

- Remember: The goal is consistent returns, not perfect execution

Final Thoughts: Mistakes Are Tuition, But Only If You Learn

Every covered call trader makes mistakes. The question is whether you learn from them or repeat them. The seven mistakes we've covered cost traders thousands annually—but they're all preventable with the right approach.

The path from struggling to successful looks like this:

- Recognize which mistakes you're making

- Implement systematic rules to prevent them

- Track everything so you can see what works

- Adjust based on data, not emotion

- Repeat the profitable process consistently

Covered calls are one of the most forgiving options strategies. You can make mistakes and still be profitable. But why settle for "profitable despite mistakes" when you can be "consistently profitable through good process"?

Start by fixing one mistake at a time. Most traders see the biggest improvement by separating stocks they want to keep from stocks they're willing to sell. That single shift eliminates the emotional conflict that leads to expensive rolling and poor decisions.

From there, add strike selection rules, implement early closing targets, and build proper tracking. Within a few months, your covered call results will improve measurably.

The edge isn't in finding secret strike selection formulas or timing the market perfectly. The edge is in avoiding the mistakes that cost everyone else money.

Risk Disclosure

Risk Disclosure: Options trading involves substantial risk and is not suitable for all investors. Covered calls limit upside potential and do not protect against downside risk beyond the premium collected. Past performance does not guarantee future results. This content is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions.

The examples used in this article are for educational purposes only and are not recommendations to buy or sell any security. All investment decisions should be based on your own analysis and risk tolerance.